SPEAK to most Malaysians on the street and one will find that many are scratching their heads almost to the point of exasperation as to why the ringgit’s weakness is so stubbornly persistent.

In fact, a topic of conversation that will unquestionably surface at watering holes, restaurants and gym locker rooms is how expensive tertiary education is getting following the Malaysian currency’s latest slide.

The other worries are over the price of cars with the weaker ringgit and some wonder how much more expensive will food be as Malaysia imports most of what we eat.

On the other hand, it can be said that those who have kept abreast of developments in the business, economics and political arenas of the country would be able to make out good educated guesses as to why the local note has been so shaken, and more importantly, what needs to be done.

The scourge of corruption is also blamed for the weakness of the local unit. The ringgit’s decline has been in the making since 2014, a decade ago, when the 1MDB scandal became mainstream news globally. The ringgit has been on a long-term decline since with many governments in those ensuing years having not tackled what some will say are the many root causes for the currency’s fall.

Having appreciated to RM4.60 at the end of 2023, many economists have predicted for the ringgit to maintain its momentum, at least until it touches the RM4.30 to RM4.50 range by the end of this year.

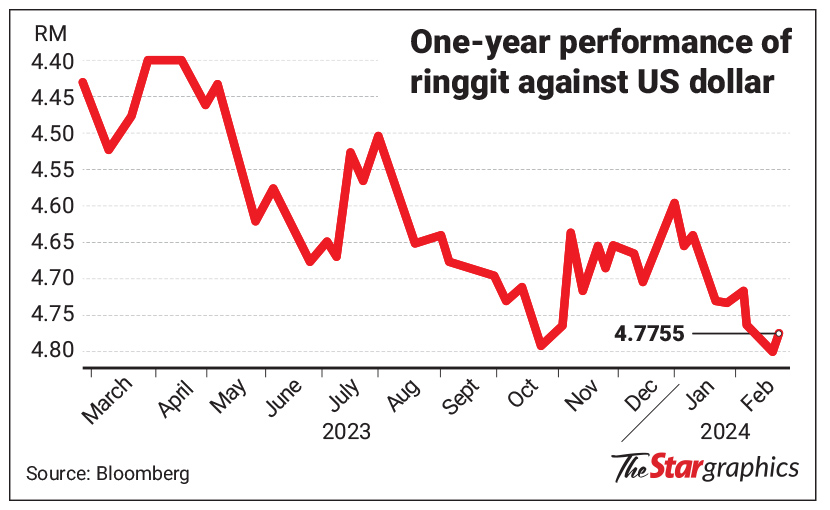

However, the latest beatdown began in the middle of January as the Malaysian currency slipped past the psychological barrier of RM4.70 again, with this past week alone seeing it dip to RM4.801 to the US dollar – its weakest standing against the greenback since January 1998 – while the Singapore dollar has also strengthened to approximately RM3.56.

Incidentally, the reasons given for the ringgit’s spiral was attributed to “external factors”, by which any Malaysian would most likely suspect to be the continued mixed messages permeated by the US Federal Reserve (Fed).

The Fed has indicated that it is on the right track in fighting inflation and is maintaining the US Treasury rates untouched but it is adamant the battle is not over.

Some are also stipulating that with China seemingly still dragging its feet in terms of its post-lockdown recovery, this situation has affected Malaysia since the former has been the latter’s largest trading partner since 2009, in addition to the ringgit being positively correlated to the yuan.

However, there are other countries that see China as its largest trading partner, like Singapore, which have not seen their currency slide as much as the ringgit.

But is merely pointing the finger at the outside world sufficient in helping Malaysia find solutions to halt the local currency’s weakness, or should our policymakers be more proactive in identifying domestic concerns and rectifying them, doing more of a part in driving up demand for the ringgit?

In fact, experts in the economic and financial spheres have been pointing to a number of well-documented reasons for the prolonged poor showing of the Malaysian note, and this topic itself has been discussed at length, both within the mainstream publications and on social media.

And the preponderance of reasons do point inwards with much of it skew to the policy responses by many government since 2014, which was the start of the decade-long decline in the value of the ringgit.

Perhaps what the average Malaysians on the street would like to know at this minute is what can actually be done to improve the ringgit’s standing, instead of merely looking at its problems. After all, one can say the value of a country’s currency corresponds to the potential of that nation.

