WHILE investors remained obsessed with what is going on in the United States with respect to its economic data points, its yield curve, and the US Federal Reserve (Fed) decision to leave the Fed Fund Rate unchanged at 5% to 5.25%, little focus has been paid across the Pacific, and specifically, on the world’s second-largest economy.

While the Fed is likely to keep rates higher for longer, China is keeping rates low, in the absence of inflationary pressure and to support its “ailing” economy as well as due to the weakness of the property market.

Not only that, China remains committed to keeping the tap running with more stimulus packages to sustain economic momentum as the country is focused on delivering economic growth of at least 5% this year.

How long will China keep rates at this level or whether it has room to lower benchmark rates even lower remains a guessing game for now.

Encouraging GDP growth

While the United States reported better-than-expected gross domestic product (GDP) growth for the third quarter (3Q) at 4.9%, China did not disappoint with a similar pace of growth in the same quarter, beating market expectations of a 4.6% increase.

However, a distinction must be made as the US 3Q growth was a quarter-on-quarter (q-o-q) annualised rate while the Chinese data was a year-on-year (y-o-y) increase.

Hence, the two data points are not comparable. For a similar comparison, the US economy, measured on a y-o-y basis, expanded by 2.9%.

For China, riding on the strong tailwind from 1Q data, the Chinese economy expanded by 5.2% for the first nine months of 2023, ahead of the government’s estimate of 5% growth for this year.

Meanwhile, the International Monetary Fund (IMF), in its recent review of the Chinese economy, upgraded its forecast this year with a growth rate of 5.4% against the 5% the world body had predicted earlier, citing “strong post-Covid-19 recovery” but at the same time, warned that growth will slow down to just 4.6% next year – which in Chinese terms, means the dreaded “R” word – recession.

Nevertheless, the IMF’s forecast for 2024 is still much better than the previous estimate of 4.2%. Not out of the woods

