MALAYSIA took a giant step in streamlining its steel sector with the introduction of the Steel Industry Roadmap (SIR) 2035 recently.

The core objective of the blueprint is to ensure the industry remains healthy, not only based on production capacity and supplies, but also well-positioned to meet net-zero targets.

The steel industry is one of the largest carbon emitters, and steps must be taken to ensure production practices are environmentally friendly and sustainable.

In unveiling the roadmap, 15 strategic incentives were recommended that will take the steel industry to net-zero emissions by the year 2050.

Missing the trees

While the general intent of SIR is clear and well defined, there are genuine areas of concern that exist today that are detrimental, especially to the local steel producers.

The proposed reform to tackle overcapacity in the upstream sector via licensing requirements and to address the sector’s imbalances only addresses part of the real issue at hand.

The steel industry is a strategic sector valued at RM26.4bil, contributing 1.7% to the nation’s gross domestic product.

The sector is also a significant contributor to the country’s merchandise trade with a 2.4% share valued at RM62.5bil.

It is a core supplier of raw materials for infrastructure and property development, as well as the manufacturing industry.

The sector also provides 283,000 high-paying jobs and must remain sustainable to ensure the industry is able to not only compete but also grow at the same time.

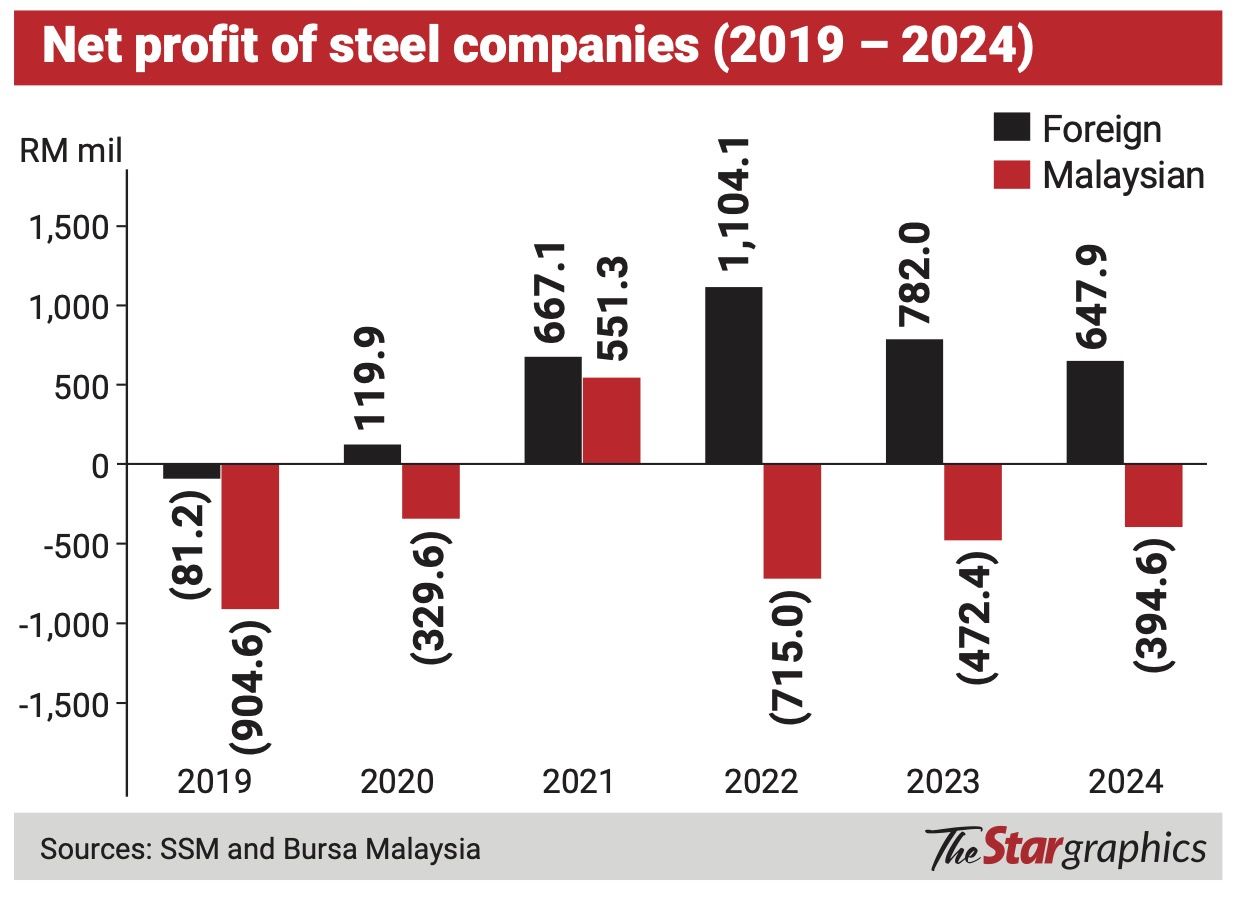

The industry faces a significant threat from the dominance of foreign-owned steelmakers, which now control over 83% of the market by volume of tonnage, driven by the emergence of large foreign players with production capacity that is three times more than local steel producers.

