LAST Monday was the cut-off date for the FTSE Bursa Malaysia KLCI (FBM KLCI) index review and based on the ranking of the top 30 market capitalisation, it was indeed momentous as both Genting Bhd (Genting) and Genting Malaysia Bhd (GenM) will likely be booted out when the official announcement is made next week.

(Genting) and Genting Malaysia Bhd (GenM) will likely be booted out when the official announcement is made next week.

The rebalancing date itself will be implemented after close of business on the third Friday of December, which is Dec 20, while the effective date is on Monday, Dec 23.

In place of the two names that have been an index constituent from Day 1 of the formation of the index itself will be Gamuda Bhd and the new kid on the block, 99 Speed Mart Retail Holdings Bhd.

An investor’s favourite

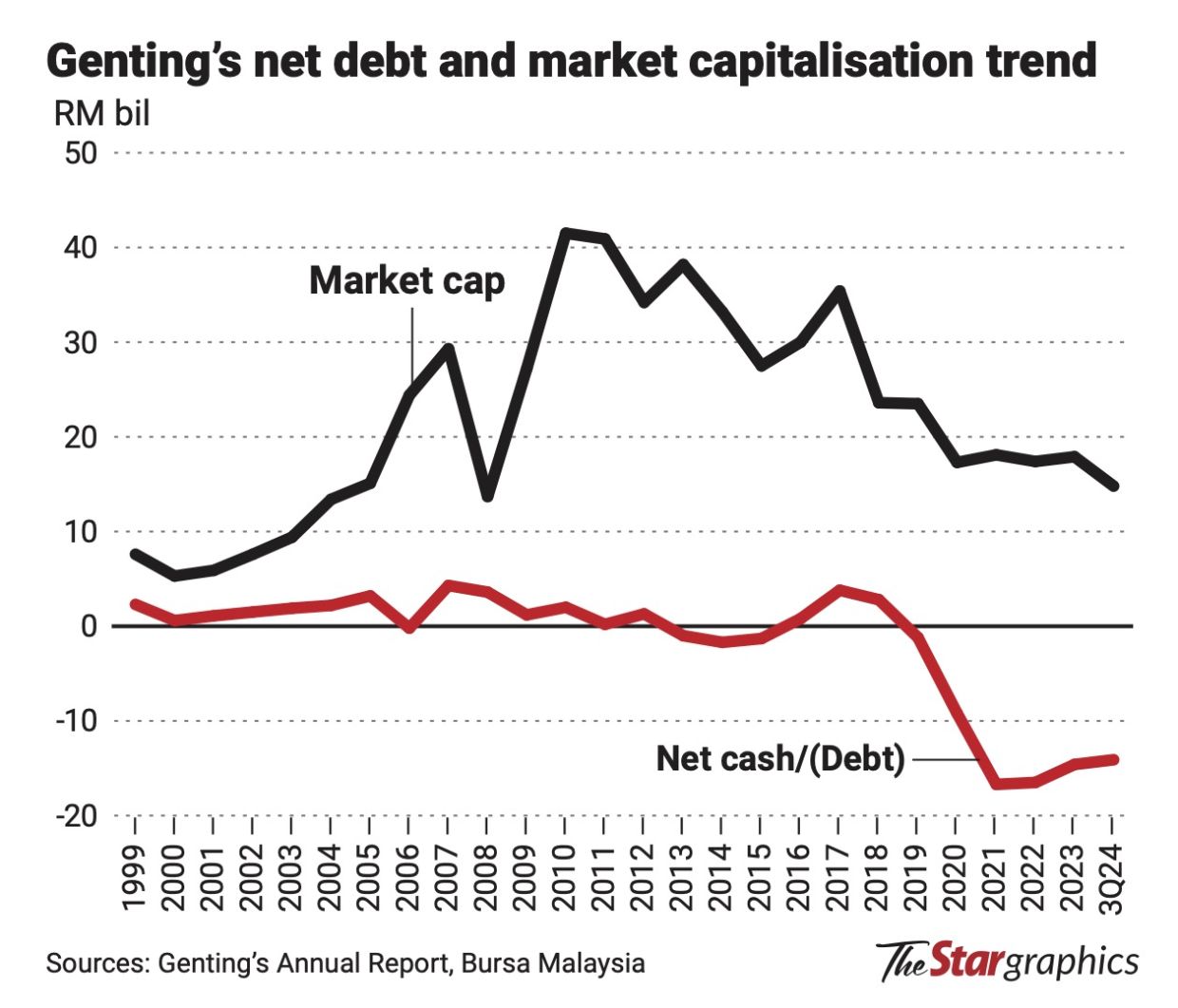

Genting and GenM were once the high-flying stocks of Bursa Malaysia. In early 2011, Genting’s share price hit a record high of almost RM12, translating to a market capitalisation of more than RM45bil, making it one of the top-ranked index-linked stocks and one company that no fund could ignore.

