IN Budget 2023, the total debt service charges (DSC) were estimated at RM46.1bil. As a percentage of total government expenditure, the DSC is expected to be at 15.4%.

As it is, this is already higher than the self-imposed 15% limit that Malaysia has adhered to.

Yet, the DSC ratio for Budget 2024 is rising even further to 16.4%, as the DSC in absolute terms will increase by 8% or RM3.7bil to RM49.8bil.

With total federal government debt continuing to rise, Malaysia’s DSC is only expected to grow over time, as failure to reign in budget deficits will only see the country continuing its debt dependency.

Rising debts

Although the budget deficit is expected to be lower in 2024, running a budget deficit means the government does not have enough revenue to pay for all its operational and development expenses.

For next year, the government estimates a budget deficit of RM85.4bil, which suggests that the government will have to raise almost a similar amount to finance almost the entire net development expenditure (DE) of RM89.2bil.

This will see the federal government debt rise to RM1.23 trillion, translating to a debt-to-gross domestic product (GDP) ratio of 62.4%, 0.4 percentage points higher than this year’s level of 62%.

Under the Public Finance and Fiscal Responsibility Bill, 2023 (PFFR), which was approved by Dewan Rakyat last week, the statutory debt-to-GDP ratio is expected to marginally surpass the ≤60% target as the ratio is expected to be at 60.1% this year and 60.6% next year as seen in Figure 1.

Debt-funded growth

One of the pertinent questions among economists is the minimum level of government spending in the form of DE that is needed to sustain economic growth.

Surprisingly, under the PFFR bill, the government recognised that it needs to spend at least 3% of GDP for DE to ensure economic growth.

Based on the data in the accompanying table, the government spent between 3.5% and 4.1% of nominal GDP between 2018 and 2022 and is expected to spend 5.2% of nominal GDP this year, and this will drop to 4.5% next year.

Overall, between 2018 and 2024, Malaysia’s DE is at about 4.1% of its nominal GDP. This brings us to the question: Is Malaysia fuelling economic growth via borrowings?