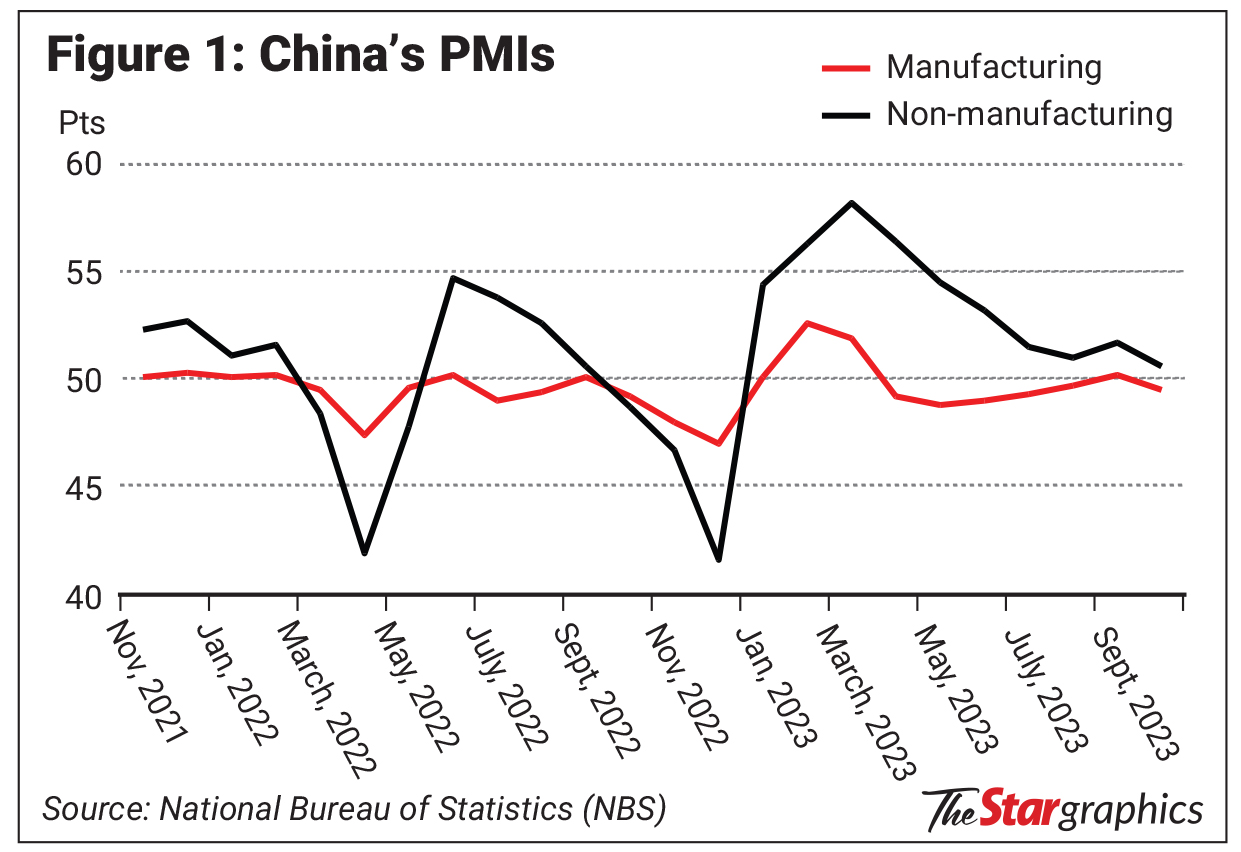

Despite the strength in 3Q GDP data, the recent weakness in the official Purchasing Managers’ Index (PMI) remains a concern as the October Manufacturing PMI dipped below 50, a sign the world’s manufacturing hub is back into contraction while the Non-Manufacturing data, which was at just 50.6, was the lowest this year as seen in Figure 1. In fact, on the external front, Chinese data is also showing a mixed picture with the latest October 2023 exports coming in below expectations with a contraction of 6.4% y-o-y but imports were ahead of forecast, rising by 3% y-o-y.