Genting and GenM had been the darlings of the stock market for the longest time, especially among foreign portfolio managers, as they were always seen as proxies to the economy due to the diversified nature of its business model as well as the exposure to the lucrative casino operations, before regional competitors emerged.

Genting was not only involved in the leisure and hospitality business, but also very much in some key segments of the economy, including the power, plantation, oil and gas, and property sectors; as well as expanding overseas, which included Resorts World Sentosa. Genting was also into the cruise business with the acquisition of Star Cruises as an associate company.

It transformed its business operations or tried to re-invent itself to remain ahead of the competition by going big in theme park development as well as casino businesses in various jurisdictions, especially in the United Kingdom and the United States. At the same time, it was also actively bidding for casino licences in Japan, New York, Thailand and the United Arab Emirates.

Victim of Covid-19

Before Covid-19, Genting’s share price held up relatively well despite the challenging business environment, especially in the leisure and hospitality sector with the emergence of new casinos in the region and a highly competitive market. At end-2019, Genting’s share price had fallen to hover just above RM6 although its market capitalisation remained relatively healthy at almost RM24bil.

That year, Genting’s revenue was just over RM21bil, adjusted Ebitda hit almost RM8bil and net earnings were about RM2bil, translating to an earnings per share (EPS) of 51.8 sen. At that time, shareholders’ funds totalled RM35bil although the company was marginally in net debt of about RM1.2bil.

Covid-19 impacted the business greatly as the company reported losses for three consecutive years totalling some RM2.7bil, but returned to profitability in 2023 with net earnings of RM929mil.

For the first nine months of this year, Genting reported a revenue of RM20.84bil with profit attributable to shareholders at RM1.05bil, translating to an EPS of 27.3 sen. Annualising the figures suggests that Genting may report a strong performance this year with net earnings of more than RM1.4bil and EPS of about 36.5 sen.

However, the balance sheet has shown strain as net debt has risen to more than RM15bil (see chart). The weakness of its share price is also somehow correlated to the deteriorating net cash/debt position, especially post-Covid-19.

RPTs and lawsuit

Genting or GenM have in the past been involved in related party transactions (RPTs) and some were detrimental to shareholders as the newly acquired companies from related parties were not able to turn around as expected. One key example was Empire Resorts (Empire). GenM first purchased 13.2mil shares held by Kien Huat Realty III Ltd, representing 35% voting power of Empire for US$128.6mil or RM538.8mil in 2019.

GenM defended the purchase despite the market not liking it due to the amount of investment that escaped the company from calling for a general meeting to approve the deal. Over the years, GenM has now invested close to US$725mil into Empire and is yet to see the investment yielding results.

In 2010, GenM was also involved in another RPT — the purchase of UK casino operations from Genting Singapore for £340mil. Although this was approved by the shareholders, the acquisition was met with much scepticism as reflected in the drop in the company’s share price post-announcement.

Recently, GenM was involved in a legal battle involving Genting Americas Inc.

The company is being sued by RAV Bahamas Ltd concerning the operations of Resorts World Bimini in the Bahamas, demanding damages exceeding US$600mil. GenM has vowed to defend itself and has filed a motion to dismiss the demand on multiple grounds.

Genting was also involved in 1Malaysia Development Bhd-related issues, including the sale of its power assets to the troubled state-owned company for RM2.3bil in 2012 and the purchase of superyacht Equanimity (now renamed as Tranquility) for US$126mil in 2019.

Still a conglomerate

Despite the setbacks, Genting and GenM remain institutional favourite stocks, especially among non-syariah-compliant fund managers and foreign shareholders. However, the potential falling out of the FBM KLCI will trigger an exodus and rebalancing by these funds, especially the passive ones.

All is not lost for Genting and GenM as they can always get back into the index once their market capitalisations recover to the acceptable level via auto addition or replacing constituents that may fall out.

All Genting and GenM have to do is to enhance their governance framework and not get involved with RPTs. They must also improve their net debt position gradually to convince the market that its financials have been managed more efficiently.

After all, Genting has generated net profits attributable to shareholders in excess of RM30bil between 1999 and the latest quarterly period, translating to an annual profit on average of more than RM1.15bil per annum.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.