HOW far should the government go to boost house ownership?

Not at the expense of the banking sector, say economists.

Alliance Bank chief economist Manokaran Mottain says house ownership has always been one of the main agendas of the government, but “banks must always remain prudent with their lending policy”.

“Having good asset quality (referring to quality loans) is always a priority for banks,” says Manokaran.

According to a source, the responsible financing guidelines serve to protect individuals’ interest so that they borrow within their capacity to repay throughout the loan’s tenure.

This is to prevent borrowers from falling into financial hardship due to excessive debt burden that may lead to foreclosures, which undermine the objective of house ownership.

The source says the maximum tenure of 35 years is more than sufficient.

If the loan is offered to a 25-year-old, a tenure of 35 years would extend to 60. His retirement capacity during retirement would also be considered.

Increasing the tenure to 40 years will further add to the total cost of financing without significant improvements in the affordability of one’s monthly instalment.

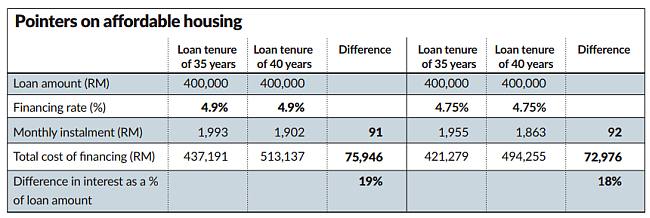

A loan tenure of 35 years will have a monthly instalment of RM1,993 compared to a 40-year RM1,902, a reduction of only RM91, with interest at 4.9%.

But the cost of financing would have risen by RM75,946. So the shorter the tenure, the lesser the total cost of financing.

Even with a lower financing rate of 4.75%, the difference in total interest costs between 35 and 40 years still works out to be 18% of the loan amount.

The source says longer tenure typically comes with higher financing rate due to the perceived risk of the longer repayment term. The mortgage reducing term assurance premium would also be higher the longer the tenure.

“The lower monthly repayments, made possible by longer financing tenures, may lead borrowers to over-estimate their ability to service the financing, and take a larger home loan than they can really afford,” the source says. With longer loan tenure, the borrower builds equity more slowly. Also, if the borrower decides to early settle the amount, the outstanding amount will be higher with an extended tenure to 40 years.

If the loan amount is RM300,000, at 4.9%, if the borrower decides to early settle after eight years, the outstanding amount is RM268,345 for a 35-year tenure versus RM276,342 for a 40-year tenure.

Based on benchmarking, the common tenure for home loans are 25 to 30 years. Singapore has capped the maximum tenure of all new private residential loans at 35 years from October 2012. Hong Kong Monetary Authority has imposed a 30-year ceiling for all mortgages from September 2012.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.