ALTHOUGH not out of the woods yet, the recent statistics released by the National Property Information Centre (Napic) exhibit a positive trend for the industry as far as the overhang is concerned.

Not only that, even future supply looks much more manageable than before as residential, serviced apartments and small-office home-office (SoHo) properties under construction fell year-on-year (y-o-y).

Based on the recently concluded quarterly results, the property sector reported a much better performance as far as sales are concerned while a select few also surprised the market with improved bottom lines.

Not surprisingly, the strong showing was a reflection of an upbeat property market as both volume and value of transactions surged to an all-time high of over 399,000 units, worth a staggering RM196.8bil, transacted in 2023.

The pick-up in activities was evident in states like Johor, where transactions jumped by more than 44% y-o-y, accounting for 16.2% of volume and 18% of the value nationwide.

Nevertheless, Selangor remains Malaysia’s favourite property hot spot, accounting for 22% and 30% of the nation’s total transaction volume and value, respectively.

In addition, according to the Napic report, some 21.5% of market transactions were purchases made directly from developers while the balance was sub-sale volume.

Reduced overhang

The biggest positive from Napic’s annual data was the significant reduction in overhang properties.

For this column, where residential properties include serviced apartments and SoHo units, the total overhang volume fell by 9.8% y-o-y to 46,641 units while in terms of value, there was an 11.1% decline to RM34.3bil.

This is the lowest overhang volume since the 47,806 units that were observed at the end of 2019, and in terms of value, it is just RM4.5bil above the level seen in the same year.

Serviced apartment overhang fell sharply with the number of units and value dropping by 13.1% and 17.7% y-o-y to 20,825 units and RM23.8bil, respectively.

Geographically, serviced apartment overhang saw a significant reduction in Johor as there was a 17.1% and 20.6% drop in volume and value to 14,132 units and RM9.7bil, respectively.

Selangor and Kuala Lumpur too saw steep declines, with both witnessing 29.4% and 20.1% fall in the number of units and 33.9% and 16.5% decline in terms of value, respectively.

Another interesting statistics are the numbers related to the “Unsold under Construction” data. As of the end of 2023, the total number dropped to 79,988 units, which is a significant development, considering just two years ago the number was as high as 120,486 units.

So this is indeed a big positive for the market as a whole.

Market impact – higher prices

For the longest time, the overhang situation has cast a dark shadow on the Malaysian property market, as it felt like we were overbuilding, and market watchers were raising concerns as to what would happen to the market when more residential and high-rise apartments and serviced residences were completed in the future.

In the residential segment, as seen in Chart 1, the total overhang has dropped 30% from the peak of 36,863 units two years ago while in terms of value, some RM5.1bil worth of overhang has been removed.

In the serviced apartment segment, overhang units have been reduced by 14.1% or 3,470 units while in terms of value, some RM4.1bil was cleared.

As the market seems to be “tighter” with less overhang, developers too have seen a good pick-up in sales last year and at the same time, the increase in transaction volume has caused prices to increase across the board.

