PETALING JAYA: Malaysia may need a realistic approach to classifying household income as the current B40, M40 and T20 framework fails to account for differences in living costs, household size and debt burdens, say experts.

Households earning the same income could also face vastly different financial pressures depending on where they live, said Federation of Malaysian Consumers Associations chief executive officer Dr Saravanan Thambirajah.

“A household earning RM15,000 in Kuala Lumpur or Penang may face very different financial realities compared to a household with the same income in smaller towns or rural states,” he said.

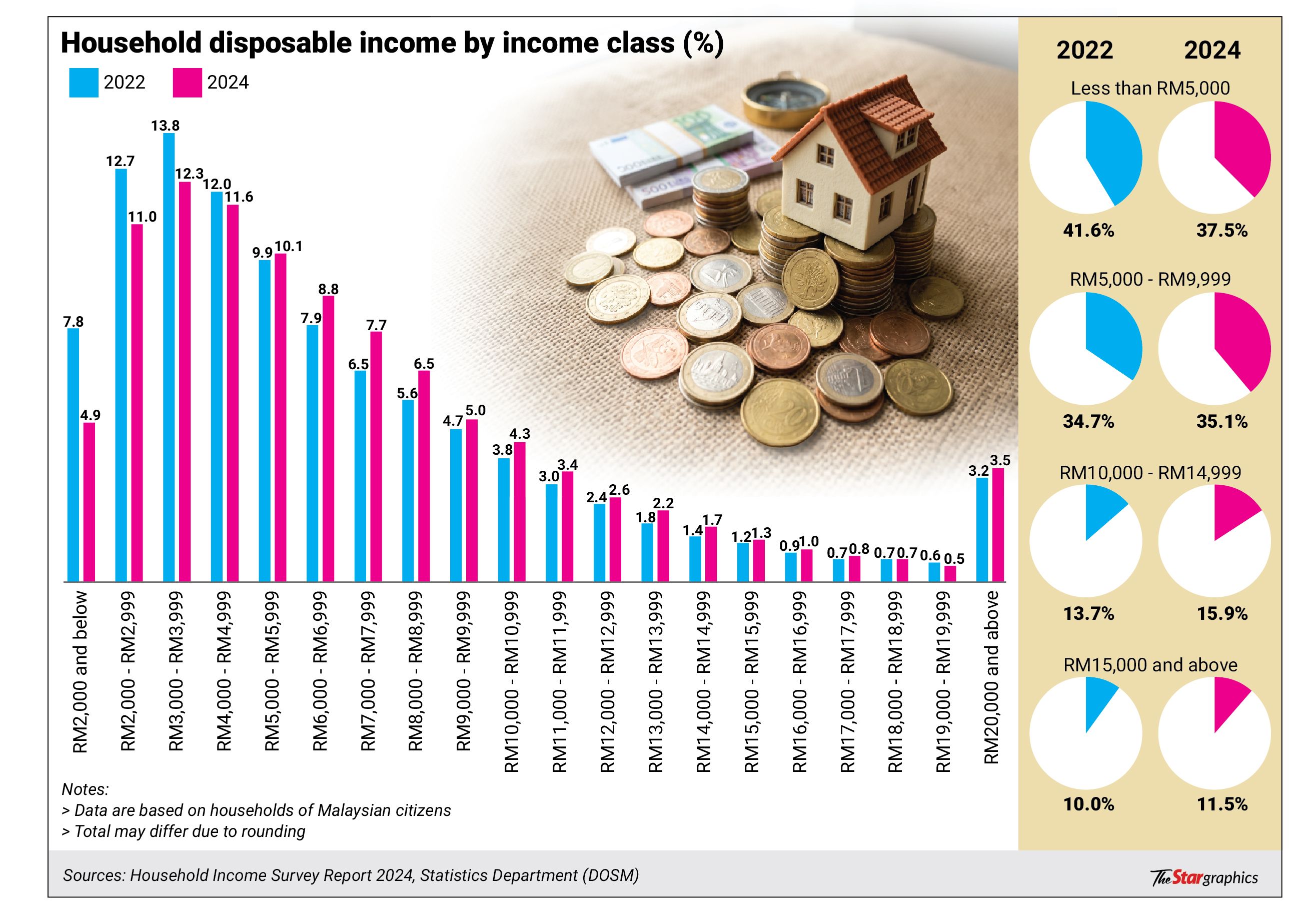

Under current classifications, a household with more than RM12,680 income is considered T20, while those in the B40 are households with income less than RM5,000 a month.

Saravanan said income classifications should be tailored according to regional living costs instead of being applied uniformly nationwide.

ALSO READ: Some T20 families living paycheque-to-paycheque

He suggested that the T20 threshold in the Klang Valley, Penang and Johor Baru be between RM16,000 and RM18,000 in monthly household income, while for major urban centres in Sabah and Sarawak, it could range between RM14,000 and RM16,000.

For smaller towns and rural areas, he said the threshold could be between RM12,000 and RM14,000.

He added that income classifications should also consider household size, debt commitments and disposable income instead of relying solely on gross salary.

Socio-Economic Research Centre executive director Lee Heng Guie said the current gross income classifications of T20, M40 and B40 do not accurately reflect real financial capacity.

“While gross income is used as a standard metric largely for tax purposes, it is misleading for understanding actual financial capability or net disposable income,” he said.

The issue arose after a government proposal to review RON95 petrol subsidies for the wealthy, specifically those in the T20 bracket.

“Gross income should not be the sole indicator of financial freedom or financial strength as it does not account for taxes, fixed expenses, debt payment and high cost of living that reduce disposable income and discretionary spending,” said Lee.

“Additionally, the geographical location – between states, cities as well as rural – and also the number of dependents (parent and children) with rising living costs would also affect the financial standing of a working family,” he said.

Majlis Amanah Rakyat (Mara) chairman Datuk Dr Asyraf Wajdi Dusuki also said the definition of the T20 category must be handled carefully as it often fails to reflect the actual financial burden of a household.

He said those with a household income of RM13,000 in cities like Kuala Lumpur could effectively fall into the M40 or even B40 groups.

“Mara takes all these factors into account before approving financing. For example, consider a couple who are both teachers earning RM6,500 each.

“When combined, they have a household income of RM13,000. If they live in a big city with three children in university and three more in school, consider their monthly expenses,” said Asyraf Wajdi.

Bank Muamalat Malaysia Bhd chief economist Mohd Afzanizam Abdul Rashid said income classification will help policymakers create the right targeted cluster, with assistance directed at the right targeted group.

“This is where having a robust database will help the government distribute financial assistance. Perhaps, MyKad is seen to be one of the main tools,” he said.

“To be honest, it’s difficult to pinpoint the exact ideal income bracket because each household has different financial commitments, and a higher cost of living reduces real income or purchasing power.”