THE year 2020 will continue to be in the memory and a talking point for many in years to come on how the Covid-19 pandemic has changed the world forever.

As with many other industries, Malaysian real estate investment trusts (M-REITs) have inevitably been adversely impacted by the pandemic during the various stages of movement control orders and resulting business disruptions.

That said, a closer look at M-REITs reveals the potential to poise for a rebound from the current depths and reach for greater heights post-Covid-19.

Though the pandemic affects most if not all the M-REITs, the impact it has differs depending on the portfolio asset concentration and focus.

M-REITs with asset portfolios focused on cyclical sectors such as retail and hotel are severely affected by consumer sentiment and movement restrictions, given the stringent lockdown of malls and strict curbs on travel-related activities.

While still fighting the pandemic, the industrial and services sectors, including healthcare and education sectors, have demonstrated relative resiliency on the back of tenancy structure which is typically a long-term master lease with fixed step-up in rental rates.

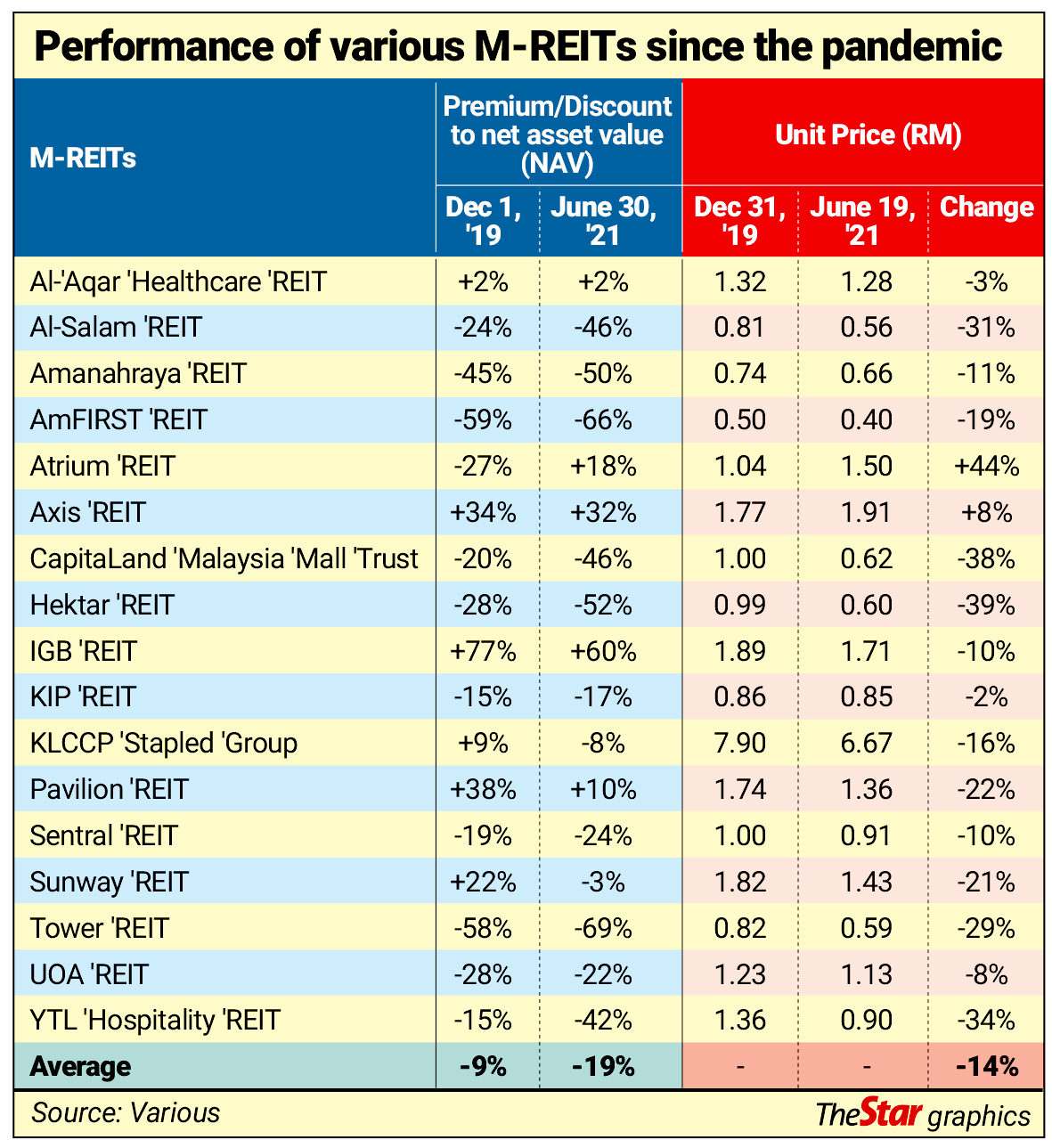

A look at the table shows that the unit prices of M-REITs have fallen by an average of 14%, due to the general decline in business performance, decrease in occupancy rates and drop in rental income during the pandemic.

