THE National Property Information Centre (Napic) recently released the 2024 property market update which showed that while overhang has dropped considerably, there has been some uptick in terms of construction activities.

Starts and new planned supply for the residential sector rose by 20.6% and 24.1% year-on-year (y-o-y) to 106,236 units and 100,461 units respectively. At the same time, the number of residential unsold units that are under construction increased by 19.2% y-o-y to 60,934 units.

There was a similar trend in the commercial segment, particularly serviced apartments, with unsold and under-construction units increased by 27.2% y-o-y to 30,279 while construction activity starts and new planned supply leapfrogged 117.3% and 106.2% to 39,011 and 40,105 units respectively.

These figures are the highest in five years based on Napic’s data.

Based on the latest quarterly results, the property sector performance has beaten sales forecasts while a select few surprised the market with improved bottom lines. Not surprisingly, the strong showing reflects an upbeat property market.

Volume and value of transactions surged to an all-time high of 420,545 units involving a staggering RM232.3bil in 2024, up 5.4% and 18.0% y-o-y respectively. Transaction volume and value in the residential segment, however, lagged the overall market, rising by just 4% and 5.9% y-o-y.

The commercial sector was the star performer with transaction volume and value surging by 13.6% and 51.6% y-o-y respectively.

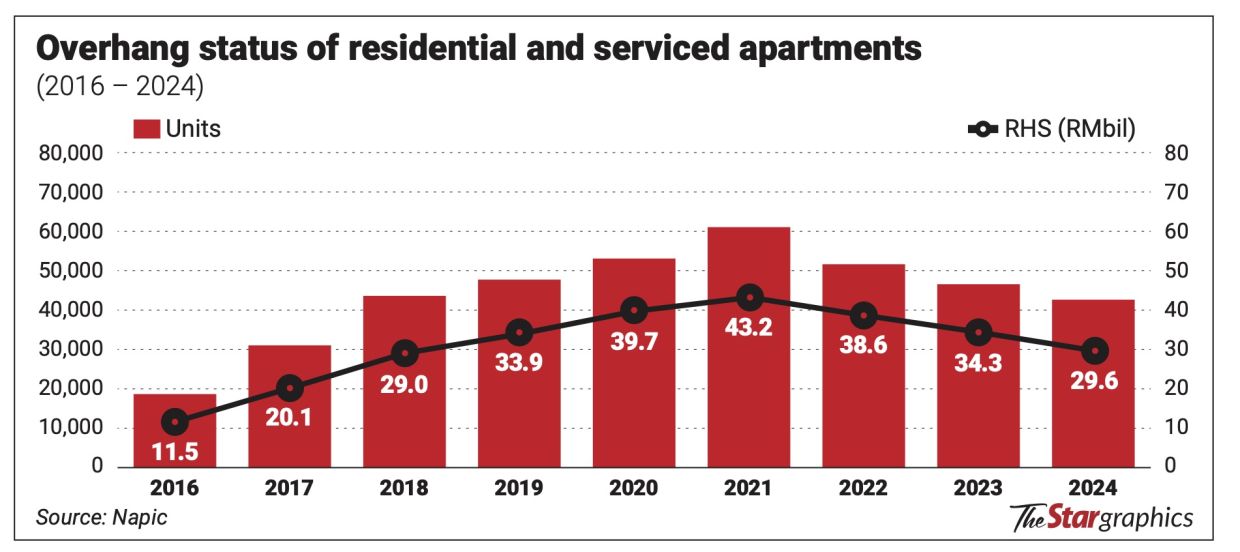

For the second year running, Napic’s annual data showed a further reduction in overhang properties. For this column, where residential properties include serviced apartments, the total overhang volume fell by another 8.4% y-o-y to 42,713 units, while in terms of value, there was a 13.6% decline to RM29.64bil.

Residential overhang dropped to 23,149 units worth RM13.94bil, or 10.3% and 21.2% respectively while serviced apartments overhang fell to 19,564 units worth RM15.7bil, a marginal decline of 6.1% and 5.6% y-o-y, respectively.

Overall, the 2024 overhang volume is the lowest since the the end of 2017 with 31,102 units, while in terms of value, it is just RM0.62bil above the level seen in 2018.

Since hitting the peak in 2021, the residential segment has now declined by 13,714 units or 37.2% worth some RM8.85bil or 38.8%.

As for the serviced apartment segment, the current overhang level is lower by 4,732 units or 19.5% worth some RM5.76bil or 23.3% from the peak overhang level seen in 2021 (see chart).

However, within the Small-office-Home-office (SoHo) segment, the overall market overhang increased marginally, rising by 11.0% and 2.7% to 1,872 units worth RM1.16bil respectively.

As the increase in both the numbers and value can be attributable to the sharp decline in 2023 when both fell by 24.7% and 22.0% respectively from the preceding year, the slight increase last year is not alarming.

Geographically, Kuala Lumpur recorded the highest number of residential overhang units with some 4,234 units worth RM3.38bil, representing 18.3% and 24.2% of the market respectively. This was followed by Johor with 2,964 units valued at RM2.89bil, which accounts for 12.8% and 20.7% of the total respectively.

Interestingly, condominiums and apartments made up the lion’s share of the overhang, representing 60% of the total in the residential segment.

In the serviced apartment segment, Johor has the highest number of overhang at 10,624 units worth RM8.97bil, representing 54.3% and 57.1% of the total.

As expected, most of these units are in the Johor Baru district. Kuala Lumpur is the next hotspot for serviced apartment overhang with 4,202 units worth RM4.03bil, representing 21.5% and 25.7% of the market overhang.

Higher prices

As 18,445 units worth some RM13.61bil representing 30.2% and 31.5% in terms of volume and value of the market overhang have been removed from the peak three years ago, it is natural that market prices have inched up.

Overall, the Malaysian House Price Index (HPI) rose by 3.3% y-o-y, slightly ahead of the increase in the Malaysian Consumer Price Index, which was up by 1.7% in 2024.

The trend of stronger market price growth vis-a-vis the headline inflation rate suggests that in overall terms, the property market remains a good inflation hedge for property owners and investors.

However, the price growth in the 4Q period alone was negative, dropping by 2% y-o-y, although on a quarter-on-quarter basis, the HPI improved by 1.5%.

With record-breaking transaction volume and value in 2024, it will be tough this year on several counts.

As it is, based on several large developers’ forward guidance for this year, the sales target from new launches has been lowered by 7% overall.

While property remains largely affordable, the slight increase in prices for new properties on the back of higher costs (labour, materials and compliance) may see softer demand.

Having said that, there are also positives, especially demand from overseas buyers under the Malaysia My Second Home programme as well as the sustained demand in the Johor property market, driven by the Johor-Singapore Special Economic Zone and the Rapid Transit System line connecting Johor Baru to Singapore.

As the property market had an excellent 2024, driven by record high transaction volume and value as well as higher overall market prices, the outlook for this year is clouded by the increase in the number of residential and serviced apartments that are categorised as unsold under construction.

The increase in construction activity in the residential and serviced apartment segments is a fresh concern. Malaysia should take steps to ensure the market overhang between 2016 and 2021 is not repeated. Hence, despite the dip in overhang data in 2024, industry players must be vigilant to ensure past mistakes are not repeated.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.