Many Malaysians only discover the limitations of their health insurance when they attempt to make a claim. As new medical plans roll out prompted by reforms, insurance experts share what consumers should look out for in their policy and what they can do if their claim is rejected.

WHEN Anne (not her real name) began experiencing severe abdominal pain last year, she assumed the worst she would have to worry about was the health risks from the surgery her doctor recommended.

The 35-year-old was diagnosed with ovarian cysts and advised to undergo a procedure costing thousands of ringgit, but she felt reassured financially, knowing that she had recently purchased health insurance.

But that relief quickly turned into confusion when her insurer declined part of her claim due to her policy’s exclusions and waiting periods.

“I thought as long as I have health insurance, they will cover any costs for medical issues, but I didn’t realise there were so many terms and conditions,” she says.

Anne eventually paid a significant portion of her medical bill out of pocket while trying to appeal the decision.

As Malaysia prepares to roll out the new base medical and health insurance/takaful (MHIT) plan, which has prompted insurers to introduce upgraded plans with revised terms, conditions and costs, insurance agents and industry representatives say many Malaysians, like Anne, still have only a limited understanding of what their health insurance policies actually cover.

As a result, some policyholders only discover exclusions, waiting periods and coverage limitations when they attempt to make a claim.

The issue has also raised broader questions about what recourse is available to policyholders when their claims are denied.

Not fully protected

One of the biggest misconceptions among consumers is the belief that purchasing a policy means they are fully protected against any medical emergency, says insurance agent Catherine Tan.

“Having insurance and understanding your insurance are two very different things,” she says.

Many frustrations surrounding rejected claims stem from policyholders not fully understanding the limitations of their coverage, she says.

“A lot of it comes down to not understanding the policy well enough. People assume insurance covers everything.

“It doesn’t. Every plan has its own terms, conditions and exclusions, and these differ from one insurer to another.”

Among the most commonly overlooked clauses are waiting periods, exclusions for pre-existing conditions and congenital illnesses, treatment caps and co-payment requirements.

Another insurance agent, K. Shakthi Kumar, says consumers often focus mainly on affordability when purchasing health insurance, without paying enough attention to details such as annual limits, room and board entitlements and exclusions.

“Many people also assume they can purchase coverage after being diagnosed with a medical condition, without realising that pre-existing illnesses are usually excluded or subject to underwriting,” he adds.

Be honest, transparent

Then there are policyholders who run into problems trying to make a claim because they failed to disclose symptoms or medical histories during the application process, says former insurance agent Intan Mas Ayu Shahimi.

Such consumers are usually worried that their application for insurance will be rejected if they disclose their health information, or they do not think it is important.

“If an applicant or policyholder wants to apply for a new policy, they should be upfront. They need to be honest, transparent, and explain all the symptoms they have,” she says.

Life Insurance Association of Malaysia chief executive officer Mark O’Dell notes that industry statistics show that 94% of initial guarantee letters were approved while 97% of final guarantee letters were approved.

“The biggest reasons for decline were non-disclosure of pre-existing conditions or general exclusions,” he explains.

Still, insurers may still offer coverage with additional charges or exclusions instead of rejecting such applications outright, Intan adds.

“There may still be discretion from the insurance or takaful company. They may impose loading, extra charges or exclusions.

“They may provide coverage for other illnesses, but exclude coverage for certain conditions,” says Intan.

Misunderstandings are further compounded by the fact that many consumers never fully read their policy documents after purchasing insurance, she says.

“In many cases, we believe people do not read their own policies.

“When they receive the policy documents, they simply put them away in a cupboard.”

According to O’Dell, exclusions for pre-existing and congenital conditions are disclosed during the point-of-sale process and have to be acknowledged by policyholders before approval.

“The policy disclosure at point of sale contains the list of standard exclusions, which includes congenital conditions.

“The policyholder must sign and acknowledge,” says O’Dell.

He says exclusions are necessary to ensure the sustainability of insurance pools and to prevent premiums from rising further for all policyholders.

Industry players say this is why policyholders need to review and better understand their coverage over time.

Review, prepare, appeal

According to Tan, many consumers treat insurance as a one-time purchase instead of reviewing their policies as their healthcare and financial needs evolve over time.

“When you’re young and just starting out, basic protection might be enough. But as your income grows, so does your lifestyle.”

