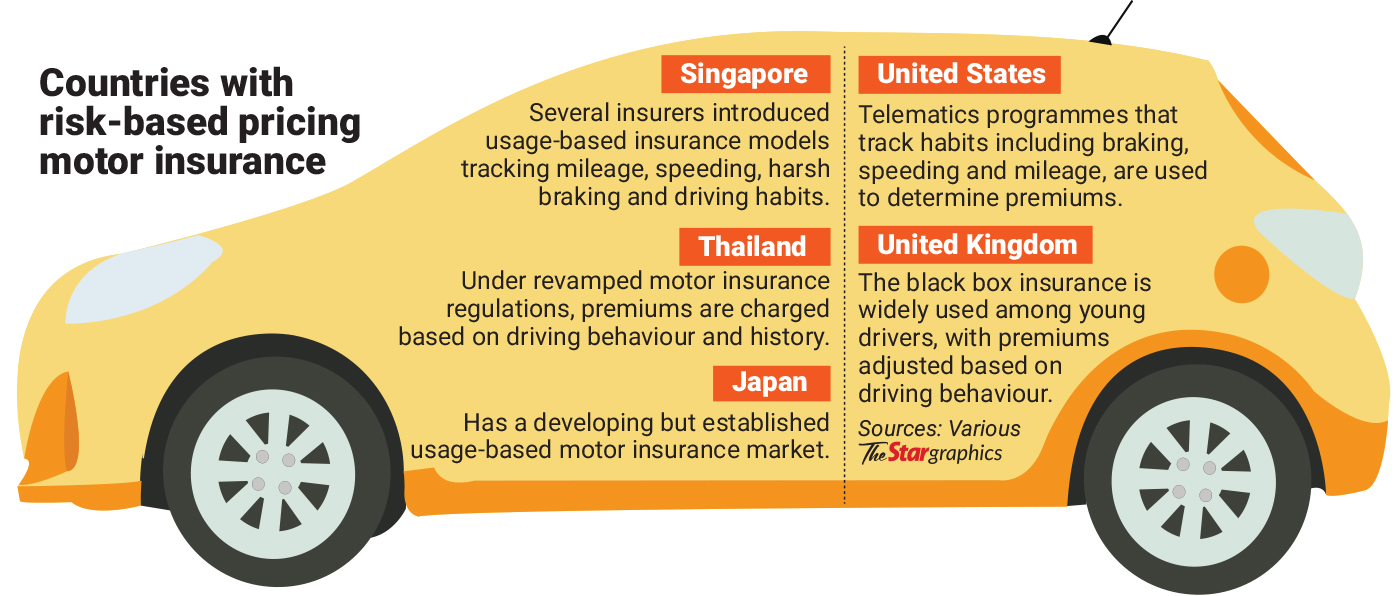

PETALING JAYA: Motor insurance premiums in Malaysia could soon depend more heavily on how safely one drives, in a move aimed at reducing road crashes and rewarding responsible motorists.

Under the proposed risk-based pricing model for motor insurance, the framework aims to reward safer drivers with better premiums and possibly discounts.

“Currently, there is a degree of cross-subsidisation where lower-risk motorists are offsetting the higher claim cost of others. We are working closely with Bank Negara Malaysia and related government agencies to see how we can further improve road safety and behaviour,” said General Insurance Association of Malaysia (PIAM) chairman Ng Kok Kheng.

According to him, risk-based pricing is already a standard for most insurance products, such as medical insurance.

ALSO READ: ‘Lower premiums must come with safeguards’

“Pricing depends on the cost incurred through claims, which are then translated into the premiums paid.

“While motor insurance remains a regulated industry, any enhancements to the framework implemented must remain fair, transparent and appropriate for consumers,” he said.

“The end goal is to reduce the number of road accidents and road fatality rates.”

Ng said a major pillar of the initiative is to build supporting infrastructure with industry, ideally requiring reliable, timely data from relevant enforcement and regulatory agencies to establish a comprehensive, integrated claims and risk database.

“This allows better predictive modelling, allows early identification of high‑risk driving patterns, supports incentivising good driving behaviour and identifies interventions required for risky driving behaviour in alignment with the public road safety agenda,” he said.

Ng said it is also important to help motorists understand how their risk profile affects their premiums over time, which can include driving behaviour and claims history.

“This may require careful implementation and consumer understanding. We want to do it in a way that is as fair as possible,” he said.

Ng added that it is difficult to set a deadline for this initiative due to its complexity.

“It’s not an easy task to manage, and we also have to see if the industry is ready.

“Currently, there is a partial risk-based pricing system for motor insurance, operating within a set range to maintain stability,” he said.

On how this differs from the current motor insurance framework, which rewards drivers based on their No-Claim Discount claims history, he said that the risk-based pricing model incorporates a broader range of risk factors.

This includes driving behaviour, accident frequency, traffic offences, vehicle usage patterns and other relevant underwriting indicators, enabling premiums to reflect an individual’s risk exposure more accurately.

“Beyond rewarding responsible drivers, the industry hopes this framework encourages a collective focus on road safety and improved driving behaviour.

“It establishes positive reinforcement for good driving behaviour that not only promotes compliance with traffic law but ultimately makes the roads safer for all,” Ng said.