Symptoms plaguing the ringgit

At the risk of appearing to flog a dead horse, a quick glance at what economists have been saying are pulling down the ringgit are both external and domestic, and some of these experts have been more forthright than others.

For example, as MIDF Research economics team writes in a note published on Thursday, the recent weakening of the Malaysian note year-to-date towards RM4.79 by mid-February (end-2023: RM4.59) was again influenced by fluctuating market sentiment.

“Recent stronger-than-expected data releases in the United States led to a review in the timing for rate cuts by the Fed from March 2024 to June as shown by the Fed funds futures as of Feb 15,” the research unit reports.

It says that the resilience shown by the US job market and its broader economy will cause the Fed to maintain the high-for-longer policy stance before embarking on a shift to rate cuts later this year amid expectations for inflation to continue moderating, translating to a downside risk to the ringgit’s outlook as the greenback will stay strong for an extended period.

The strength of the US stock market and the value the ‘Magnificent Seven” tech companies have attain are again reasons why money keeps being drawn into the United States with the capital markets being a high barometer for the dollar’s attractiveness.

In addition, the dollar’s long-held position as the world’s reserve currency – especially as the geopolitical conflicts continue flaring up almost on a weekly basis – is also significantly helping its strength, as has been observed by Center for Market Education’s (CME) chief executive and economist Dr Carmelo Ferlito.

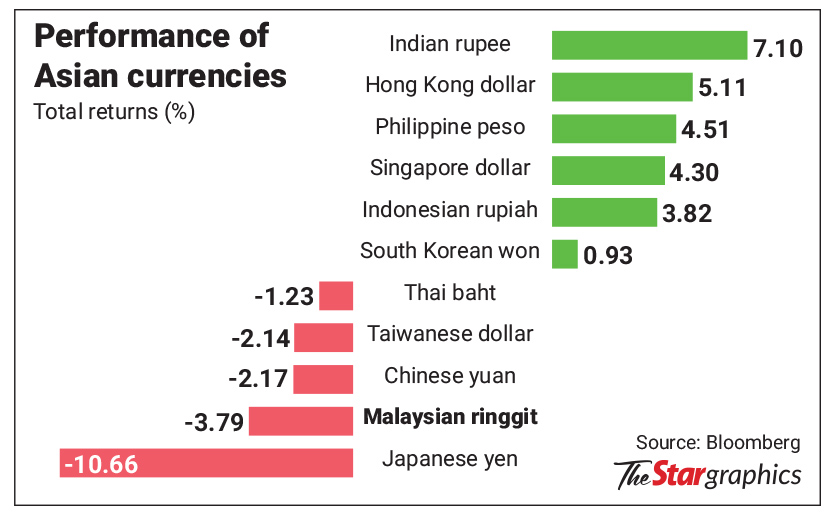

Another oft-mentioned external factor that has been weighing down the ringgit is Malaysia’s heavy links to China, whose post-lockdown recovery is still sluggish.United Overseas Bank (UOB) senior economist Julia Goh and senior foreign exchange (forex) strategist Peter Chia opine that as such, many Asian currencies are nursing year-to-date losses, as the Thai baht has also depreciated by 5.1% against the dollar, as compared with the ringgit’s slide of 4.1%.

Of particular interest is that while the international factors that have been contributing to the battering of the local note are well-established, economists are also delving into domestic elements that have given rise to this persistent weakness of the ringgit, in an attempt to discover if more can indeed be done.

Sunway University professor of economics Dr Yeah Kim Leng is straight to the point when he reveals that from a macro perspective, a better measure of exchange rates is the effective exchange rates based on a basket of inflation-adjusted, trade-weighted currencies of the country’s trading partners as tracked by the Bank for International Settlements.

“Based on this measure, Malaysia’s effective exchange rate index in 2023 showed a decline of 2.6% from the previous year, a 4.8% fall from the value in 2020 and a 18.7% drop from 2010,” he tells StarBizWeek.

Looking at the mirror

With this, Yeah says the ringgit’s decline can be considered a persistent trend that can only be reversed through effective structural reforms and sustained upgrading of the economy along with improved governance and political and economic stability.

CME’s Ferlito says domestically, there has been in the background a general climate of policy uncertainty, with Putrajaya having been focused on issues such as the bumiputra agenda, new price controls, and government intervention in the rice industry.

“Instead, needed reforms such as business-friendly regulations or the rationalisation of subsidies keep on being delayed.