With many Malaysians still unclear about the extent and limitations of their health insurance, cases like Anne’s are not uncommon.

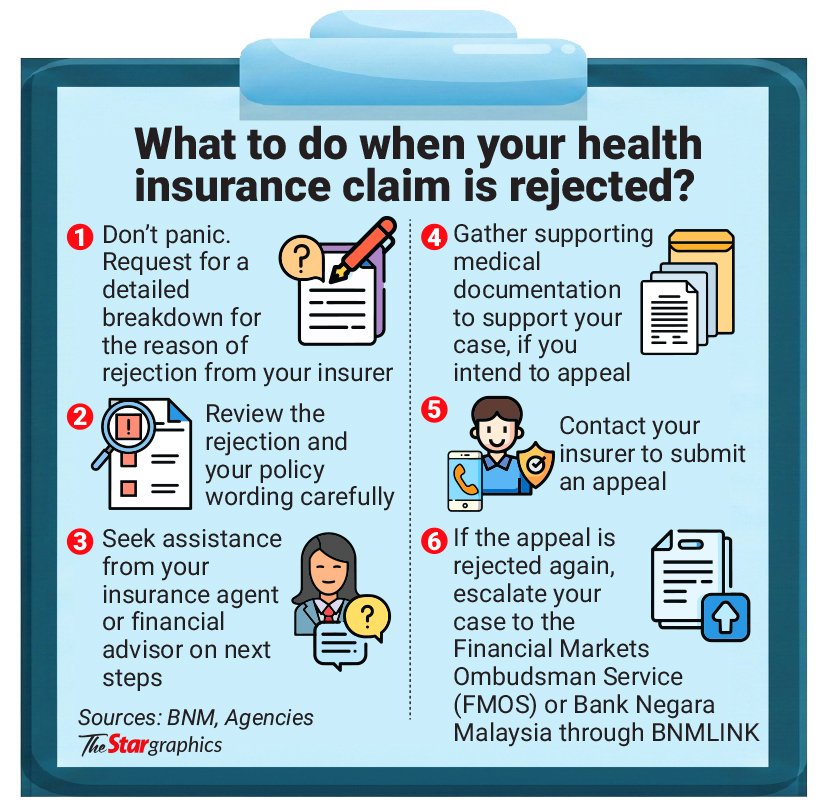

For policyholders whose claims are rejected, agents stress that consumers should first seek a detailed explanation from their insurer or agent before panicking.

“First, don’t panic. Reach out to your agent, get a clear explanation, and explore your options,” says Tan.

Shakthi says consumers should request a detailed breakdown of why the claim was rejected from their insurers as some cases may involve missing documents or requests for clarification rather than outright denial.

“They should then review the policy wording carefully and seek assistance from their agent or financial advisor to better understand the decision and think of possible next steps,” he says.

Tan says policyholders should also gather supporting medical documentation if they intend to challenge the insurer’s decision.

“If the rejection stands, you can appeal. Get supporting documents, a letter from your doctor if needed, and make your case,” she says.

Consumers who remain dissatisfied after exhausting the insurer’s internal dispute process can escalate the complaint to the Financial Markets Ombudsman Service (FMOS), which offers independent dispute resolution for financial consumers.

For complaints that fall outside FMOS’ scope, consumers may also contact Bank Negara Malaysia through BNMLINK.

Regulators have also recently moved to strengthen consumer protections surrounding claims handling and dispute resolution.

Bank Negara has recently revised its policies for stronger consumer protection and fair conduct reforms, with the institution saying that part of the revision is to aim for a clearer, quicker and fairer claims settlement process.

“The Claims Settlement Prac-tices Policy Document is enhan-ced to make general insurance or takaful claims clearer to understand, faster to complete and fairer to consumers.

“It also calls for the industry to adopt digital solutions to produce transformative customer experience,” says Bank Negara.

Aside from the solutions mentioned above, O’Dell says policyholders can also choose to take legal action.

At the same time, agents say consumers themselves must also take a more active role in understanding their policies before problems arise.

“Agents can keep educating, but consumers have to show up for that conversation too,” says Tan.

She adds that many people avoid engaging with their agents after purchasing insurance because they do not want to feel pressured into buying additional products, but that lack of engagement can lead to misunderstandings later on.

“The less you engage, the less you understand. And most people only realise that when something goes wrong,” she says.