ONE of the first reactions to the “unilateral” and unsolicited bid by Sunway Bhd for IJM Corp Bhd was whether it constituted a hostile takeover.

for IJM Corp Bhd was whether it constituted a hostile takeover.

Initially anticipating a merger announcement, comments were heard from the floor of the press conference room pointing out that only Sunway was announcing the planned voluntary takeover of IJM, without the latter present.

While hostile bids are part and parcel of capital market activity, they rarely occur in the Malaysian market.

And it would indeed be very interesting if Sunway, a successful conglomerate led by its iconic founder and leader Tan Sri Jeffrey Cheah, were to actually embark on such an audacious move.

Sunway, the potential acquirer, appears to be capitalising on the stronger premium its shares currently command on Bursa Malaysia to propose and mainly fund this deal.

Its market capitalisation now stands at about RM38.45bil, factoring in the upcoming mega listing of its 84%-owned healthcare arm, Sunway Healthcare, by the end of this quarter.

In comparison, IJM’s market capitalisation stands at around RM10.2bil.

With the majority – about 90% – of the purchase price to be satisfied through the issuance of new Sunway shares, some are questioning whether this is a good deal for IJM’s shareholders.

This concern is further amplified by the fact that IJM’s shareholders would not be entitled to the dividend-in-specie to be distributed to Sunway’s shareholders when Sunway Healthcare is listed.

Sunway intends to distribute 676.04 million Sunway Healthcare shares to existing shareholders, based on one Sunway Healthcare share for every 10 Sunway shares held, with the entitlement date to be determined later.

For Sunway’s shareholders, the offer’s reliance on new Sunway shares raises dilution concerns, given the enlarged equity base and the absence of guaranteed earnings accretion.

Assuming 100% acceptance of the offer, IJM’s shareholders would make up about 20% of the enlarged share base, Sunway chief financial officer Clement Chen said at the announcement on Monday.

The price reaction seen in IJM’s shares a day after the proposed deal was announced indicates some doubt as to whether the offer will be accepted.

Privatisation offers usually result in the acquiree’s shares trading near the offer price, which in this case is RM3.15 per share. However, IJM’s shares closed one sen lower at RM2.74 a day after the proposed offer was made.

IJM’s shares traded at RM2.82 at the time of writing.

Hostile or not?

Meanwhile, checks with bankers on the ground reveal that despite the bid being declared unsolicited, there may have been certain parties involved in putting the deal together, indicating that the attempted buyout may not be hostile after all.

“One clear indication of this is the fact that the offer isn’t aggressive enough to have the traits of a hostile takeover.

“Going by some views, the offer undervalues the target (IJM).

“Combine that with a low cash value, the deal sounds like an opportunistic one for Sunway, which may have been cajoled into making the offer,” notes a seasoned investment banker.

With a high proportion of new shares being used to fund the deal, a key concern is the limited cash element in the offer.

With only 10% of the offer price payable in cash, will shareholders find this offer uninteresting?

IJM’s shareholding structure is diverse, with the Employees Provident Fund (EPF) as its single largest shareholder, holding about an 18.4% stake based on the latest publicly available information, while the Retirement Fund Inc owns a 9.64% stake.

The company’s top 30 shareholders are mainly institutional asset managers, collectively holding about 60% of the shares.

Take the case of Permodalan Nasional Bhd (PNB), which owns 14.54% of IJM through its various funds.

Sunway has said it intends to reach a 90% shareholding in IJM through acceptances, after which it intends to compulsorily acquire the remaining shares and delist the company.

PNB alone can put a stop to that with its shareholding in IJM.

Note also that PNB does look like it is in the mood for cash.

In late October 2025, it was reported that PNB and EPF had appointed BNP Paribas to advise on a potential sale of the commercial assets of the Battersea Power Station project in London, following expressions of interest from external investors.

However, PNB and EPF later issued a joint statement clarifying that they have no immediate plans to sell the assets and remain committed to the project as a key strategic investment.

They stated that engaging advisers to evaluate unsolicited proposals is a normal part of business practice, especially when investments reach a certain level of maturity and targeted returns, and does not necessarily indicate a need for cash.

Still, one might ask why a bank would be appointed to advise on a sale if liquidity were not a concern.

If indeed some major IJM shareholders were to hold out for a higher cash portion, that could be an issue for Sunway.

As it stands, the cash portion of RM0.315 per share would amount to some RM1.1bil, to be funded partly through debt.

Sunway’s net gearing ratio stood at 0.36 times as at Sept 30, 2025, before factoring in this proposed transaction.

Analysts note that it may not be ideal to raise significantly more cash via debt to fund the offer, especially if it is just to get every IJM shareholder on board eventually.

That being said, most analysts are recommending that IJM shareholders accept Sunway’s RM3.15-per-share takeover offer, viewing it as fair and offering strategic benefits such as exposure to a larger, more diversified group.

While the offer is below some target prices (TPs) of around RM3.40, firms including TA Research, Hong Leong Investment Bank Research and MBSB Research highlight its alignment with historical valuation multiples, certainty of value and potential synergies.

