How FY2025 sustainability reports are improving under NSRF, and where they still fall short

The 2025 sustainability reports of public listed companies with a Dec 31 financial year-end are hot off the press.

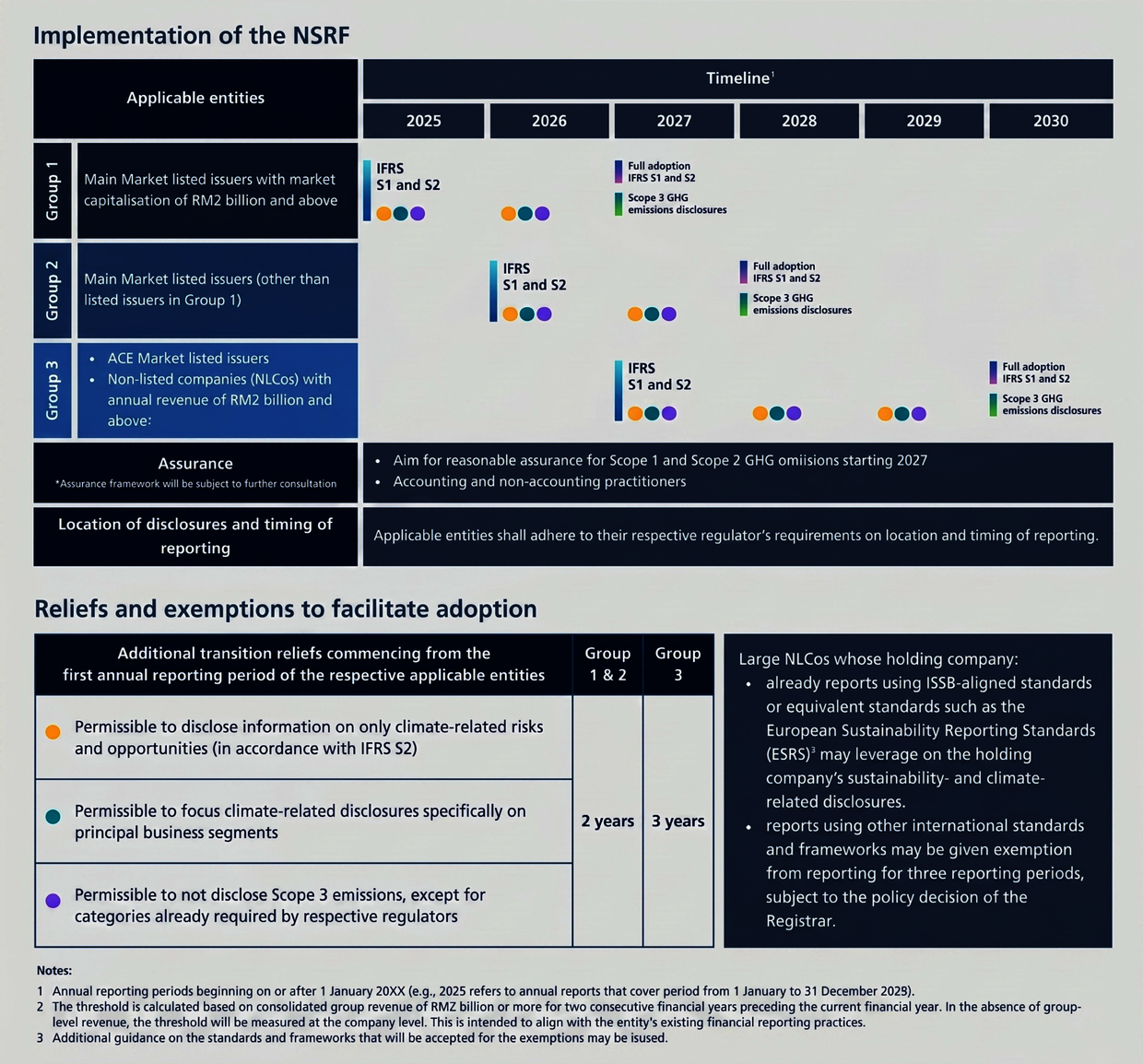

For main market listed issuers with a market capitalisation of RM2bil and above, the reports marked their first year of sustainability disclosures aligned with the National Sustainability Reporting Framework (NSRF).

Under the framework, the reports have to be prepared in accordance with the International Sustainability Standards Board’s IFRS S2 Climate-related Disclosures, detailing the climate-related physical and transition risks faced by the companies, as well as the climate-related opportunities they may be able to leverage. The NSRF is meant to ensure companies provide consistent, comparable and reliable sustainability information.

