MUCH has been debated as to the cause of the ringgit’s weakness. Despite the promise of reforms, as well as the baby steps introduced in Budget 2024, the ringgit continues to head south, vis-a-vis the mighty US dollar.

The differential in the US interest rate and Malaysia’s is also well documented and has been a triggering factor for the ringgit, while China’s loose monetary policy has had a damaging impact on the Malaysian currency, as the Chinese yuan, as recent as two months ago, was flirting at near 16-year lows.

Volatility in financial accountWhile Malaysia continues to show positive current account and overall balances, the breakdown of our balance of payment account shows a different picture. Based on data provided by Bank Negara, Malaysia recorded a net outflow of RM254.6bil in its financial account between 2010 and September this year as can be seen in Chart 1, with the biggest outflow seen in 2014 where some RM80bil left Malaysian shore and in 2020, when some RM77.4bil left the country.

DIA offsets FDI Inflow

Malaysian investing overseas is nothing new. Statistics for the third quarter of 2023 (3Q23) showed that domestic investment abroad (DIA) totalled some RM13.4bil, bringing the year-to-date total to RM22.5bil.

Compared to a year ago, when DIA stood at RM30.1bil, the amount for the first nine months was lower by RM7.6bil or 25.2%.

Thanks to net foreign direct investment (FDI), which totalled RM7.2bil in 3Q23 and RM22.3bil in the first nine months of 2023, direct investment registered a net outflow of RM6.1bil and just RM0.1bil in 3Q23 and in the first nine months of 2023, respectively.

This is a huge decline compared to the first nine months of 2022, where direct investment registered a net inflow of RM25.2bil, thanks largely to a strong net FDI of RM55.4bil against DIA of RM30.1bil.

From 2008 up to the end of 3Q23, Malaysia has recorded a total DIA of almost RM574bil and during the same period, some RM547.4bil in FDIs were received.

Interestingly, between 2008 and 2014, FDI inflows outpaced DIA with a total net direct investment inflow of approximately RM122.1bil.

But since 2015 and up to 3Q23, the DIA outflow has been stronger than FDI inflows, as Malaysia registered net direct investment outflow of RM96.6bil.

Big drag

While DIA has been a drag since 2015, the portfolio flows are another story altogether.

For 3Q23 alone, Malaysia recorded a portfolio outflow of RM14.1bil, of which some RM15.4bil were related to outflows carried out by residents while non-residents recorded an inflow of RM1.3bil.

The 3Q23 outflow was a strong reversal of the RM0.5bil inflow that was recorded for the same period last year.

For the first nine months of this year, Malaysia saw total portfolio outflows of RM39.3bil, a RM10bil year-on-year increase from the outflow of RM29.3bil last year.

In terms of breakdown, residents recorded an outflow of RM41.9bil, while non-residents recorded an inflow of RM2.6bil.

While most market watchers have been rather focused on looking at foreign portfolio flows, in reality, it is the residents’ portfolio flows that have been a big drag.

Between 2010 and up to 3Q23, portfolio outflows made by residents totalled RM394.6bil, with some RM215.7bil or 54.7% of it, occurring between 2020 and 3Q23.

This was of course offset by non-resident portfolio inflows, which amounted to RM232.6bil between 2010 and the last reported quarterly period.

