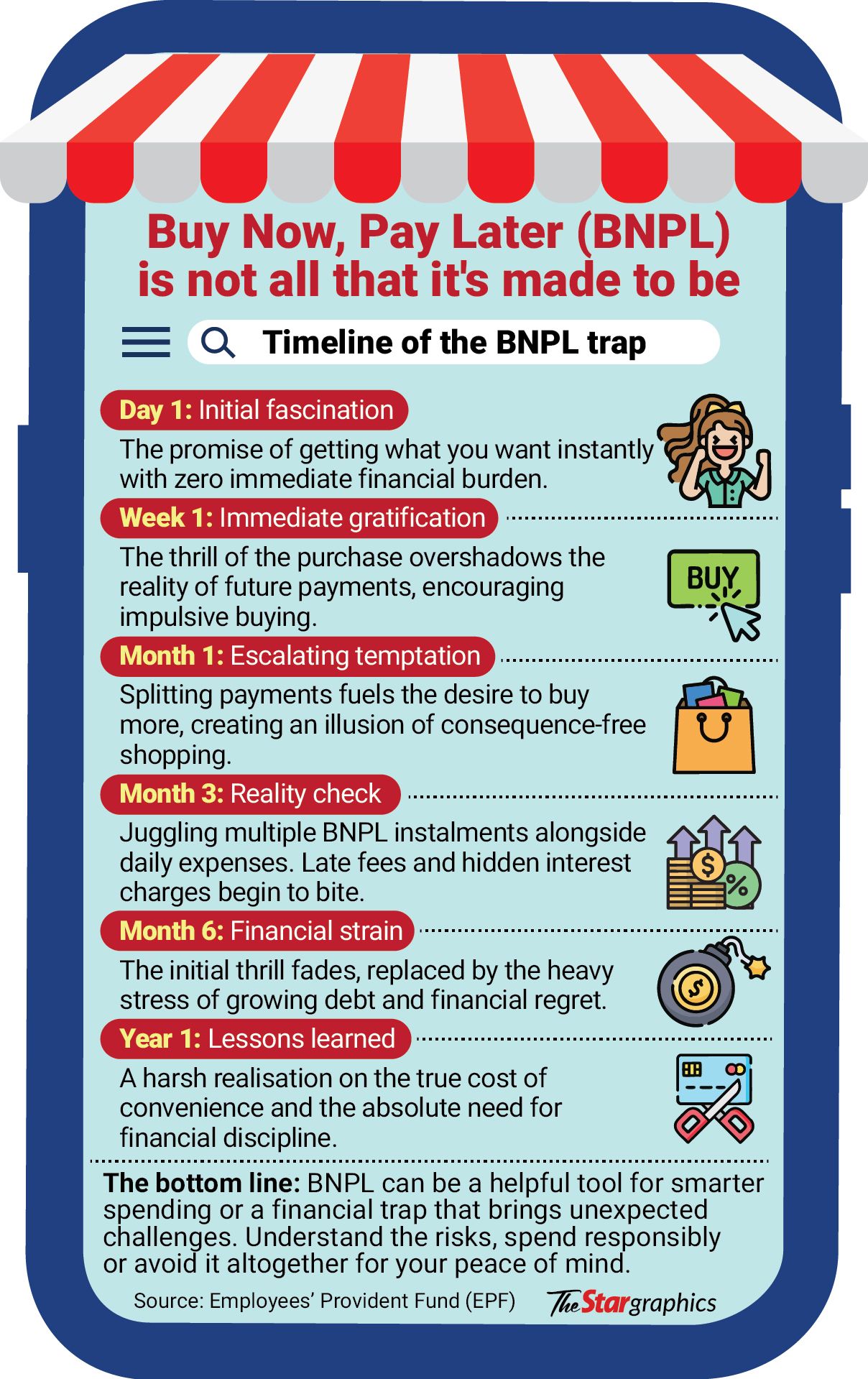

PETALING JAYA: Buy Now, Pay Later (BNPL) services are helping businesses increase sales and manage cash flow, but industry leaders warn that the model can also cut into profit margins and carry risks for both merchants and consumers.

Small and Medium Enterprises Association (Samenta) president Datuk William Ng said the BNPL model is really a double-edged sword for SMEs.

“While it is marketed as a tool to drive growth, the reality is that it often forces a trade-off between volume and margin,” he said when contacted.

“For many SMEs, BNPL helps win the initial sale by reducing the barrier to entry for consumers, effectively lowering cart abandonment rates.

“However, this comes at a significant cost. While the consumer enjoys a seamless, interest-free experience, the merchant is often the one absorbing a Merchant Discount Rate (MDR) that typically ranges from 3% to 5%, and sometimes higher for smaller players.

“In an environment where many SMEs are already struggling with rising operational costs, giving away such a large percentage of the gross transaction value can severely erode net profit margins.”

Ng revealed that the association frequently hears from members that these fees are substantially higher.

SME Association of Malaysia president Dr Chin Chee Seong said BNPL fees are generally manageable and usually lower than commissions charged by major e-commerce platforms.

“BNPL has really helped inrease sales. Providers are charging commissions ranging from 4% to 8%, but most merchants are willing to pay to receive their funds upfront,” he said.

Chin shared that some businesses will likely see a drop in sales if they were to stop offering BNPL.

Ng agrees and said, “If an SME were to stop offering these services today, there is a legitimate fear that sales would drop, particularly among young customers who have integrated BNPL into their budgeting habits.”

Chin added, “It would be better if the commission fees to providers were lower, but that also depends on how much you sell the product.”

Meanwhile, the Malay Businessmen and Industrialists Association of Malaysia (Perdasama) president Mohd Azamanizam Baharon said that while using BNPL credit schemes benefits merchants, it can also cause micro-debt risks to users.

“Merchants have many advantages because it helps customers obtain goods and services through flexible credit facilities such as three-month instalment payment plans.

“Merchants can also use the credit facilities as a form of capital rotation. For example, a trader can apply for RM500 through a platform and use it as business capital to buy raw materials, with repayment made in instalments,” he said.

“From an entrepreneur’s perspective, the BNPL system provides easy credit facilities to customers which help merchants increase sales.”

The sellers will just have to ensure that they pay the amount in instalments, or end up getting charged a late payment fee.

However, Azamanizam warned of the risks of micro debts, where users spend beyond their means, accumulating many small commitments which eventually become large debts.

“Young people are more vulnerable to high indebtedness because the payments initially appear small,” he said.

Previously, the Finance Ministry said there is an increase in the number of BNPL service providers in the market, from 10 in 2023 to 16 providers in 2025.

This is in line with the rapid growth of 243 million transactions worth RM21.3bil in 2025.

“The risks associated with consumer loans under the BNPL scheme remain under control and are expected to stay at 0.3% of the total household debt in Malaysia.

“As of Dec 31 last year, the total loans stood at RM4.9bil while the amount of overdue BNPL is at RM160.2mil or 3.3% of the total of BNPL loans. This figure reflects that the debt burden of BNPL users is manageable,” the ministry said in a written reply to Kubang Pasu MP Datuk Dr Ku Abd Rahman Ku Ismail.