Early comprehensive exposure to financial literacy key to nurturing money savvy youths

MANAGING money is a rite of passage that everyone goes through as they advance into adulthood.

For many grown-ups, however, money management can be a challenge due to a lack of exposure to personal finance during their formative years.

That is why education institutions should step up efforts to instil better financial literacy among the young, experts assert.

The fundamentals of savings and investments should be introduced to youths at schools and universities as a subject of its own, they recommend.

Financial literacy, experts said, must be introduced early on when children are developing so that they grow up to become prudent adults.

Financial education should be taught to everyone and not just to those who major in finance, accountancy or business, said Universiti Malaya Faculty of Business and Economics Assoc Prof Dr Aida Idris.

“The tricky part of teaching financial literacy lies in how we approach the subject because some students come with zero financial knowledge to begin with,” she told StarEdu.

Stressing that teachers and faculty members need to be experts in the subject, Aida said a formal education in financial literacy needs to be all-inclusive and comprehensible so that students may acquire the knowledge easily.

According to the Credit Counselling and Debt Management Agency (AKPK), an agency set up by Bank Negara Malaysia in 2006 to help individuals take control of their financial situation and gain peace of mind that comes from the wise use of credit, there are already some elements of financial literacy in the current education syllabus.Beginning 2019, Form Three students were required to take the Consumer Mathematics (Matematik Pengguna) subject that exposes them to making correct decisions with their finances.

And at the tertiary level, financial literacy is introduced in some higher learning institutions as an elective subject using the AKPK’s “Celik Wang” book as learning material.Universiti Tunku Abdul Rahman (UTAR) finance department head Dr Lim Boon Keong said the subject of financial literacy should cover topics such as money management, credit management, investment, insurance, tax planning, retirement planning and estate planning.

“Students should learn how to preserve, accumulate and distribute their wealth. By managing various aspects of financial literacy, youths will be able to manage their money better,” he explained.

Education institutions, Lim pointed out, should also take the initiative to organise financial planning workshops on a regular basis to train students.

“Inviting industry experts to give talks and organising competitions can help boost financial literacy among students,” he said.

Youths, Lim added, must be equipped with basic knowledge of personal finance from the get-go.

“Learning financial literacy at an early age helps youths shape the right attitude in managing money. And this will stick with them throughout their lives. As such, managing money is also about managing the future,” he said.

Starting young

The point of an early formal education in financial literacy is even more pertinent in light of the country’s high bankruptcy rate, especially among youths.

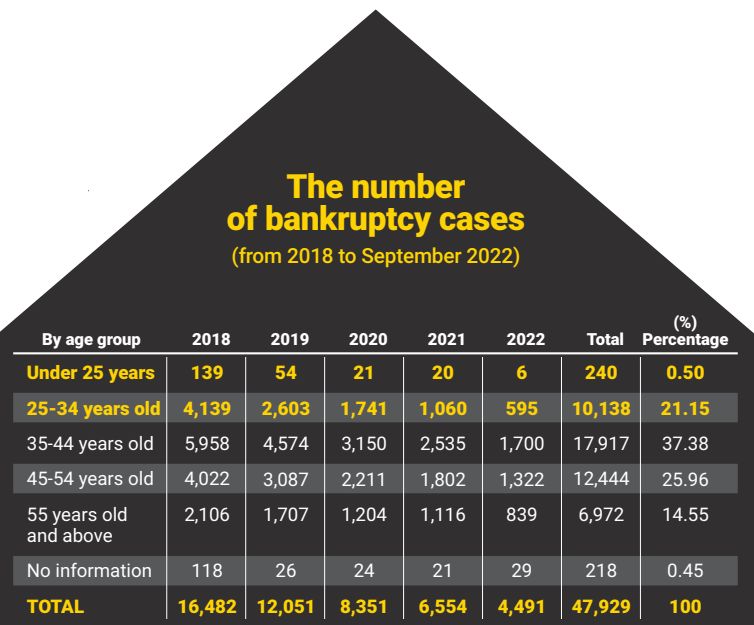

Based on the latest data available on the Insolvency Department website, an average of 17 bankruptcy petitions have been filed nationwide this year with 16 bankrupts declared daily.