Stronger retail sales

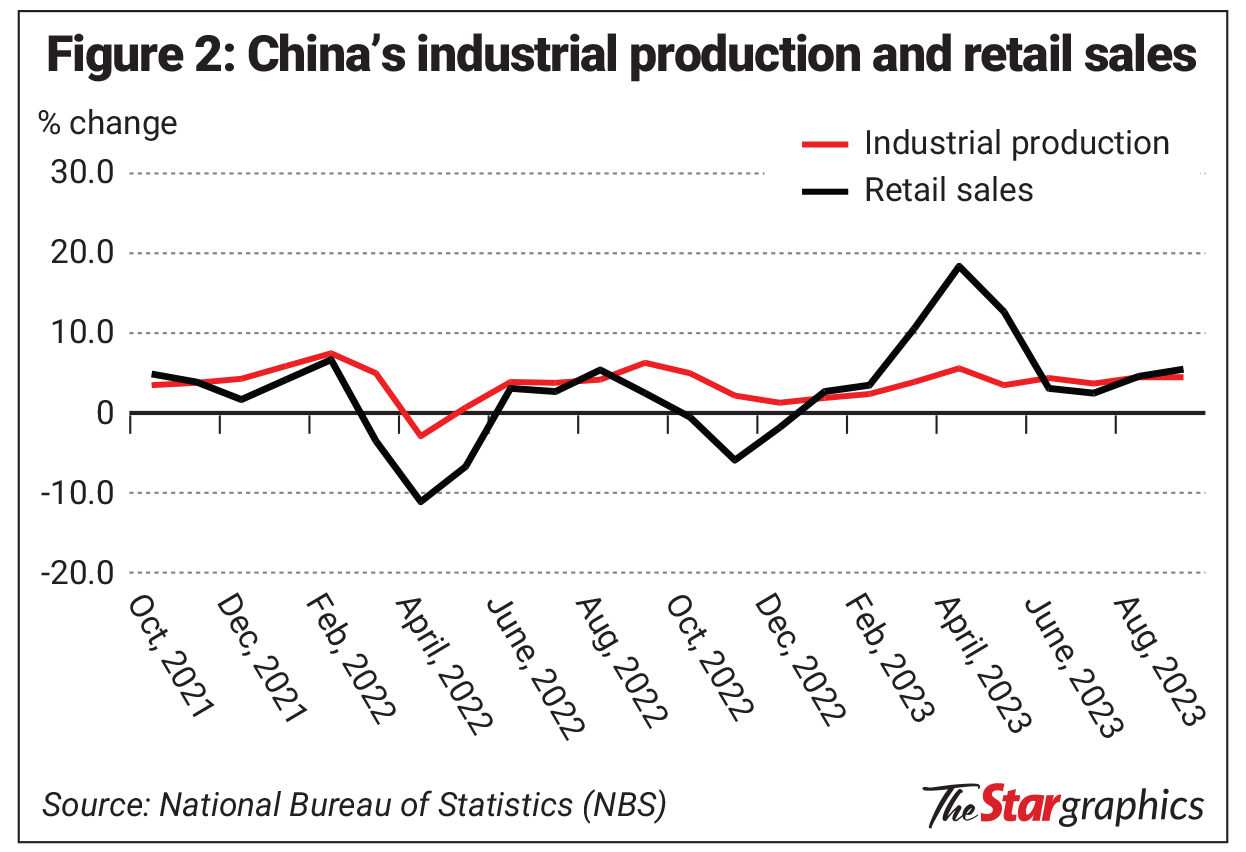

After the initial euphoria after the re-opening of the Chinese economy post-pandemic, industrial production and retail-sales data were closely watched numbers.

As expected, after the initial revenge spending, which saw retail sales rising double-digits y-o-y in the months of March to May, the momentum was lost thereafter as new worries rattled Chinese consumers, especially in relation to the fragile property market.

Retail sales, which slowed to growth of just 2.5% in July 2023, have since rebounded and the September 2023 growth of 5.5% was not only better than expected but showed resilience after the rebound in August. Similarly, industrial production data showed positive promise as the latest Sept 2023 growth of 4.5% matched the previous month’s pace, as seen in Figure 2.

