WHEN the US Federal Open Market Committee (FOMC) met in December, the guidance given to the market was that the US Federal Reserve (Fed) had revised its guidance with a 75-basis-point (bps) cut in the Fed Fund Rate (FFR) this year from the current rate of 5.25%-5.50% range, based on its latest dot plot.

The minutes of the meeting released this week also showed that the Fed was rather concerned of a move to cut rates too soon for fear that the expected lower inflation rate is sustainable.

The Fed indicated that no cuts would be coming until the FOMC had “greater confidence” that inflation was indeed falling. In essence, the Fed did not want to cut rates too soon for fear it may have misjudged the inflationary pattern.

Meanwhile, the market was more optimistic with the view that the FFR will be lowered by as much as 150 bps cut this year to end the year at 3.75%-4.00%, as the Fed was expected to cut rates six times on a measured basis, starting from its March 2024 meeting onwards.

Reason – the market expects the core Personal Consumption Expenditure (PCE) rate to be much lower than the guided median rate of 2.4% this year.

The market was right when the December 2023 core PCE came in at 2.9% year-on-year (y-o-y), suggesting that the Fed is well on the way to meeting its 2% core PCE target, which is the preferred measure for inflation, as the three-month and six-month annualised rate dropped to just 1.5% and 1.9% y-o-y.

However, by the time when the headline and core Consumer Price Index (CPI) was released middle of last week, market bets changed drastically.

The headline CPI for January 2024 hit 3.1%, much higher than the market’s expected annual increase of 2.9% y-o-y, while core inflation stayed stubbornly high at 3.9% y-o-y.

Although the January 2024 headline data was lower than the preceding month’s print of a 3.4% increase, the pace of decline in the data was rather disappointing, causing investors to reduce their bets on the number of rate hikes as well as the timing of it.

To make matters worse, another gauge, the US Producer Price Index, which measures prices at the factory gates, rose by 0.9% y-o-y in January 2024, and hence this caused investors to remain cautious as to the number of rate cuts this year.

From six to three

Given the above data, the Fed Fund Futures is now pricing in only three rate cuts with the first 25-bps rate cut only expected to occur in the FOMC’s June meeting. That too, the market is now giving a 54.1% chance.

Another 25-bps rate cut is expected in the September meeting while the last 25-bps cut is forecast to occur in the November meeting. The FFR is now projected to end the year at 4.50%-4.75%, as guided by the Fed.

Dollar bulls

With the market changing its stance on the pace and timing of rate cuts this year, it is of no surprise to witness how the US dollar has outperformed perhaps every major currency, including the ringgit, based on the key economic data that has been presented over the past few weeks.

The Dollar Index, which ended 2023 at 101.38 is now up 2.5% year-to-date and was last seen at 103.94.

Naturally, this also suggests that most currencies have weakened against the mighty dollar this year with losses ranging from less than 1% to as much as 6.7% on the Japanese yen as of Thursday’s closing levels.

The ringgit too has weakened considerably and is now down 4% against the greenback and weaker by 2.4% against the Singapore dollar.

Against other major currencies, the ringgit is down 3.7% against the British pound, 2.8% against the yuan, 2.7% against the Indonesian rupiah, 2.2% against the euro and 0.4% against the Australian dollar since the start of the year.

Nevertheless, the ringgit has strengthened against the yen by 2% and by 0.5% against the Thai baht.

More pain ahead?

Last week, Malaysia reported a lower-than-expected fourth-quarter 2023 (4Q23) gross domestic product (GDP) growth of just 3% against a forecast of a 3.4% growth, bringing last year’s full-year GDP growth to just 3.7%, well below even from the low-end of the 4%-5% growth estimated for 2023.

The final 4Q GDP data was also lower than the advanced estimate that was released by the Statistics Department less than a month ago, and weaker than the preceding quarter’s 3.3% y-o-y growth.

The 4Q23 GDP was also disappointing as Malaysia recorded a contraction of 2.1% on a quarter-on-quarter (q-o-q) basis, much larger than the last quarterly contraction of 1.7% seen in 4Q22.

The key weakness in the economy was observed in the manufacturing sector, which reported a 0.3% y-o-y contraction in 4Q.

On the demand side, private sector aggregate demand, which accounts for 76% of the economic pie, slowed to just 4.2%, mainly dragged by lower private investment, while net exports contracted by a staggering 35.6% y-o-y, contributing a negative 1.7 percentage point decline in the 4Q23 period’s 3% y-o-y growth.

For now, most economists are maintaining the GDP forecast for Malaysia at between 4.5% and 5% for 2024, mainly driven by expectations of a recovery in the external sector, lower global interest rates as well as inflation pressure, while domestic catalysts too are aplenty mainly driven by a host of government’s incentives coming from Budget 2024.