A total of 4,491 individuals were declared bankrupt between January and September this year, bringing the total number of bankrupts in Malaysia to a whopping 271,554.

Of those declared bankrupt between 2018 and September this year, 10,138 were aged between 25 and 34; while 240 individuals were those under 25 (see infographic).

Citing the National Youth Survey 2021 by the Merdeka Center, the AKPK said 28.8% of those polled listed financial constraints as their main concern.

Here’s where boosting financial literacy could nip the problem in the bud, the department said.

“Financial education can make a difference. It can empower and capacitate people with the knowledge, skills and confidence to take charge of their lives and build a more secure future for themselves and their families,” the AKPK said in an email response.

Agreeing, Aida said youths who are more financially literate would be aware of the negative traits which may lead them down the slippery slope of financial constraints.

“Financial literacy is important because it teaches youths that there are certain behaviours that lead to bankruptcy. If they have that knowledge, then it will be easy to identify what sort of behaviour will land them in trouble with their money,” she said.

Sunway College assistant director (Pre-U Studies) Lee Thye Cheong said to counter bankruptcy, financial literacy needs to be viewed from a wider lens.

“Contrary to popular belief, the lack of income does not cause bankruptcy. The bankruptcy trap is primarily the result of poor borrowing and spending habits.

“Education today focuses on helping youths build successful careers and generate income. However, without a structured form of education on borrowing and spending prudently, youths may not have the right mindset, knowledge and skills to avoid the risk of bankruptcy,” he explained.

That is why elements of practicality needs to be imbued into the teaching of financial literacy.

“To be effective, it is important for the teaching of financial literacy to not take an academic approach. Instead, the approach should be one that’s practical which employs practical exercises, gamification and immersive experiences for the students,” he said.

Be mindful of socmed

These days, some industrious youths have also turned to social media to get insights and perspectives on personal finance. Accounts dedicated to savings and investments are a dime a dozen on platforms such as YouTube and Instagram.

The content, however, should be taken with a pinch of salt.

Picking up financial literacy tips on such sites, Lee warned, may lead to an oversimplification of personal finance.

Most social media platforms house content that is either in the form of attractive and short sound bites or video clips. The content does not delve into the details so the danger is that youths may think that they are already being shown the whole picture, he said.

Lee cautioned that following financial advice on social media may lead youths to make the wrong decisions when it comes to their money.

“Youths need to be more discerning when it comes to where they get their information from, and whom to listen to as there are many self-proclaimed financial literacy gurus on social media trying to earn a quick buck by producing content which may do more harm than good,” he said.Meanwhile, Lim stressed that information from social media should be accompanied by proper practice and coaching.

“Social media is a good start for young people to learn financial planning. But most of these videos are short and simple, may not be complete or are insufficient to impart the necessary knowledge and skills,” he said.

He warned that some content creators may have their personal agendas or ulterior motives to make the videos, such as to scam the public.

“Also, some videos may aim to advertise their own investment portals or financial products. It can sometimes be difficult to identify whether the content is reliable,” he said.

According to Lim, it’s best to always check the “Investor Alert List” on the Securities Commission (SC) website to ensure the reliability of a company.

What’s for certain, though, is that financial literacy will encourage youths to learn to live within their means and make sound judgments about money.

“With financial knowledge and skills, youths will be able to manage their income and spending properly. They need to learn how to spend within the budget, not overborrow money from the banks and overswipe their credit cards.

“Early financial literacy education which teaches youths to have a good relationship with money can help prevent them from going bankrupt,” Lim concluded.

Nurfatihah, 21, a student in Kuala Lumpur, is a participant of the BRATs Young Journalist Programme run by The Star’s Newspaper-in-Education (Star-NiE) team. Applications for the BRATs 2023 programme are now open. For more information, go to facebook.com/niebrats.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.