This represents a fundamental shift from the traditional corporate sustainability reporting approach which uses frameworks such as Global Reporting Initiative (GRI), noted KPMG Malaysia partner – head of sustainability reporting and assurance Koh Ree Nie.

“Unlike GRI, which focuses primarily on impact materiality, IFRS S2 emphasises financial materiality, the financial implications of climate-related risks and opportunities as well as the connectivity between sustainability disclosures and the financial statements,” she said.

PwC Malaysia sustainability and climate change director Farhana Jabir said the investor-focused reporting places emphasis on how sustainability considerations impact an organisation’s financial performance.

The reports offer insight into organisational approaches to climate risk management, monitoring capabilities and data infrastructure maturity, she added.

“These disclosures reveal how well-equipped organisations are to track and respond to the financial impacts of climate challenges while providing transparency into their strategic methodology and analytical rigour.”

In all, the NSRF and the adoption pathways towards IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 have accelerated the maturity of reporting practices, Koh said.

“This regulatory push has encouraged companies to strengthen governance practices, enhance climate-related disclosures and improve the integration of sustainability matters within overall risk management and business strategy.”

Improvements observed

Many organisations are focusing on climate-first disclosures and making use of the proportionality mechanisms as a way to ensure information reported is factual while internal capabilities mature, Farhana noted.

The reports showed that the sustainability conversation within the organisations has moved up to the C-suite agenda, with greater involvement from C-suite executives in understanding climate-related and broader sustainability-related risks, quantifying potential impacts and determining how these should be communicated to their stakeholders.

“This top-down commitment signals a maturation in corporate governance around sustainability matters and suggests that these disclosures will increasingly inform strategic decision-making,” she said.

These are positive signs that the market is moving towards investor-grade disclosures that support both management and investor needs, Farhana added.

From investors’ perspectives, she explained, the newly-introduced financial quantification of climate-related risks and opportunities with explicit linkages to financial statements will be the most significant advancement in sustainability disclosure transparency.

Unlike previous reporting regimes, these reports now provide direct visibility into how climate considerations impact financial performance and position.

“Importantly, the IFRS elevates sustainability reporting to financial-grade reporting, with chief financial officers now assuming key responsibility for these reports, whereas previous sustainability reporting typically fell under the purview of chief risk officers or sustainability functions.

“Some companies are beginning to provide clearer linkages between climate-related risks and their financial statements. Others are still at an earlier stage. This variation is expected in the first year, but will be an important indicator of reporting maturity,” she said.

What investors need

In this first batch of IFRS S2-aligned reports, investors are likely to focus heavily on how climate-related risks and opportunities are connected to the companies’ financial performance, strategy and long-term resilience, Koh said.

More specifically, investors will be looking for evidence that climate-related matters are not disclosed merely as standalone sustainability narratives, but are meaningfully integrated into financial decision-making, risk management and business planning.

They would most likely focus on:

- How climate risks and related capital expenditures are reflected in cash flow projections, asset valuations and impairment assessments, which demonstrate connectivity between climate disclosures and the financial statements.

- Identification of assets and operations that are vulnerable to physical climate risks, together with management’s mitigation strategies and adaptation plans.

- Which business segments or revenue streams are exposed to climate transition risks, including regulatory changes, evolving customer preferences or technological disruption and how management intends to respond to these risks.

- The company’s resilience analysis, including the use of climate-related scenario analysis to assess the robustness of its strategy under different climate pathways

- For carbon-intensive industries, the credibility of decarbonisation strategies, particularly in light of the anticipated implementation of carbon pricing or carbon tax mechanisms

Koh said investors and stakeholders should pay close attention to whether companies are demonstrating concrete actions, measurable progress and accountability, beyond headline net-zero commitments and aspirational sustainability targets.

Specifically, they should look at what initiatives or operational changes have already been implemented or are planned, the level of investment and capital expenditure allocated for decarbonisation or climate adaptation efforts, and whether management decisions and resource allocations are aligned with the sustainability commitments.

Another key item is the extent to which targets are supported by measurable milestones, timelines and performance indicators, Koh added.

Gaps identified

Noting that the sustainability reporting remains primarily driven by compliance expectations at this stage, Koh said many companies appear focused on meeting the core mandatory requirements, often relying on transitional reliefs and providing limited voluntary or forward-looking disclosures beyond baseline compliance expectations.

As such, stakeholders may find it difficult to assess how effectively companies are identifying, managing and responding to sustainability-related risks and opportunities, she said.