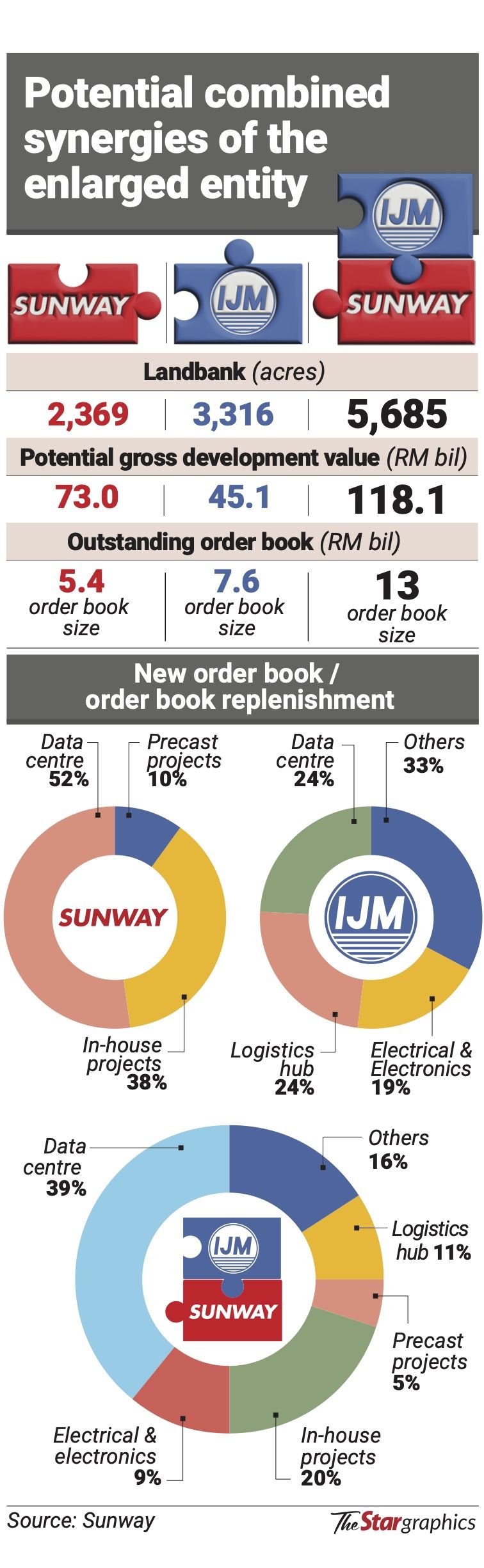

Notably, the deal would merge two of the country’s leading construction and property players into a single powerhouse with a combined valuation of about RM47.7bil.

However, Kenanga Research’s dissenting view stands out.

The research house says the RM3.15 offer price is unattractive for IJM shareholders as it falls below its fair value estimate of RM3.40.

“In addition, the implied valuation is unfavourable, with Sunway’s issue price of RM5.65 translating into a lofty 2026 calendar year (CY26) price-to-earnings ratio (PER) forecast of 27.6 times, compared with 19.4 times CY26 PER implied by the RM3.15 offer for IJM,” it says.

“Based on our Sunway’s TP of RM4.73, the implied value of the offer for IJM is only RM2.69, which is below both the current share price of RM2.75 and our TP of RM3.40,” Kenanga Research adds.

The research house adds that while it is unfavourably inclined towards the offer price, it acknowledges that the enlarged entity could enhance operational efficiencies, potentially improving IJM’s construction margins, alongside possible synergies across the property and industrial manufacturing segments.

Other positives for IJM include its position to secure a portion of contracts for the Penang light rail transit (LRT) Mutiara Line project, given its involvement in previous LRT developments.

Its strong earnings visibility is underpinned by an outstanding construction order book of RM9.3bil and a favourable property sales outlook.