Annual production has dwindled to just nine million tonnes due to intense competition.

Hence, any steel industry roadmap must address the uneven playing field, without cost increases to consumers, and at the same time, safeguard the local supply chain via the distribution and retail network.

With foreign-owned mills dominating the industry, the foreign-owned steel mills’ market share is projected to reach 90% in the next few months.

With the strong presence and backing from their headquarters, these foreign-owned steel mills have employed a pricing strategy to gain market share, forcing locally-owned companies into unsustainable losses to the tune of RM2.26bil over the past six years.

A check with Companies Commission Malaysia data, as well as data from listed companies, suggests that foreign players have benefitted from positioning themselves in the market, at the expense of local steel producers, with a cumulative net profit of RM3.24bil over the same period.

Polluting plants

The foreign-owned steel mills utilise high-emissions blast furnace (BOF) technology, which emits up to six times more greenhouse gas (GHG) per tonne of steel than the cleaner electric furnace technologies used by Malaysian-owned mills.

Foreign-owned BOF mills are run by importing environmentally harmful iron ore and coal that emit large quantities of GHG to produce steel products.

Due to their dominance, and if left unchecked, these foreign-owned steel mills will be able to shape the whole building materials supply chain, from the downstream manufacturers to distributors and thereafter to contractors and end-users.

While they are able to sell to the market at competitive prices, the fear is that once they reach clear dominance, they will be able to raise prices and cause inflationary pressure on steel products.

The misguided SST

Foreign-owned mills enjoy a 15-year tax exemption as well as significant capital allowances.

They also pay 0% sales and service tax (SST) on imported raw materials such as iron ore.

In contrast, Malaysian-owned mills are burdened with a 5% SST on their primary raw material, which is mainly steel scrap.

With preferential treatment given to foreign downstream enterprises, Malaysian-owned companies risked being sidelined from this vast economic sector.

The government should instead prioritise the locally-owned steel mills, as well as create a level playing field.

With the introduction of a comprehensive carbon tax for energy emitters as proposed under the SIR, though crucial, it is time-consuming and difficult to implement.

Local steel mills do not have the time or the luxury to benefit from the government decarbonisation policy, as they are being crowded out by foreign-owned millers.

The locally-owned steel plants need immediate, practical measures to provide them with “breathing space” and restore market equilibrium, while long-term solutions are being finalised.

While the government has granted tax reliefs to these foreign-owned steel plants, enabling them to chalk up huge profits, efforts must also be made to recoup some of these profits if they are repatriated back to their home country in the form of dividend tax of at least 10%.

These funds should then be ring-fenced to assist local steel millers to play catch-up in terms of plant modernisation as well as decarbonisation towards net zero.

Sustainability

The removal of SST on scrap metal will allow the locally-owned steel mills to conduct strategic capital investment for long-term sustainability of the industry, as well as the downstream supply chain.

Locally-owned steel millers can restore deferred maintenance and upkeep to improve operating efficiency and reduce energy consumption, move towards sustainable practices, and align Malaysian-owned steel producers with the global decarbonisation agenda and the National Energy Transformation Roadmap, as well as the New Industrial Masterplan 2030.

With this, Malaysian-based steel companies can jointly plan new large-scale, low-carbon facilities and remain competitive in the market.

Among the fifteen strategic proposals under the SIR is the setting up of a Carbon Competitiveness Fund, which will support co-investment in green transition and innovative products.

This is a low-hanging fruit and should be expedited to help low-emission Malaysian-owned mills to upgrade their ageing facilities to remain competitive and in business.

In conclusion, the steel industry is headed towards a complete monopolisation by foreign interests at the expense of Malaysian-owned steel plants.

The industry’s supply chain and sectors that depend on steel products may be subject to higher prices in the future if concrete measures are not taken to resurrect the local players.

Foreign-owned steel mills should be encouraged to produce higher-grade steel products not produced by locally-owned mills that are currently imported.

These foreign-owned plants can use their BOF technology appropriately and maintain their business margins, thus reducing overcapacity in the construction-grade market.

A secure and stronger local steel industry protects jobs and creates new, high-skilled, high-value employment, cementing the long-term future for Malaysian workers with new investments that are more environmentally friendly.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.