“As companies transition from GRI’s broader multi-stakeholder approach to the investor-centric focus of IFRS S1 and S2, many disclosures still appear oriented towards stakeholder legitimacy and reputational positioning rather than investor decision-making needs.”

Koh added that the linkage between sustainability matters and financial performance, including integration within the financial statements or Management Discussion and Analysis (MD&A), remains relatively weak.

Common gaps include:

- Immature greenhouse gas (GHG) emissions reporting, particularly in relation to Scope 1 and Scope 3 disclosures

- Sustainability data quality and internal control processes are still less developed compared to those established for financial reporting

- A heavier emphasis on qualitative narratives rather than quantitative, financially-linked sustainability disclosures

- Limited use of scenario analysis and forward-looking assessments

- Generic disclosures with insufficient company-specific insights and measurable outcomes

Challenges

With the current geopolitical climate, substantial complexity has been added to sustainability disclosure preparation, PwC’s Farhana noted.

Organisations have to dedicate considerable resources to articulate how their climate initiatives and commitments may be affected by the volatile, uncertain, complex and ambiguous environment, and management teams have to explain how the organisation is managing medium-and long-term risks, particularly transition risks, while acknowledging the potential impacts of geopolitical factors.

“IFRS S2’s specific requirements for disclosing capital deployment related to climate risk management are highlighting the critical importance of integrating climate considerations into core business planning processes.

“But organisations are discovering that developing these disclosures requires substantial lead time and strategic alignment across multiple business functions,” Farhana elaborated.

In practice, this points to a broader organisational shift, she said.

“ESG no longer sits primarily within the sustainability function. While the first wave of integration is likely to be led by finance and risk functions, meaningful climate risk reduction will depend on how effectively companies embed ESG considerations into operations, procurement and broader value chain decisions.”

What to improve

Building on the foundation they have laid in their FY2025 sustainability reporting, companies are expected to demonstrate greater maturity in their FY2026 reports.

Farhana anticipated advancement in financial quantification methodologies, including climate scenario analysis.

“Companies are expected to move beyond foundational scenario frameworks to develop more nuanced, sector-specific analyses that provide deeper insights into potential future operating environments and strategic implications.”

She also expected progress in Scope 3 measurement, although meaningful progress will likely require a broader ecosystem push.

“For example, the Companies Commission of Malaysia’s (SSM) recently proposed framework, which would require non-listed companies to begin reporting their Scope 1 and 2 emissions, could help strengthen the data foundation needed for more reliable value chain emissions reporting,” Farhana added.

KPMG’s Koh, meanwhile, said she expects to see more company-specific and granular disclosures that provide clearer insights into how climate-related risks and opportunities are impacting the company, including more detailed explanations of the strategies, mitigation measures and action plans.

More quantitative information on the financial impacts of climate-related risks and opportunities would complete the narrative and qualitative disclosures, she added.

“This may include disclosures on investments, capital expenditures, transition costs, cost savings or other financial implications, enabling investors to better understand how the company is allocating its financial resources and capital in response to climate-related matters,” she explained.

There should also be greater connectivity between sustainability disclosures and the financial statements.

“Investors are likely to look for clearer alignment between sustainability targets, climate strategies, business plans and the assumptions reflected in the financial statements, allowing for a better understanding of the overall financial implications of climate-related risks and opportunities,” Koh said.

Decarbonisation commitments

Judging from the FY2025 sustainability reports, how ready are Corporate Malaysia in terms of actual decarbonisation?

Koh observed that while many listed companies are more actively discussing decarbonisation commitments, a significant number of companies still appear to be at the target-setting and disclosure-building stage.

A small group of leading companies, particularly larger listed issuers and companies operating in more carbon-intensive sectors, are beginning to develop more credible and structured transition plans, she noted.

These companies are gradually providing more detailed disclosures on decarbonisation strategies, renewable energy adoption, emission reduction initiatives, governance structures and transition-related investments.

“At the same time, a larger group of companies are still focused on building foundational capabilities, such as establishing GHG emissions inventories, improving the quality of emissions data, strengthening reporting systems, and enhancing internal governance and controls over climate-related information,” she said.

In many cases, Koh added, the decarbonisation journey disclosed by companies remains relatively high-level, with transition pathways still underdeveloped and execution details remaining limited.

“While many companies disclose net-zero ambitions, renewable energy aspirations and climate commitments, fewer companies currently provide sufficiently detailed information on how those targets will be achieved in practice.”

The NSRF is expected to accelerate improvements in this area, Koh said, with the enhanced reporting requirements likely to drive more structured climate governance, stronger integration of sustainability considerations into corporate strategy and financial planning, and more credible and decision-useful transition planning over time.