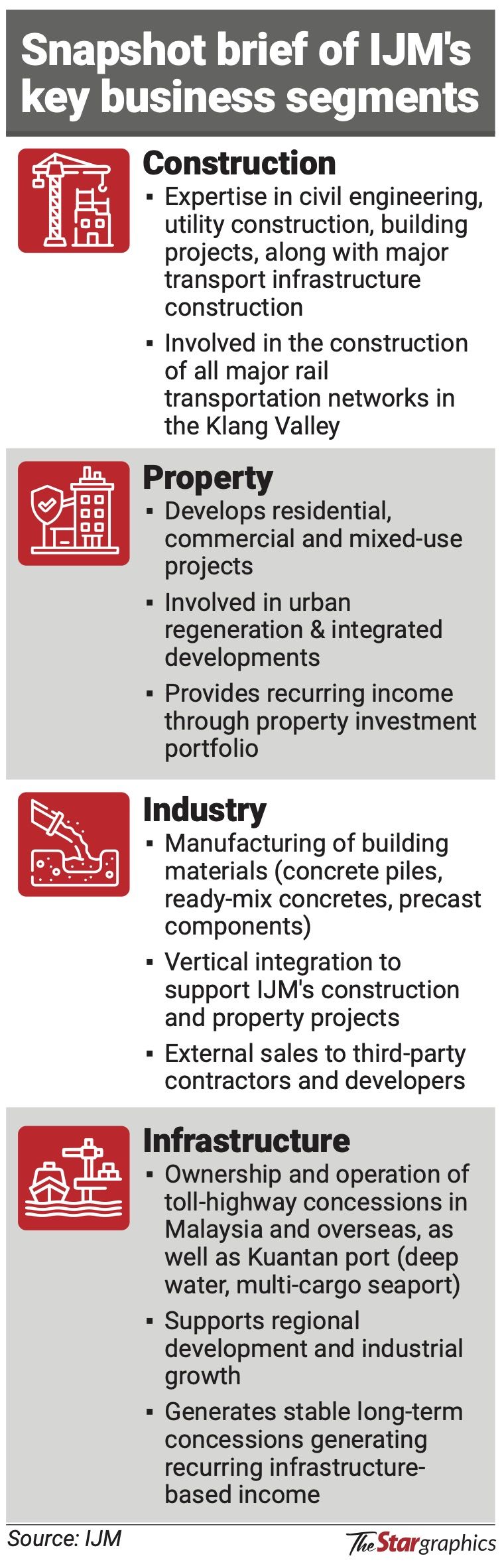

IJM also owns Kuantan Port, the largest port on the East Coast, with other potential re-rating catalysts including a possible divestment of its tolled road assets to lighten its balance sheet and recycle capital, adds Kenanga Research, which has an “outperform” call on the stock.

The research house notes that while it is unfavourably inclined towards the offer price, it acknowledges that the enlarged entity could enhance operational efficiencies, potentially improving IJM’s construction margins, alongside possible synergies across the property and industrial manufacturing segments.

Meanwhile, MBSB Research senior analyst Royce Tan says the privatisation offer price is “not that generous” but believes it “fair”.

“The offer price of RM3.15 is still a premium compared to today’s close, which values IJM at a forward PER of 21.1 times, based on our financial year 2027 (FY27) estimates, which is also in line with its five-year mean PER of 21.4 times.

“As of its third quarter of FY26, IJM’s net tangible assets per share stood at RM3.17,” Tan tells StarBiz 7.

He adds that while the offer represents a slight 4.3% discount to its sum-of-the-parts-derived fair value of RM3.29, it remains reasonable based on those valuation comparisons.

“While it would seem that IJM’s shareholders may potentially be losing out (from Sunway Healthcare’s dividend-in-specie), the deal provides an immediate premium and a continued exposure to the construction and property upcyle via Sunway, so this seems to be fair on a risk-adjusted basis,” he notes.

The absence of any entitlement for IJM shareholders to Sunway’s planned dividend distribution of shares in its healthcare division is a stark feature of the proposed buyout.

Sunway Healthcare’s enterprise value (EV) is estimated at RM8.455bil, based on earnings before interest, taxes, depreciation and amortisation (Ebitda) of RM469.72mil for FY24, according to information disclosed in its prospectus exposure.

This valuation applies a conservative EV/Ebitda multiple of 18 times to the latest publicly available financial data, which is slightly more than a year old.

In contrast, some analysts estimate that Sunway Healthcare could be listed at between 20 and 23 times EV/Ebitda, based on valuation precedents from comparable private hospital transactions.

Based on the above, the implied equity value for FY24 is approximately RM8.15bil.

Given that Sunway’s retained stake in Sunway Healthcare post-initial public offering (IPO) will be 69.4%, this equates to RM5.67bil, or about 83.11 sen per Sunway share.

Furthermore, with Sunway’s shares trading at around RM5.63, this suggests that a meaningful portion of the anticipated Sunway Healthcare IPO value is already reflected in its share price.

Stripping out the healthcare component, Sunway’s remaining businesses are therefore valued at about RM4.80 per share, based on conservative valuation assumptions using FY24 numbers.

Sunway also indicated in its latest financial statements for the nine-month year-to-date period in FY25 that its healthcare segment, excluding startup losses from its two newly opened hospitals, recorded organic growth of 18.4%, driven by higher bed capacity and improved occupancy rates.

One of the two new hospitals – Sunway Medical Centre Damansara – achieved Ebitda breakeven significantly faster than usual, in just eight months, compared with an industry average of around two years.

The quicker breakeven of new hospitals, together with stronger bottom-line growth across Sunway’s other business segments in the latest quarter, suggests that the group’s current equity value may be higher than earlier implied.

If so, this would indicate that even greater healthcare-related premiums are already embedded in Sunway’s share price.

This, in turn, implies that much of the highly anticipated IPO upside may already be priced in, and that future share price gains would depend largely on execution and the ability to sustain growth.

Looking ahead, Sunway Healthcare also has plans to establish new healthcare facilities in Penang, Kelantan and Johor, according to information on its website.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.