The biggest drag

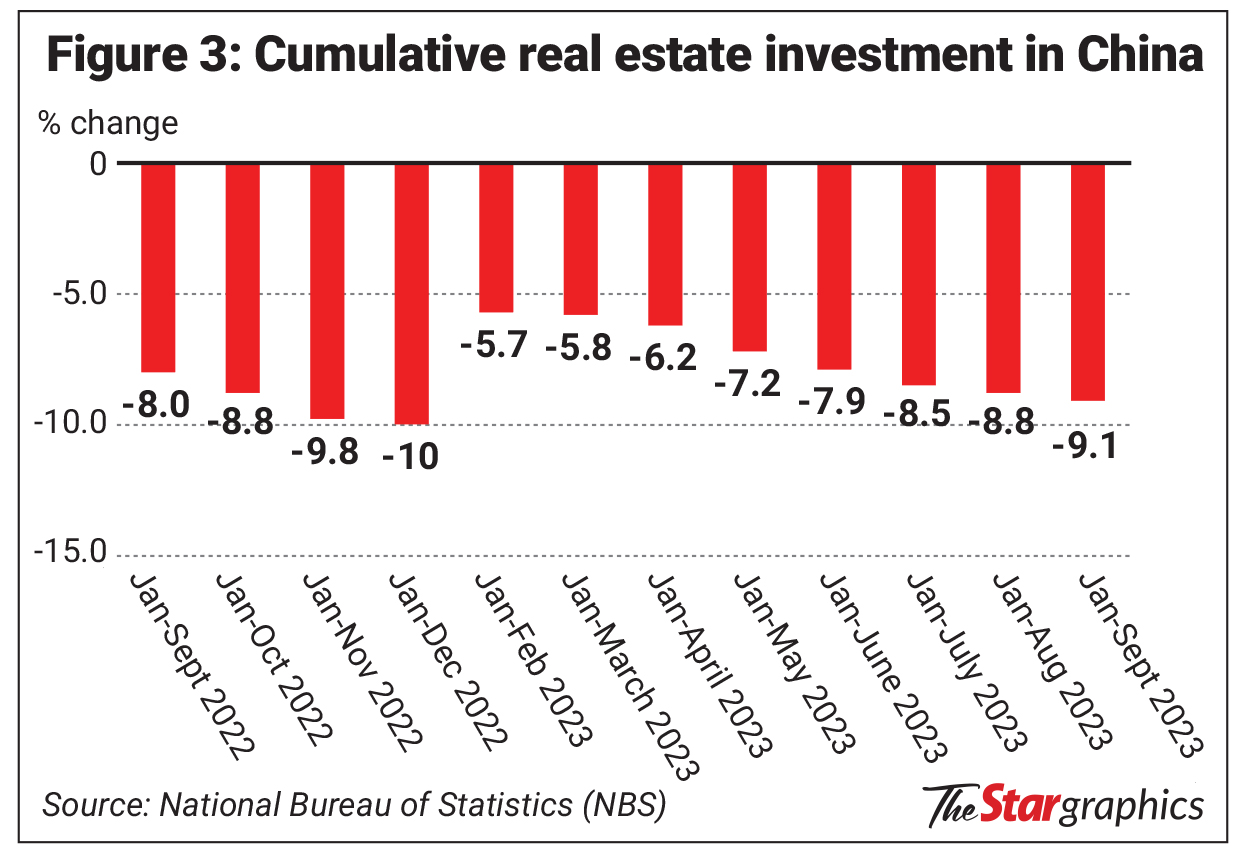

The Chinese property market is the biggest drag on its economy as the sector has remained in contraction for the longest time.

For the first nine months of this year, cumulative real estate sales are now down by 9.1% y-o-y to just 8.73 trillion yuan, as seen in Figure 3.

The troubles at companies like Country Garden and Evergrande, which are saddled with huge debts, have caused a loss of confidence in the real estate market.

Beijing’s effort to restore confidence in the market, by not only lowering mortgage rates, reducing the down-payment thresholds, and easing requirements for first-time home buyers, will take time to see results as investors or home buyers adopt a wait-and-see attitude.Yuan woes

Between December 2021 and August this year, the People’s Bank of China (PBoC) has lowered its benchmark one-year Loan Prime Rate by 40 basis points to 3.45% – the only central bank to lower rates, in its effort to boost lending activities and to support growth of the economy, resulting in its currency taking a hit against the mighty US dollar.

Year-to-date, both the Chinese yuan onshore and offshore rates are down by about 5.6%, and off the lows that were seen just about two months ago when the currency hit a fresh 16-year low.

The recent Fed move to hold the benchmark Fed Fund Rate unchanged for the second time in a row, provided some relief not only for the yuan but also to other regional currencies, including the ringgit.

Year-to-date, the US Dollar Index itself is now up by 2%, which suggests that the balance weakness on the yuan is related to the yield spread between the United States and China as well as weakness in the Chinese economic data points.

What Next?

The confidence shown by the IMF in upping its forecast for China for this year and 2024 shows that the Chinese economy may have turned the corner and is poised to show a strong showing for the 4Q period.

Whether this will roll over into next year remains a wild card for now as it will largely depend on the pace of “recovery” that we are observing in some of the Chinese data points and whether they are sustainable.

Positive momentum will not only be good for the world’s second-largest economy but also Asean economies, especially export-dependent countries like Malaysia.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.