“Furthermore, investors will be nervous about investing in a country where a government can intervene into its economy any time,” he adds.

Mirroring Yeah’s sentiments, he says with such an extended downtrend, there are doubts that the ringgit’s path could be easily reversed, expounding that strong actions in terms of policy consistency and the commitment to a clear pro-market agenda are necessary and the best that can be done.

He is of the view that the first item on the government’s to-do list would be adopt a more decisive approach towards the implementation of market reforms, including taking action on those that have been announced such as a more friendly Malaysia My Second Home policy, a more liberal skilled labour policy and the aforementioned rationalisation of subsidies.

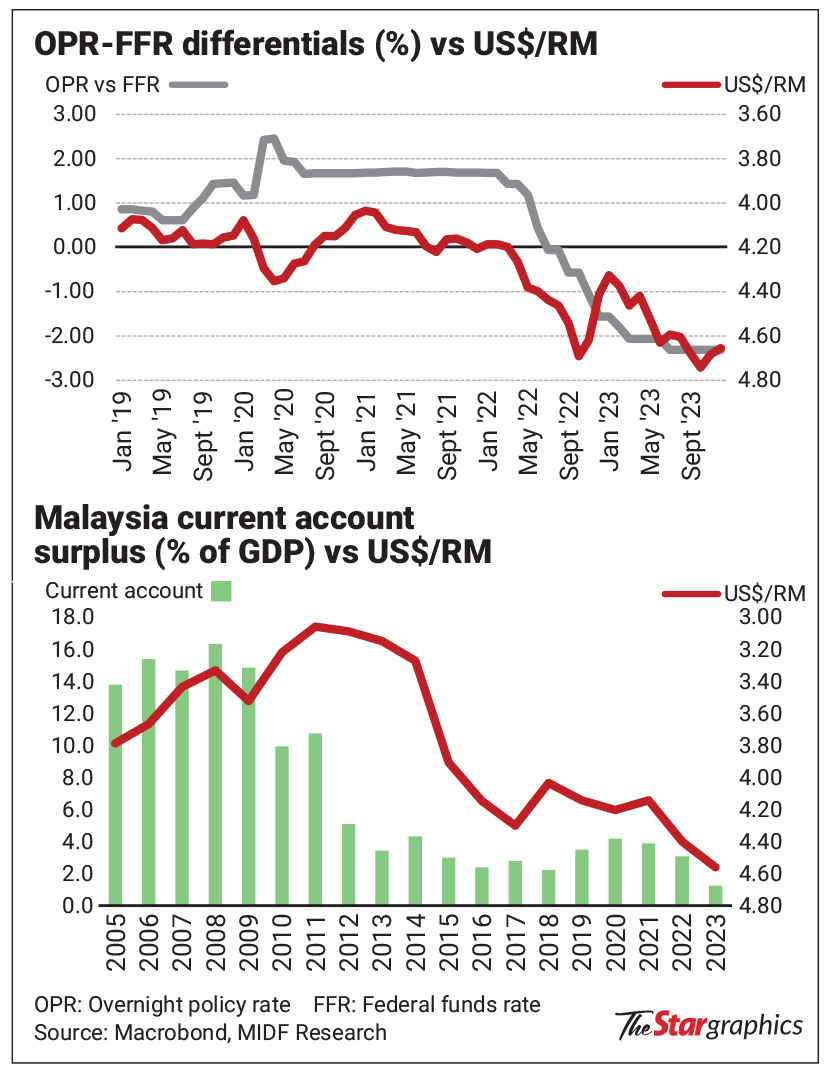

At the same time, Yeah explains that growth and interest rate differentials, commodity prices as well as current account and fiscal balances are also among the “hard” determinants of exchange rates, coupled with capital flows and transactions that drive supply and demand in the forex markets.

“There are also ‘soft’ determinants related to institutional quality, political stability, geopolitical events, investor confidence, sentiments and expectations that have varying degrees of power in explaining currency movements,” he stresses.

Yeah highlights that export-oriented economies like Malaysia tend to have undervalued currencies that provide a boost to export competitiveness, and therefore Malaysia’s export-oriented industries have benefited from a weak ringgit.

On the flip side, he points out that imports are more costly, and a noteworthy point he makes is that a weak ringgit deters structural upgrading as imports of capital goods and technology become more expensive.

He says: “Given the country’s present stage of development as an upper-middle-income country and its aspiration to achieve high-income nation status, it would be more beneficial for the country to have a stronger currency.”

