ONE of the closest barometers for the ringgit is the correlation with foreign portfolio flows, and for the local bourse, a continuous inflow of foreign funds suggests that the market is in for a good run.

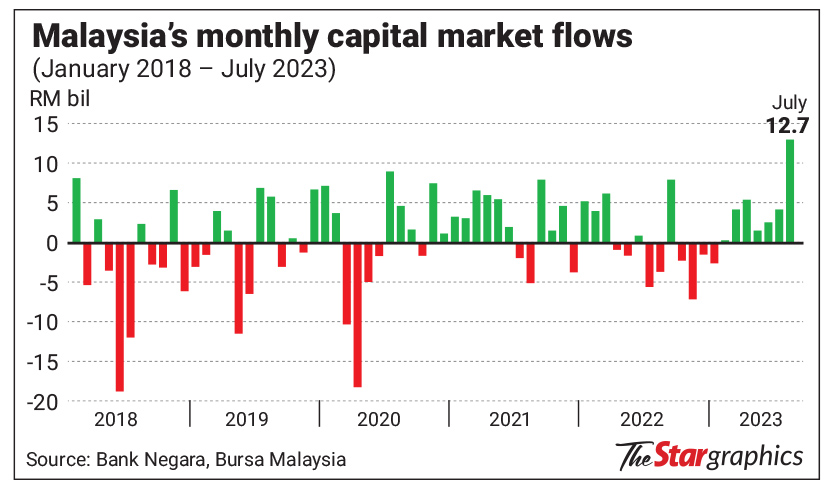

So far this year, based on data compiled by Bursa Malaysia and Bank Negara, foreign portfolio inflows into the Malaysia capital market have been strong with total cumulative net inflows up to July 2023 at RM29.6bil, led by the bumper inflow of RM12.7bil last month as seen in the accompanying chart.

The July inflow was mainly due to the massive inflow of some RM11.3bil in the Malaysian fixed-income market while the equity market saw an inflow of RM1.4bil last month.

Carry-trade, inexpensive ringgit

For foreign investors, there are only two reasons to buy Malaysian fixed-income instruments and this is either related to the current yield spread vis-a-vis other foreign jurisdictions; or in anticipation of capital gains, which foreign investors may realise on the back of the strengthening ringgit or drop in the benchmark yields.

As for the first reason, if one were to take the benchmark five-year and 10-year Malaysian Government Securities (MGS) papers, the average traded yield in July 2023 was at 3.62% and 3.87% respectively, which is not significantly higher than regional peers and much lower than what US treasuries offer sovereign bond investors.

Based on the current yield on the 10-year MGS at 3.85%, the local sovereign paper is only higher than Canada (at 3.69%), half of Europe (which trades between as low as 0.95% in Switzerland to as high as 19.5% in Turkiye), Japan (at just 0.64%), Singapore (3.26%), Thailand (2.58%), Vietnam (2.68%), China (2.56%), and Taiwan (1.21%).

However, when viewed with Malaysia’s current credit rating of A- by Standard & Poor’s, Malaysia’s rating is only higher than that of Thailand and Vietnam as these two countries are rated BBB+ and BB+ respectively. Hence, the argument of foreign inflows into the Malaysian fixed-income market for carry trade purposes has little weight as there are other much more rewarding options out there, and to start with, the US treasuries.

Although in July, the 10-year US treasuries only gave investors almost identical returns when compared with the similar 10-year MGS, the yield spread has now widened to more than 40 basis points as the 10-year US treasury paper has now spiked to almost 40 basis points against the current yield on the 10-year MGS at 3.85%.

Hence, the other underlying pull factor has to be the inexpensive ringgit, which in July traded at about RM4.5939 to the US dollar and down some 4.6% since the end of last year’s close of RM4.3900 to the dollar and lower by 8.2% from its year’s high of RM4.2450 against the greenback.

Short-term funds must have positioned themselves in anticipation of a weaker dollar, which in turn would result in foreign exchange gains once these positions are closed.

After all, with Bank Negara not expected to raise the overnight policy rate any higher, these portfolio inflows are in for both capital gains as well as foreign exchange gains.

This also perhaps explains the increase in Bank Negara’s international reserves, which rose by US$1.5bil in July to US$112.9bil from US$111.4bil as at the end of June 2023.

Net buyers

Foreign shareholding, which stood at 20.6% as at the end of June 2023, remained unchanged in July despite the net inflow of some RM1.41bil.

For July, the total market capitalisation of foreign-owned shareholdings improved by 5.2% month-on-month to RM361bil, in line with the increase of the total market capitalisation of Bursa Malaysia, which rose by a similar quantum to RM1.757 trillion from RM1.669 trillion as at end of June 2023.

For this month, the inflows have been relatively lighter with a total net inflow of about RM160mil as at Aug 24, 2023. Year-to-date, the foreigner has remained net sellers with a total outflow of RM2.62bil.

However, since they turned net buyers on July 12, the market has seen total inflows of about RM1.94bil, which also allowed the FBM KLCI to gain some 3.8% or 53 points over a space of 31 market days.

Higher for longer

While the US Federal Reserve (Fed) is seen pausing after it makes another 25 basis point hike next month, investors are also concerned on the tone of the Fed’s narrative based on the latest minutes of the Federal Open Market Committee (FOMC) meeting.

The FOMC officials expressed worries on inflation and commented that more hikes are necessary in the future unless conditions change.

Hence, the FOMC will likely remain hawkish, given its dependence on economic data points from hereon, especially those related to core personal consumption expenditures and the stretched labour market.

While disinflation is well underway, the Fed’s concern on the pace of decline in inflation prints probably warrants the hawkish tone.

With both the 10-year and 30-year at unprecedented levels, rising by 28 basis points and 30 basis points this month alone, this has also allowed the dollar to regain some strength and was last seen at 104.20, up 2.3% this month alone.

In addition, with the ringgit highly correlated with the movement of the yuan, the People’s Bank of China’s move to cut interest rates this week by 10 basis points for the one-year loan prime rate to 3.45% is not helping either as a weaker yuan drags the ringgit lower.

The ringgit, which was last seen at RM4.6450 to the dollar has weakened by 3.2% this month alone.

Flows may reverse

Until and unless the Fed turns dovish and China stops cutting its benchmark interest rate, the ringgit is likely to remain under pressure and hence the capital market inflows seen in the past few months will likely reverse.

As it is, over the past six market days alone, foreign outflows totalled RM371.6mil.

However, as we are nearing the pivot point as far as the global interest rate is concerned, some funds will likely hold their unrealised loss positions until the inevitable occurs – a pause in the US rate hike cycle followed by a similar move by other central banks.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.