DESPITE global volatility from prolonged US tariff tensions, geopolitical risks and elevated interest rates, Malaysia’s financial market remains stable and resilient.

The market continues to function efficiently, supported by strong macroeconomic fundamentals, a well-capitalised banking system and a vibrant capital market that sustains economic activity.

A supportive monetary policy stance together with a strengthening ringgit continues to buoy investor confidence. In July, the central bank cut the overnight policy rate (OPR) by 25 basis points to 2.75%, the first reduction in the OPR since May 2023, to safeguard growth amid moderating inflation.

The statutory reserve requirement (SRR) was also lowered to 1% to boost liquidity. These moves led to lower lending and deposit rates, easing borrowing costs for households and businesses.

The ringgit strengthened 5.8% to RM4.23 against the US dollar by end-August, ranking among Asia’s top-performing currencies, reflecting a weaker greenback amid US Federal Reserve rate cuts and fiscal concerns, steady Chinese growth and Malaysia's sound fundamentals.

The ringgit may see more gains in anticipation of further US interest rate easing as well as Malaysia's ongoing policy reforms.

Malaysia’s banking system remains robust, with capital ratios comfortably above regulatory minimums (CET1: 14.9%; total capital: 18.4%) and a strong liquidity coverage ratio of 158.4%. Asset quality remains sound, with low impaired loans at 1.4% and ample provisioning buffers.

Total loans grew 5.4% year-to-date to RM2.31 trillion, driven by sustained household and business demand. Small and medium enterprise financing expanded 8.2% to RM410.4bil, reflecting strong working capital needs.

Household debt, while high at 84.8% of GDP, remains manageable, supported by rising incomes and prudent lending standards. Despite global uncertainty, Malaysia’s capital market continues to thrive as a key funding avenue.

Private sector fundraising rose 8.2% to RM75.9bil in the first seven months of 2025, with strong corporate bond issuance (7.2%) and equity fundraising (29%), including 38 new initial public offerings worth RM4.3bil.

Public sector issuances moderated in line with fiscal consolidation efforts.

Corporate bond yields declined across all ratings amid strong investor appetite and lower inflation expectations, while Malaysian Government Securities yields trended lower on foreign inflows.

The Economic Outlook 2026 expects easing global rate environment and Malaysia’s policy clarity to sustain demand for both sovereign and corporate debt.

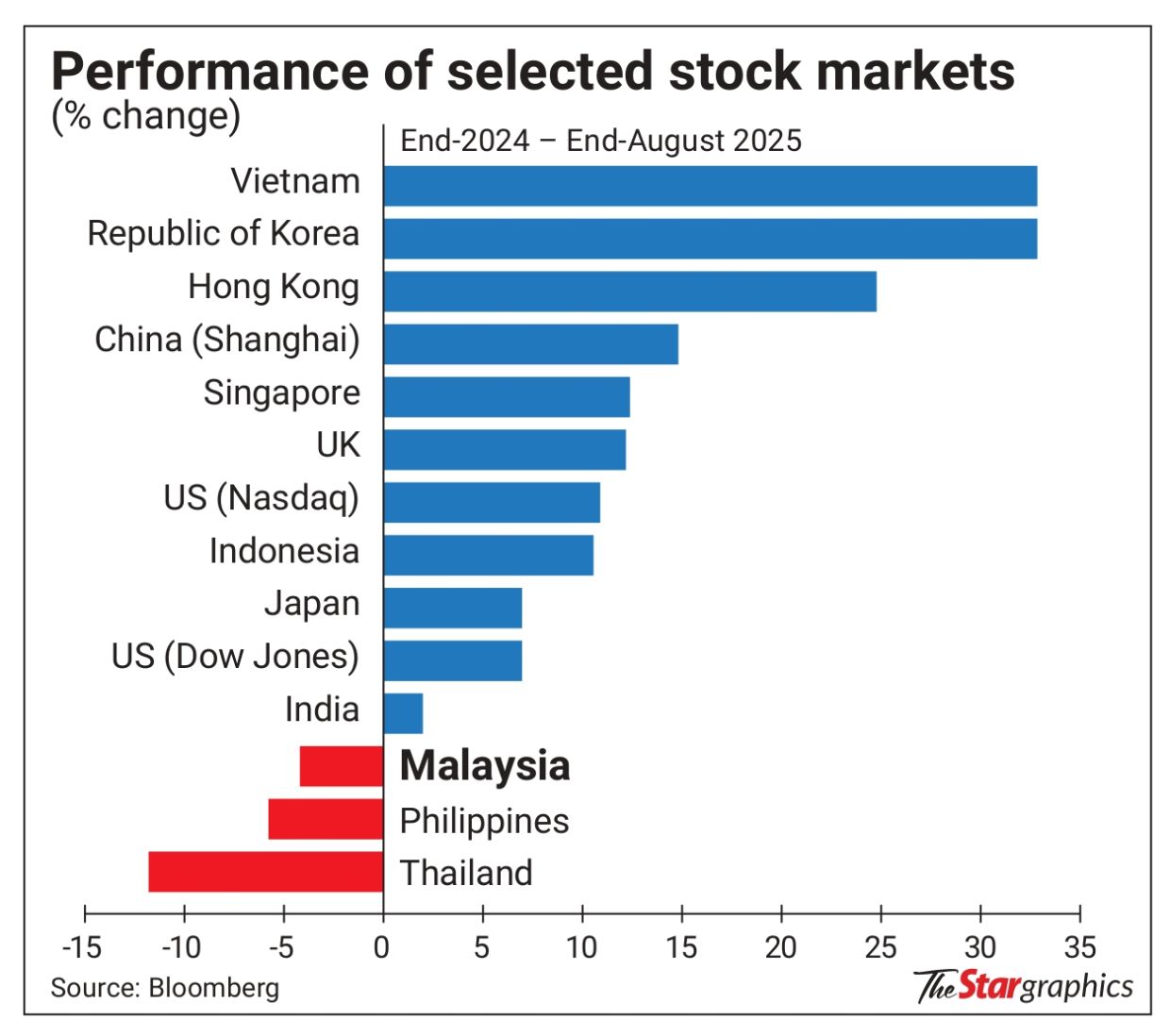

The FBM KLCI staged a recovery from April’s tariff-driven dip to close August at 1,575 points, buoyed by foreign inflows, stronger domestic consumption and expectations of Fed rate cuts. Market capitalisation reached RM1.95 trillion, with healthy trading activity and stable foreign participation at about 19%.

Looking ahead to 2026, the local bourse is poised to benefit from stable politics, robust consumer spending and ringgit strength. The upcoming Capital Market Master Plan 4 — a 20-year roadmap focusing on sustainability, inclusivity and collaboration — aims to position Malaysia as a regional leader in sustainable finance.

Overall, Malaysia’s financial outlook remains positive. Supportive monetary measures, sound banking fundamentals and thriving capital market activity underpin resilience amid external headwinds. Strengthening Islamic finance and ongoing structural reforms under the Ekonomi Madani framework reinforce Malaysia’s trajectory toward sustainable and inclusive economic growth.