Moreover, 14 out of 17 M-REITs suffered a drop in price-to-net asset value (NAV), and 12 out of 17 M-REITs are priced below their NAV, presenting an attractive entry point for potential investors looking to ride the post-pandemic economic recovery with long-term investments and regular dividend income distribution.

M-REITs collectively own a wide range of property assets, including many iconic malls, hotels, offices, medical centres, education buildings and industrial/warehousing properties – supporting tens of thousands of businesses and serving millions of Malaysians from all walks of life.

Recognising the public duty to bring much-needed positive impact to society, the economy and the country during this unprecedented time, M-REITs have risen to the challenge in providing support for various stakeholders, including rental relief and promotional assistance for tenants to ensure business continuity and long-term sustainability.

M-REITs have also shouldered the corporate social responsibility (CSR) of ensuring the safety of shoppers, tenants, guests and employees in the premises by adhering to strict standard operating procedures (SOPs) and investing in health, safety, security and environment (HSSE) technologies that enhance screening, cleaning and disinfecting routines.

This is especially important as many M-REIT assets host critical and essential services, from hypermarkets and hospitals to factories and logistics facilities, which are instrumental to the continuity of the supply chain and sustainability of the economy.

Staying lean to prepare for post-Covid-19 trends and opportunities. One thing that Covid-19 has highlighted is the need for businesses to be dynamic and agile to adapt to changes.

Being accountable to investors, M-REITs have been proactive and decisive in implementing difficult but necessary business decisions during the pandemic, including the reduction, cancellation and deferment of non-essential spending to contain costs, variation of income distribution frequency and income distribution payout as well as introduction of distribution reinvestment scheme to conserve cash.

Given the strict statutory borrowing limit of 50% of total asset value (TAV) before the pandemic, many M-REITs have inherently strong balance sheets – a saving grace amidst the current challenging business operating conditions.

Pursuant to the temporary increase in gearing limit to 60% of TAV as approved by the Securities Commission (SC) effective till December 2022, M-REITs have additional debt headroom to manoeuvre, if required, to meet their financial obligations and working capital needs in the event that the situation deteriorates further.

The pandemic has led to changes in consumer behaviours, accelerating the adoption of e-commerce and work-from-home (WFH) arrangements. This has led to opportunities for retail-focused M-REITs to migrate to omni-channel marketing through e-mall platforms to complement their existing physical retail malls.

Meanwhile, office-focused M-REITs are exploring strategies such as the repurposing of under-utilised office space to alternative uses such as smart commercial hubs and co-working spaces to adapt to future trends of hybrid work or rotational arrangement entailing alternate shifts between working from home and from office, which may potentially be common after the pandemic.

Moreover, as work-from-anywhere (WFA) is expected to persist globally beyond the current pandemic, the Malaysian office sector could potentially benefit from the relocation of multinational companies (MNCs) from developed countries to emerging countries or outsourcing of services to Malaysian professionals who are able to serve the world from relatively affordable co-working desks, office spaces and meeting rooms in Malaysia. These factors combined would continue to support the demand for office spaces in the long run.

The government’s efforts and progress in accelerating the pace of the national vaccination programme have been encouraging, moving Malaysia closer to a post-Covid-19 world and setting the stage for relaxation in movement control orders and for business activities to resume in the new normal.

Coupled with the expected relaxation of inter-district and inter-state travels, the self-reinforcing cycle of increased consumer spending, improved business sentiment, greater market confidence and decreased unemployment would lead Malaysia on the path to economic recovery – although the final boost of international borders reopening would be highly dependent on the success of countries across the world in containing the pandemic.

Inflation is a sign of growth, and the return of inflation, or reflation, would likely accompany economic recovery. Real estate assets have always been viewed as a traditional hedge against inflation and M-REITs may be attractive to investors in a reflationary post-Covid-19 world.

In line with the recovery of the economy, business operations, rental rates, and the increase in prices of goods and services, the performance of high quality and well-managed M-REITs are expected to improve, though the pace of recovery may differ depending on the underlying fundamentals of each M-REIT.

Meanwhile, the demand for e-commerce, healthcare, education, data infrastructure, logistics assets and high-tech warehousing with facilities such as automated storage and retrieval system or ASRS is expected to grow, in line with the ongoing digital transformation, evolving consumer preferences and increased focus on quality education and healthcare.

As the saying goes, “Resilience is a spring that when compressed, will bounce back”.

Though headwinds persist, after the trough comes recovery and expansion – there are silver linings for M-REITs, and clearer skies to come.

Datuk Jeffrey Ng is the immediate past chairman of the Malaysian REIT Managers Association and CEO of Sunway REIT Management Sdn Bhd. The views expressed here are his own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.