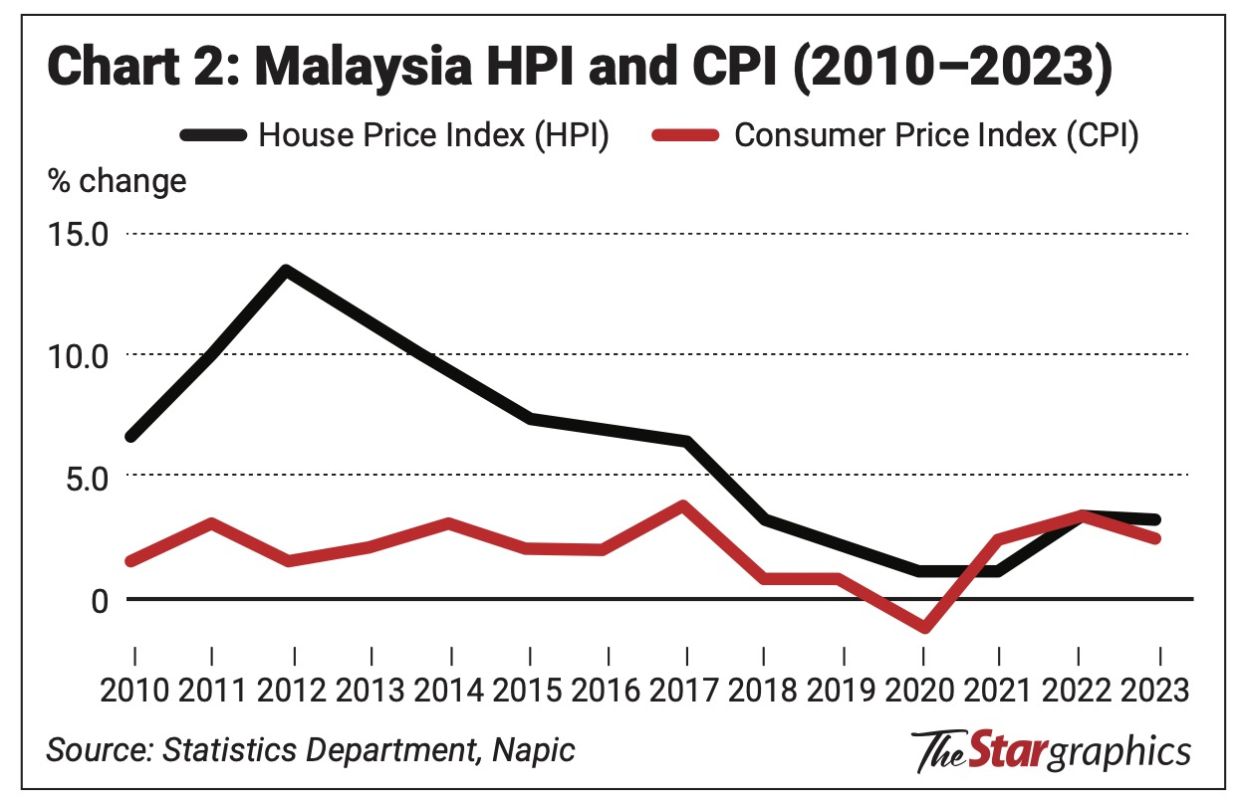

Overall, the Malaysian house price index (HPI) rose by 3.2% y-o-y, slightly ahead of the increase in the Malaysian consumer price index, which rose by 2.5% in 2023, as can be seen in Chart 2.

In the fourth quarter of 2023 period alone, HPI rose by 3.9% quarter-on-quarter (q-o-q) and 3.7% y-o-y.

Inflection point

As prices rise and supply tightens due to lower overhangs, it will be interesting to see how the year 2024 will pan out.

As it is, based on forward-looking statements from most large developers, the guidance given for this year is for marginally higher sales from new launches and hence the market is expected to remain healthy with relatively good pick-up.

While Malaysia may not see an inflection point to the extent property prices become unaffordable for the general public, as we have seen in other more developed cities like Singapore, Hong Kong or Sydney, there is a likelihood that in certain locations and certain sub-segments of the market we may see demand far outpacing supply as the tight market will push prices higher.

This includes the renewed interest in the Johor property market where new launches and secondary market transactions, capitalising on the soon-to-be-completed Rapid Transit System line connecting Johor Bahru to Singapore, are rising.

Penang property market too seems to be getting a new lease of life with strong sales seen by Eastern & Oriental Bhd ’s Andaman Island, as foreign buyers are lured by relatively cheap ringgit, while prices in the Klang Valley have generally held up relatively well although rental yields have been under pressure.

’s Andaman Island, as foreign buyers are lured by relatively cheap ringgit, while prices in the Klang Valley have generally held up relatively well although rental yields have been under pressure.

In conclusion, after several years of unabated increase in the overhang, especially within the high-rise and serviced apartment segments and, in particular, for the Johor property market, the industry is now much healthier and is poised to see sustainable growth, going forward.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.