Like many Malaysians, and Ferlito, Yeah is hoping the economic masterplans and sectoral blueprints unveiled by the unity government last year will herald the structural transformation processes, and projects that have commenced will enable the country to achieve high and sustained growth and productivity increases.

“That confidence and expectations will then have an enduring effect on the ringgit’s recovery and hoped-for upward trajectory,” he remarks.

Moreover, he identifies that Malaysia’s narrowing current account surplus, outward investment, the repatriations of profits and wages, capital outflows on top of softer inflows are some of the factors contributing to the weaker demand for the ringgit.

There are general concerns that the repatriation of profits by established multinational companies in Malaysia and the money being invested by Malaysian companies abroad are larger that the amount of investments and repatriation of profit that is coming into the country.

He suggests that the government continue to look for avenues to attract foreign investment, and to boost inbound tourism as well as facilitating foreign access to medical, educational and professional services as strategies that can boost demand for the ringgit.

Goh and Chia of UOB agree that while a weaker currency against multiple currencies a country trades with could boost its export competitiveness, how much the country imports in terms of intermediate inputs to produce exports, or imports for domestic consumption and investment purpose can offset the export advantage.

Hence, they reckon that if the import dependence is high, then a weaker ringgit becomes a bane because of the higher import cost that could nudge up inflation pressures.

“Malaysia’s share of goods imports to gross domestic product (GDP) rose from 48.6% in 2015 to 58.6% in 2022, but dropped to 49.8% in 2023 owing to weaker external trade.

“For larger firms, they may have options to hedge away the currency volatility or pass on the higher costs.

“But smaller firms and exporters that have lesser options will face more challenges,” they observe.

The duo are of the opinion that as Malaysia strives to move up the value-added curve and raise the economic complexity of its products, having a firm and stable ringgit would be more supportive to this objective.

Meanwhile, developing on Ferlito’s point of ensuring the execution of reforms, executive director and veteran economist at the Socio-Economic Research Centre (SERC), Lee Heng Guie, says a gradual approach and the proper sequencing of reforms, accompanied by mitigating measures would minimise economic as well as social pains.

He says: “The strength of the local note will depend on how well Malaysia sustains its economic growth in an environment of price and financial stability, as well as how we mend our budget deficit and contain debt and liabilities.”

Additionally, he says Malaysia should also rebuild both domestic and foreign investors’ confidence, revitalise domestic investment; and attract the inflows of dependable long-term foreign direct investments by ensuring the domestic equities market is appealing to portfolio investors.

Offering an alternate perspective, independent economist Julian Suresh Sundaram is adamant that the weak ringgit is less a reflection of domestic troubles but rather one that is global in nature, and that any move to repair the local currency should not be an isolated act but in lockstep with other currencies.

Speaking from a global point of view, Julian briefly enlists the macro aspects that can help improve the ringgit such as for the dollar to cease strengthening, the emergence of weaker US data, the Bank of Japan shifting its easy monetary policy stance as well as the improvement of China’s economic prospects.

Half-jokingly, he even adds that Malaysia can have more international artists booking their shows here!

Back home, he opines that there is little out there indicating a radical shift in domestic fortunes, both positive or otherwise.

“Malaysia has a steady economic trajectory, well-functioning financial markets with strong institutions and little prospects of significant financial market losses.

“In the meantime, is our political front any different from the upheavals seen in the rest of the world? So as long as the bureaucracy remains well functioning, a more dynamic political scenario is now a feature both here and the world over,” he muses, before adding that in the medium term, the fate of the ringgit is more influenced by factors outside the country.

Comparison with Singapore

With the ringgit topic being so hot these days, however, any gripes about foreign influence will undoubtedly invoke comparison with little sister Singapore, who in spite of the global macro scenario, have done well to maintain the strength of its currency.

Any comparison with Singapore is valid, given the republic was once part of Malaysia and share similar cultural and ethnic traits, apart from the fact that both currencies were once traded at parity.

One such example is the oft-stated negative impact China’s feeble recovery is having on the ringgit and more extensively, Malaysia’s export situation, until one realises that China is also Singapore’s largest trading partner.

CME’s Ferlito explains that the strength of the Singapore dollar is in its market status as a safe investment in times of uncertainty and as a regional reserve currency.