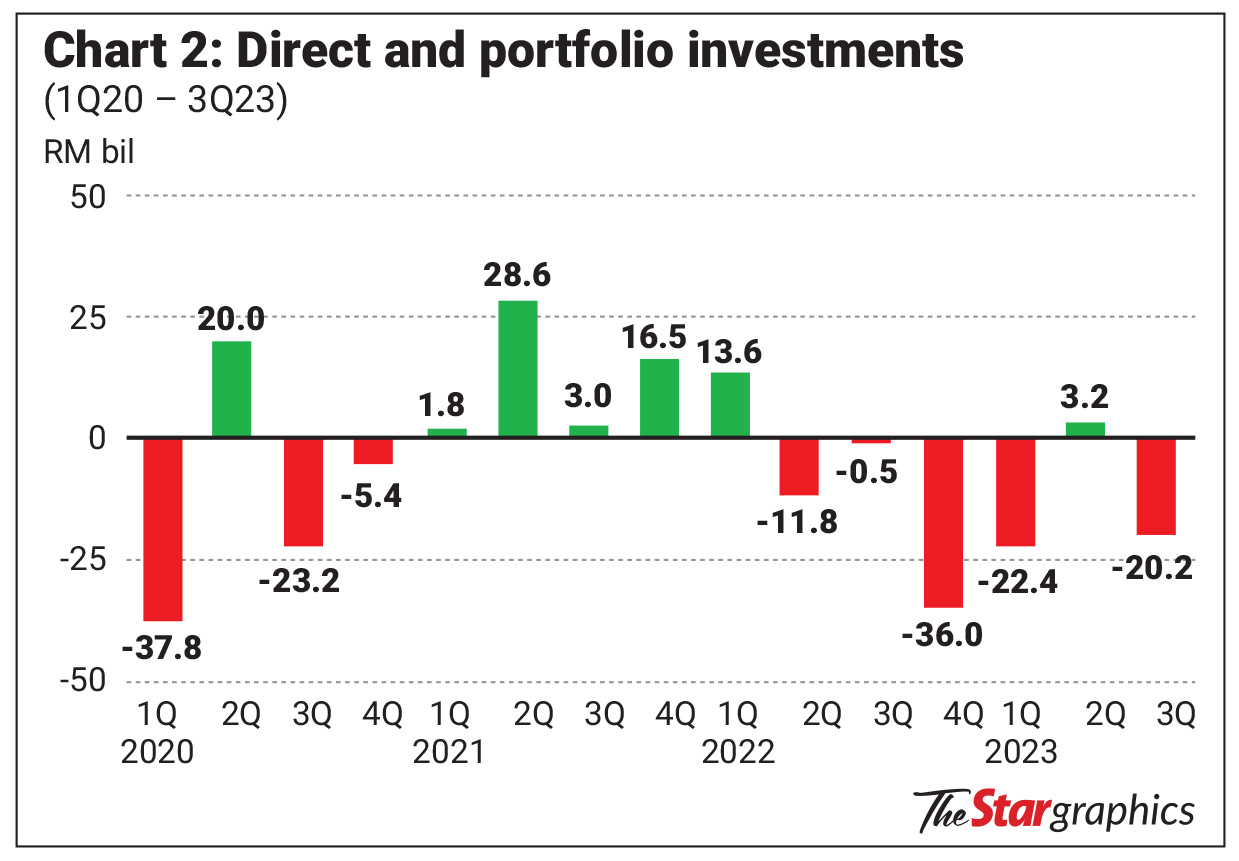

Taken together, direct investments (comprising of DIA and FDI) and portfolio flows (from both residents and non-residents), one would note that over the space of 13 years and into the first nine months of this year, Malaysia recorded total net outflows of RM139.2bil, but more importantly, this was mostly prevalent after 2013 where Malaysia recorded total outflows of almost RM230bil, somewhat cushioned by the strong RM49.9bil inflow in 2021.

Chart 2 summarises the total direct investment and portfolio flows between 1Q20 and 3Q23.

“Other Investments” is another element within the nation’s financial account and the flows here too have been erratic, which has seen a total outflow of some RM109.1bil between 2010 and the first nine months of 2023.

However, thanks largely to an inflow of RM49.2bil in 2022 and RM40.4bil up to September 2023, the overall picture is less worrying, as these inflows cut the overall outflow by 45%.