Malaysia got the ball running in terms of a better 2024 as exports for January surged 8.7% y-o-y. However, as imports jumped by 18.8% y-o-y, Malaysia recorded a much lower trade surplus of just RM10.1bil, down a whopping 44.2% y-o-y.

Hence, the “what if” scenario is still playing out as potential higher-for-longer US interest rates and other hawkish tones from major central banks may cause aggregate demand to be slower than expected, while weaker net exports may drag overall GDP growth yet again.

Will Bank Negara cut?

The consensus view for now is for Bank Negara to leave the current overnight policy rate (OPR) at 3% unchanged for the rest of the year.

In the January Monetary Policy Statement, the committee reckoned that the global growth outlook remains subject to downside risk, mainly from higher-than-anticipated inflation outturns, geopolitical tensions and a sharp tightening in financial market conditions.

Nevertheless, the committee viewed that the current OPR remains supportive of the economy and is consistent with the current assessment of inflation and growth forecast.

The words deployed in the statement suggest that Bank Negara is cautious on the outlook and with the 4Q GDP coming in outside the expected range, the downside risk to growth this year has increased.

With inflation expected to moderate this year and if growth slows to less than 4% in the coming one or two quarters, there is an even chance that the central bank may cut the OPR by 25 bps and if economic conditions worsen further, there is a chance of another 25-bps rate cut in the fourth quarter this year.

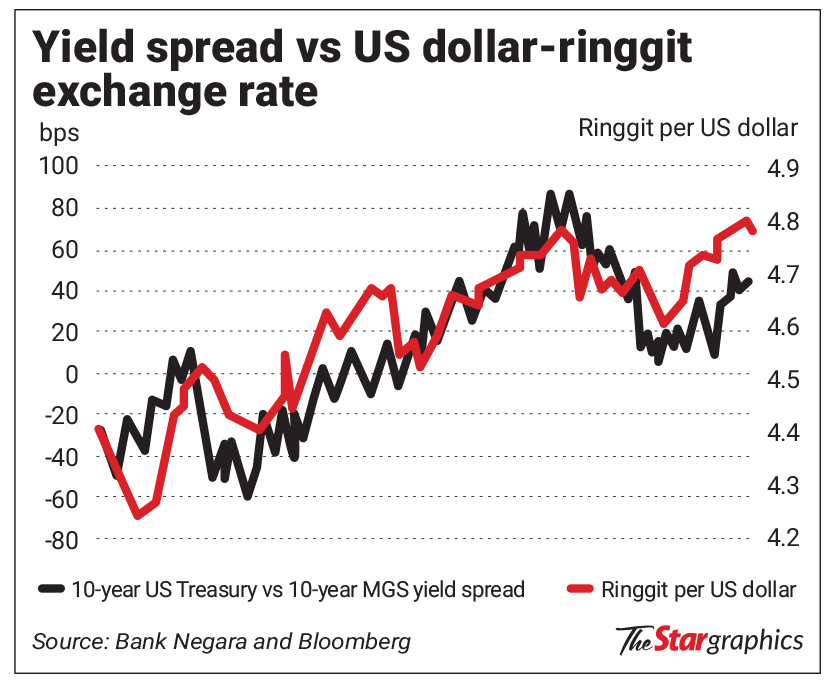

With the Fed now expected to stay the course in terms of three rate cuts and as echoed by the market, Malaysia’s potential move of also cutting the OPR may leave the spread between the 10-year Malaysian Government Securities and the 10-year US Treasuries persistently high as seen in the accompanying chart.

The chart also shows that there is a strong correlation between the spread of the 10-year sovereign papers and the US dollar-to-ringgit exchange rate, with a correlation coefficient of 83%.

Based on this scenario, the US dollar will remain elevated, which in turn will see the ringgit remaining under pressure for a longer period.

Will we see a big handle of 5.00 against the greenback in the coming days or weeks will very much depend on the market’s anticipation of whether the 10-year US treasury papers are headed higher or lower, which indirectly would be re-priced depending on incoming economic data points.

While the spread between the two benchmark yields is one of the factors that is causing the ringgit to weaken, there are other factors too, which this column has highlighted before.

This includes the large deficits that we have observed in errors and omissions in our balance of payments, the weak financials of the government, the slow pace of reforms, low tax collection, high perceived corruption as well as dwindling current account surplus and massive outflows due to direct investments abroad and portfolio outflows.

Given the above scenario, while most market watchers agree that the ringgit is grossly undervalued and should appreciate when global interest rates normalised, the big handle of 5.00 on the US dollar-ringgit exchange rate cannot be discounted after all.

Perhaps Soros will be right, finally – a quarter of a century later when he first predicted the ringgit’s misfortunes.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.