“Due to its position in the region and its solid reputation as a financial hub, the Singapore dollar is functioning like a ‘mini dollar’, playing the role of the US dollar to a certain degree in Asean,” he says.

Aside from that, he observes that higher interest rates in Singapore and the United States, possibly due to more lofty inflationary pressures, is also a reason for the strength of the Singapore dollar.

Looking into Singapore itself, Sunway University’s Yeah details that Singapore uses its exchange rate rather than interest rate as the monetary policy tool to manage growth and inflation. Its vast reserves affords it the luxury of using monetary policy to slowly target the currency for appreciation to combat against inflation.

He contends that similar to the strong greenback, the city-state’s appreciating currency will have the effect of reducing exports to China while making imports from China more cost-competitive.

Yeah says a strong Singapore currency will gradually result in cheaper Chinese goods and services flooding Singapore’s markets while its exports to China will eventually decline due to exchange rate-related cost factors.

Nevertheless, he adds: “Price is not the sole demand factor for high-value goods as quality, convenience, reliability and after sales support are equally important.

“Hence, if Singapore is able to raise productivity and create high-value products and services, its strong currency will not dampen its exports to China.”

Out of box ideas

After all that has been said, perhaps what Malaysia really needs are creative ideas that can help generate increased demand for its currency.

Co-founder and chief executive at Singapore’s Alta Alternative Investments Pte Ltd Kelvin Lee comments that despite the ringgit’s troubles, the fundamentals of the Malaysian economy are sound.

He reports: “From our interactions in Malaysia, we see renewed energy recently, particularly in agritech entrepreneurship. Entrepreneurship remains one of the best drivers of the economy, through increased productivity, job creation and growth.”

Kelvin believes that the establishment of family offices in Malaysia presents an intriguing avenue for enhancing the ringgit’s standing in the global market.

By definition, family offices are privately held companies that manage investments and assets for wealthy families.

Malaysia can leverage its strengths with its strategic geographical location, diverse cultural heritage and robust financial ecosystem to differentiate itself and position family offices as integral components of its economic growth strategy, Kelvin opines.

“The establishment of family offices in Malaysia has the potential to deepen the country’s financial markets, stimulate economic activity and enhance the global competitiveness of the ringgit,” he adds.

However, he acknowledges that careful consideration must be given to Malaysian regulatory, institutional and market specific factors to ensure the viability and sustainability of this initiative, even though it pays to create a conducive environment for wealth management as well as investment activities that the country can uniquely offer, as this will attract family offices and high-net-worth individuals.

“Recent initiatives by the Securities Commission, such as the Capital Market Development Fund, have been instrumental in providing grants and incentives to facilitate the growth of the financial services sector.

“Malaysia may consider launching more similar initiatives that offer financial support and capacity-building initiatives to nurture the venture capital ecosystem, thereby encouraging investment in innovative and high-growth companies,” says Kelvin.

Despite the dark clouds, most economists are still optimistic that the ringgit will strengthen from the second half of 2024, with UOB duo Goh and Chia as well as Yeah forecasting the local note to touch RM4.50 to the dollar by year-end, while MIDF Research is even more positive with a RM4.20 prediction.

Helping the ringgit will be the International Monetary Fund’s projection of global trade to grow by 3.3% this year from 0.4% in 2023.

Even the important semiconductor industry will see a reversal of fortunes with World Semiconductor Trade Statistics projecting to see sales rise by 13.1% in 2024 after contracting by 8.2% in 2023. The improvement in trade and semiconductor exports will support the economy and the ringgit this year.

Maybe ideas such as those shared by Alta’s Kelvin are what the ringgit needs as a shot in the arm.

Ultimately, economists are unanimous that Malaysia should be doing more to enhance its competitiveness for the ringgit, with SERC’s Lee telling StarBizWeek that the government has to address structural weaknesses through steady pace of reforms to enhance economic and financial resilience.

“These include rebuilding the strength of the fiscal balance sheet, strengthening the current account surplus and reserves accumulation, but more crucially, enhancing investment climate and investment prospects to sustain the inflows of long-term capital and corporate investment as well as to drive higher domestic investments,” he suggests.

As World Bank lead economist for Malaysia Apurva Sanghi sums it up in a nutshell tweet on X: “The ringgit is weak because of long-term decline in Malaysian competitiveness. If you want to lose weight, you develop good habits first. Weight takes care of itself. Address this decline and the ringgit will take care of itself.”

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.