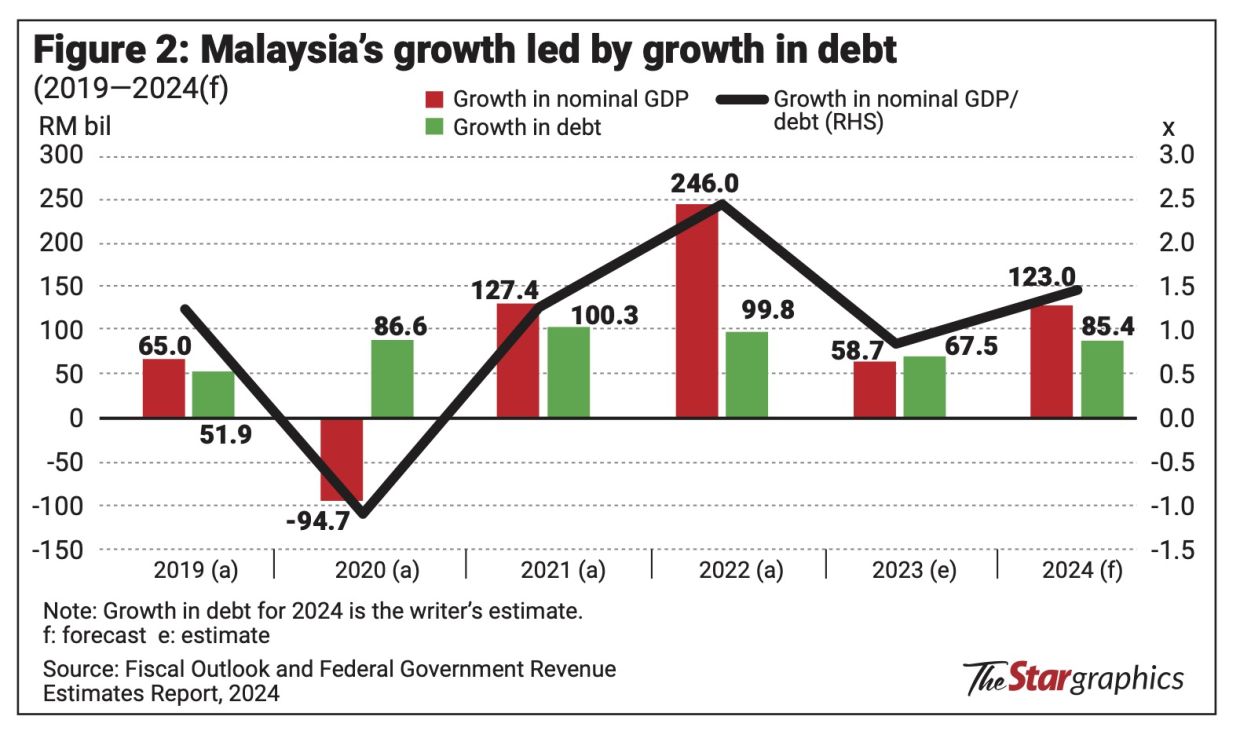

The short answer seems to suggest so, as Malaysia’s debt expansion more or less mirrors the growth of nominal GDP in absolute terms with the last six years’ average nominal GDP growth at 1.07 times of growth in federal government debt as seen in Figure 2.

But what is real DE?

In Budget 2023, one of the pertinent reasons why DE ballooned to RM96.3bil is due to the US$3bil 1Malaysia Development Bhd (1MDB)-related debt that was parked under it.

In addition, as highlighted in this column before, debt payments made for public-private partnerships (PPP) and public finance incentives (PFI) were also parked under DE.

Under Budget 2023, this was some RM7.2bil, leaving the net actual DE at just RM74.6bil.

Under Budget 2024, without any payments due for 1MDB-related debts, the total DE is approximately RM78.9bil, or RM4.3bil, a 5.8% year-on-year (y-o-y) increase from this year’s budget.

Malaysia, despite focusing on attaining fiscal discipline, can’t seem to run away from raising new debts using the off-balance sheet method or under the PPP/PFI arrangements.

For Budget 2024, the PPP/PFI payments alone totalled approximately RM11bil, a whopping 53.7% y-o-y increase from this year’s figure.

Key ministries that are expected to see a huge jump in PPP/PFI payments parked under DE are the Works Ministry at RM2.05bil from just RM261mil this year, followed by the Local Government Development Ministry at RM1.51bil from just RM49mil this year.

Meanwhile, the Prime Minister’s Department will see PPP/PFI payments amounting to RM1.23bil next year from the RM942mil that is estimated for this year.

Malaysia’s core debt

Outside the federal government debt, Malaysia has two other buckets of debt and this includes some RM221bil in the form of committed guarantees and another RM142.2bil in the form of other liabilities.

These core borrowings are not going to go away anytime soon, but to the contrary, with the government’s commitment to building large infrastructure projects, the numbers can only go up.

Under committed guarantees, the key debts are debts held by transport agencies and they include Danainfra Nasional (RM82.9bil); Prasarana Malaysia (RM42.9bil); and Malaysia Rail Link (RM34.9bil).

These three alone account for RM160.6bil or 72.5% of the total committed guarantees.

Other liabilities is another bucket of debt, comprising three main components totalling some RM142.2bil.

This includes 105 projects worth some RM93.8bil under the PPP model or almost RM900mil per project, RM45.9bil worth of projects under the PFI model, and another RM2.5bil under PBLT Sdn Bhd.

Although the government intends to pare down its exposure under other liabilities, the numbers over the years have remained relatively flat and it is hard to see if this is going to go down anytime soon.

In essence, while the government recognises that it needs to have greater fiscal discipline, the numbers as far as the debt-to-GDP ratio and DSC remain elevated and worrying.

Pankaj C Kumar is a long-time investment analyst. The views expressed here are his own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.