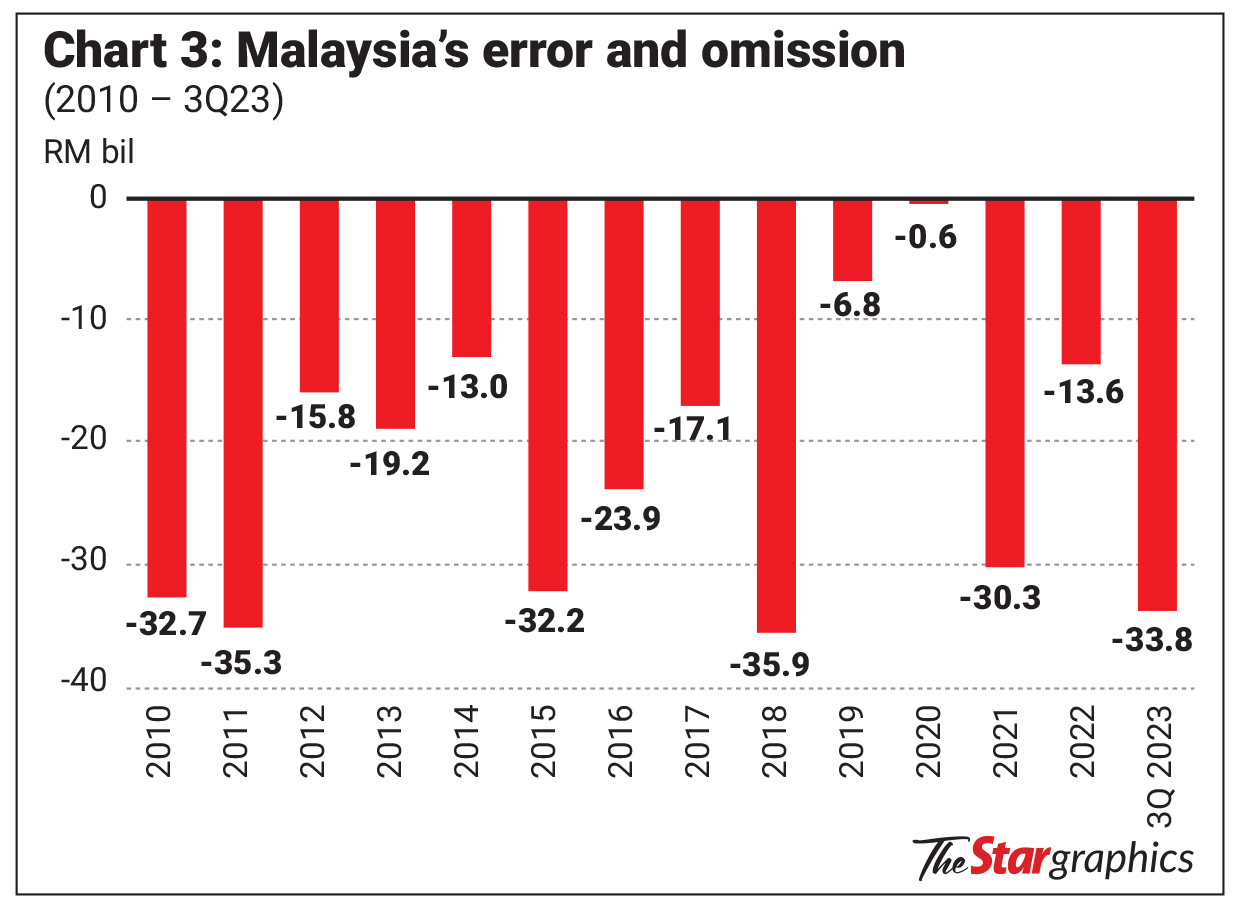

Staggering errors, omissionsAnalysing the nation’s balance of payment, there is another mystery in the form of “errors and omission” (E&O) that either allows Malaysia to record an overall surplus or deficit.

Between 2010 and 3Q23, E&O recorded a deficit of RM310.4bil as seen in Chart 3.

E&O has always been a drag this year with the latest nine months cumulative figure at RM33.8bil.

In balance of payment calculations, E&O appears as a balancing figure as the final surplus or deficit of the government’s finances is the result of all inflows and outflows.

Trade surplus

Malaysia is fortunate to be running huge trade surpluses which has helped the nation to record consistent current account surpluses.

Of course, the nation continues to see deficits in the services sector and primary and secondary incomes.

While our capital account is relatively non-contributor, the balances in the financial account and E&O are the keys to maintaining a healthy balance of payment surplus as highlighted earlier.

In conclusion, while Malaysia sees consistency in terms of maintaining a healthy balance of payment and current account surpluses, the nature of flows in other investments and E&O are worrying as it shows that there are significant uncaptured outflows, which is perhaps a reason for the ringgit weakness since 2010 when the ringgit was then trading at about RM3.20 to the US dollar.

In addition, there have been numerous studies done on the impact of 1Malaysia Development Bhd on the Malaysian portfolio flows and clearly, the flows seen in DIA and FDIs show that DIA accelerated post-2015, which probably also explains the impact on our ringgit.

Another contributing factor is also the outflows made by our institutional funds overseas as the local domestic capital market is not large enough for them as well as for diversification purposes. The statement made by the Deputy Finance Minister II in Parliament early this week showed that the market value of the top six government-link investment companies was worth some RM522bil in value perhaps explains some of the reason for the strong outflows seen made by residents as captured in the financial account of the balance of payment statement.

Pankaj C Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.