AS part of ongoing efforts to promote continued access to financing for small and medium enterprises (SMEs), Bank Negara conducted a survey in 2018 to obtain a better understanding of the financing needs and behaviour of SMEs.

According to Bank Negara’s annual report 2018, a total of 1,529 formal SME businesses participated in the survey, which covered firm and entrepreneur characteristics, business performance and challenges, as well as access to finance and usage of financial services.

“The survey showed that more than 90% of the SMEs served the domestic market, with 7% exporting their products and services. About 83% of SMEs reported utilising information and communications technology (ICT) in their business operations, with 22% that have their own website and 14% that operate online stores.

“More than half of the respondents (53%) used professional services including auditors, accountants or financial advisors to manage their financial accounts,” says the central bank.

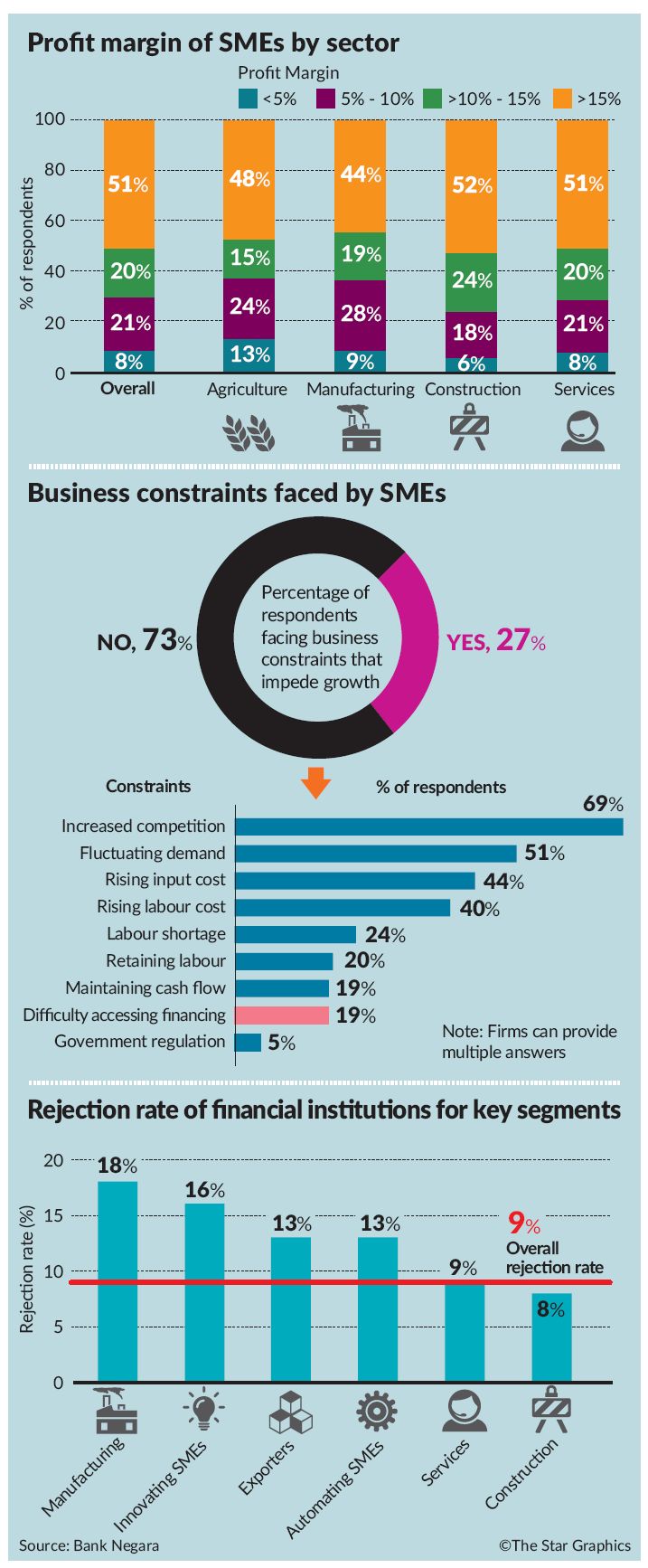

Despite the challenging business environment in the first quarter of 2018, the majority of SMEs (71%) recorded profit margins of above 10% and were able to maintain positive cash flows, says Bank Negara.

