BASEL III or the third Basel accord was introduced in 2010 to ensure banks remain strongly capitalised and had enough liquidity to face any future financial crisis. The framework is to be implemented progressively across different countries between 2013 and 2019.

The latest accord is a continuation and a more stringent ruling to strengthen the banking regulatory framework under Basel I and Basel II.

The fall of Lehman Brothers Holdings Inc during the 2008-2009 financial meltdown triggered by the subprime mortgage crisis in the United States reverberated to other markets causing regulators to tighten their grip on their economies.

Unlike the United States and Europe, the Asian markets were relatively in a better position, thanks to the measures that had been put in place earlier by the regulators to strengthen the risk management and supervisory capabilities to battle the Asian financial crisis.

Not wanting to take any chances, the Basel Committee on Banking Supervision imposed stricter measures under Basel III to ensure banks were ready to handle any crisis that could affect their capital position by increasing bank liquidity and decreasing bank leverage.

The Basel III guidelines were designed to improve the banking sector’s ability to absorb shocks arising from financial and economic stress, improve risk management and governance and fortify the sector’s transparency and disclosure standards.

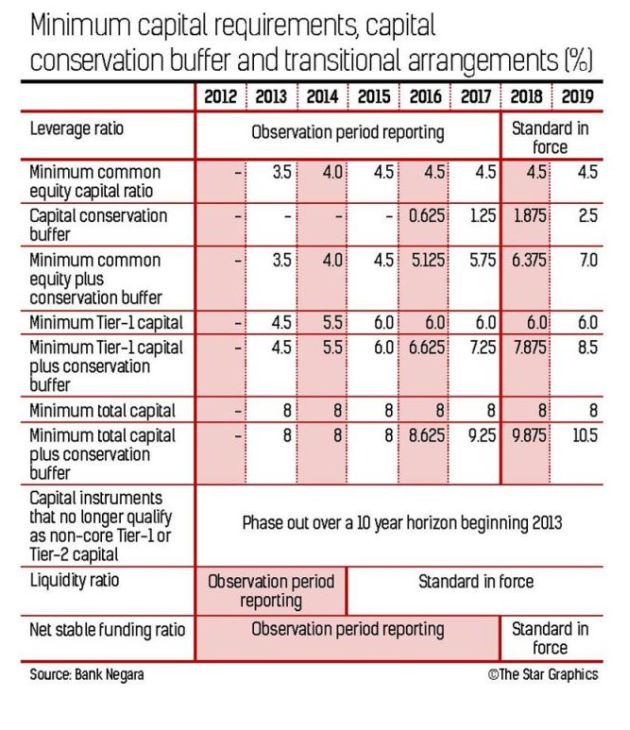

Malaysian banks started embracing the Basel III accord in January 2013 subject to further announcements by Bank Negara. The deadline for full compliance is in 2019. The new guidelines imposed higher capital requirements with capital buffers as well as leverage and liquidity ratios.

The implementation of the higher capital requirements, that started last year is a gradual process that goes on until 2019 (see table).

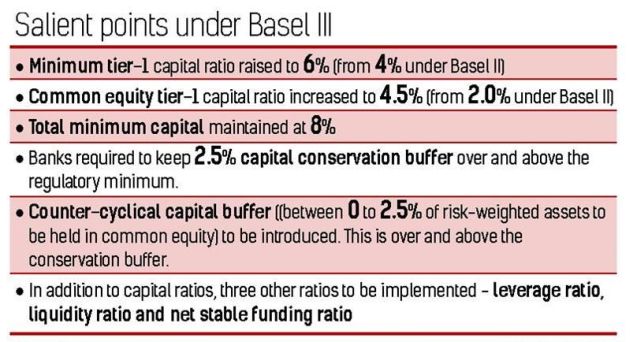

The minimum tier-1 capital ratio has been raised to 6% from 4% under Basel II and common equity Tier-1 capital ratio to 4.5% from 2% under Basel II. Total minimum capital has been maintained at 8%. In addition, banks are required to keep 2.5% capital conservation buffer over and above the regulatory minimum.

Analysts contacted by StarBizWeek say the recent cash call by Public Bank to raise up to RM5bil to beef up its capital base could see more banks following suit albeit not in the immediate term. They also agree that more banks could alternatively roll out dividend reinvestment plans (DRP) to boost their capital base under Basel III as well as issue capital instruments like Tier 1 or Tier 2 subordinated bonds or sukuk which are Basel III-compliant.

HwangDBS Vickers Research banking analyst Hon Seow Mee says Malaysian banks on the whole have complied with Basel III capital requirements (with transitional provisions).

Their current capital positions are equipped to meet Basel III capital requirements up to 2015, she says, adding that there may be concerns when the counter-cyclical buffer (0-2.5% of risk weighted assets) is determined after 2015.

Banks may decide to pre-empt this and resort to some form of capital raising in the future either in the form of share placements or rights issues.

EY Malaysia financial services and country leader of financial accounting advisory services partner Chan Hooi Lam concurs with Hon on Malaysian banks being well capitalised.

He feels due to various reasons, banks are expected to constantly look for avenues to raise their capital base, not only at common equity Tier 1 (CET-1) level but also Tier 1 and total capital levels. “Besides raising equity via issuances of shares, other capital instruments, example Tier 1 or Tier 2 subordinated bonds or sukuk which are Basel III-compliant (with loss absorption features) have been issued or planned for,’’ he notes.

Alternatively, to address capital requirements Hon and other analysts agree that other banks could roll out DRPs to conserve cash to strengthen their capital base.

To date, banking groups like Maybank, CIMB and RHB have undertaken DRPs and AmBank Group could also follow suit as it has the mandate to do.

so besides other banks. A DRP allows investors to reinvest their cash dividends by purchasing additional shares or fractional shares on the dividend payment date.

Related stories:

Teh’s extra oomph for Public Bank

Quah’s appointment quells concerns on succession

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.