“Manufacturing firms reported higher levels of productivity and paid higher wages for new graduate hires compared to other sectors.”

On financing, the central bank says respondents reported utilising funds from a variety of sources, both internal and external, with own cash contributions being the main source.

“Among other funding sources, about 27% of the respondents had facilities with financial institutions, followed by family and friends, internally-generated funds and micro-finance institutions.

“In the micro-enterprise segment, 22% had financing facilities with financial institutions, including 9% of respondents who secured financing under the Pembiayaan Mikro facility.”

Bank Negara says sources of financing also vary through the business life cycle.

“At the initial stage, young firms tend to rely on their own cash and informal sources such as family and friends. This is consistent with most research findings, which attribute such behaviour typical of young firms to information opacity; lack of collateral, track record and financial skills; as well as high transactional costs.

“As businesses mature (typically after five years in operation), they tend to rely more on external financing in the form of both debt and equity, including bank financing.”

Among the SMEs that had applied for financing, most indicated that they were able to secure financing, says the central bank.

“About 22% of the respondents had applied for financing in the six months prior to the survey, with the majority (94%) of their applications being approved.”

About 13% applied to financial institutions with 91% of their total financing applications approved, while the remaining 9% applied to other sources, with a 99% approval rate.

Women-owned firms reported higher demand for financing (33% of women-owned firms applied versus 22% for all respondents), but experienced a lower approval rate of 83% (overall: 94%) mainly due to the lack of track record and insufficient documentation.

“Most of these firms obtained unsecured financing from micro-finance institutions, banking institutions and development financial institutions,” Bank Negara says, adding that about 44% of the respondents were first-time borrowers.

“The main purposes of the financing applications were for the purchase of assets (building, property, machinery and equipment: 23%), working capital (22%) and starting a new business (19%).”

On average, the majority of the applications (89%) was approved within one month and the funds were disbursed within the subsequent month, says the central bank.

The survey also provided insights on SMEs’ usage of other financial services, such as insurance, takaful and e-payments.

“More than half of the respondents have insurance or takaful products, although this was less prevalent among micro-enterprises.

“While the current take-up has been low, potential future demand for insurance and takaful by SMEs is significant for all products across the board, with emerging interest particularly in securing protection for risks associated with cyber security, professional indemnity, payment default and damages in crops.”

The survey noted that SMEs mainly made electronic payments, but preferred cash in receiving payments from customers.

“It was also observed that cheques remained popular for payments to suppliers and other business to business transactions.”

Underlying challenges in financing

With regards to challenges, the survey reveals that financing barriers mainly relate to documentation, costs and business viability.

“Among the key constraints to business growth, difficulty in accessing sufficient financing was ranked low, second to last out of the nine constraints identified by SMEs,” says the central bank.

It says SMEs that experienced rejections of their financing applications cited insufficient documentation, insufficient cash flow to meet repayments and non-viable business plans as the main reasons for rejection.

“SMEs involved in automation, innovation, manufactures of goods, and exports experienced higher rejection rates compared to the overall SMEs. Firms that automated stated insufficient collateral and projects perceived to be of higher risk as key reasons for rejection.

“The rejected applications were mainly for the purchase of machinery and equipment and ICT tools, as well as undertaking research and development.”

Bank Negara says these projects could be deemed to be higher risk as they may involve moveable and intangible assets with low salvage value in the event of commercial failure and involve the use of new and untested processes with high uncertainty on returns.

“Innovative firms cited insufficient documentation as a key factor for rejection. Exporting and manufacturing firms that faced greater difficulty obtaining financing were mainly firms that were newly established with limited repayment track records.

“Businesses that needed financing but did not apply (41%) were either cautious in taking on debt, unsure of their repayment capacity, or found the application process too difficult.”

The survey revealed that about 46% of the respondents stated that the financing products offered by financial institutions did not meet their business needs due to high financing costs (50%), insufficient financing amount (42%) and onerous documentation requirements (29%).

“The average financing rate that respondents were willing to pay was 3.88%, well below the average lending rates to SMEs of 6.18% at the time of the survey (second quarter 2018).”

The survey also indicated that the main constraints to SME growth were factors associated with operating and business conditions, namely increasing competition (69% of respondents), fluctuating demand (51%), rising input costs (44%) and rising labour costs (40%).

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.