Bank Negara’s latest rate hike is controlling price pressures in more ways than one

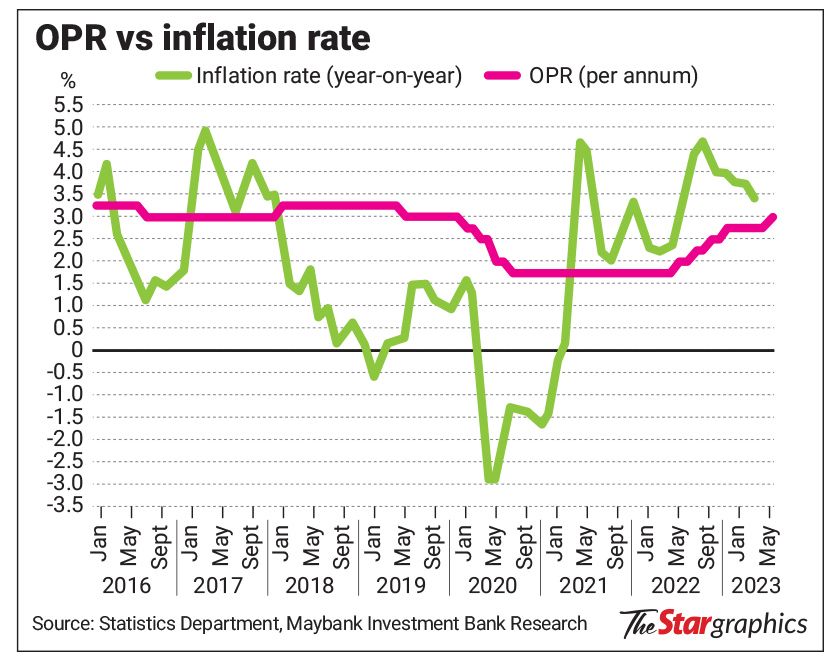

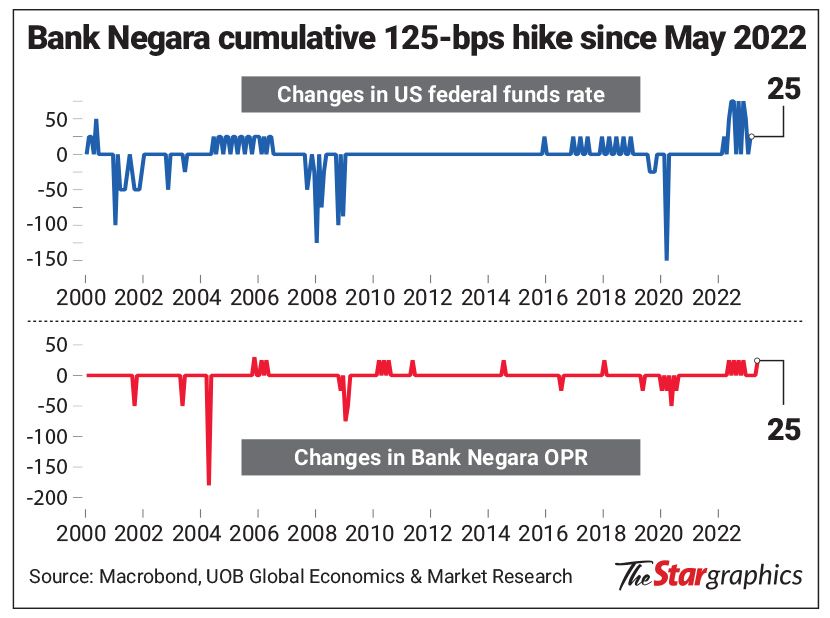

EARLIER this week, Bank Negara surprised many in the local economic and monetary spheres by having its Monetary Policy Committee (MPC) raise its overnight policy rate (OPR) by 25 basis points to 3%.

As is well known by now, the central bank says the latest move comes as the balance of risk to the inflation outlook is still biased to the upside, while making the judgment that it is timely at present to further “normalise” monetary accommodation in light of sturdy domestic economic growth.

Interestingly, the move, while possibly inflicting discomfort on certain segments of society, particularly those servicing loan repayments, is a precautionary measure against factors that could jack up inflation in the near future, according to several economists surveyed.

Crunching the numbers

Of note is that Singapore-based economic studies team UOB Global Economics & Markets Research is one of three research institutions that correctly called Bank Negara’s latest OPR hike, out of 19 analysts surveyed.

Its economists Julia Goh and Loke Siew Ting at the same time predict that this could be the final increase in the OPR for 2023.

Goh and Loke, in a note analysing the central bank’s movements on Wednesday morning, are also placing their headline inflation estimate for Malaysia at 2.8%, with an upside risk of between 0.2% and 1% over the next 12 months.

This will bring it in line with Bank Negara’s range approximate of between 2.8% and 3.8%.

Mulling over the possibility that the latest move could be “preemptive” against inflation, they explain: “Some domestic policies relating to subsidies and prices are expected to be rationalised in the second half of 2023 (2H23), starting from July at the earliest.

“They include electricity tariffs for domestic users, the price of chicken, eggs and cooking oil, as well as subsidies for diesel, in addition to the minimum wage hike to RM1,500 for companies that employ less than five employees.

“These changes will post more upside pressure for consumer price inflation, living costs and business operating costs in 2H23 should they materialise.

“This, alongside uncertainty surrounding the six state elections, could make it more challenging to raise rates further in 2H23.”

Goh and Loke reckon that a further partial removal of electricity subsidies could contribute an additional 0.2% to their 2.8% baseline headline inflation estimate, while a gradual increase in subsidised petrol prices, the weak exchange rate of the ringgit against other currencies and a rise in the crude oil price would bring about respective additions of 0.4%, 0.3% and 0.1% to that base approximation.

No systemic risks

Although recent developments in the US banking sector have raised valid concerns – the latest being the collapse of First Republic Bank following the earlier demise of Silicon Valley Bank – the UOB duo are not anticipating any systemic risks to the US financial system, and hence believe the Federal Reserve (Fed) will maintain its focus on battling inflation.

“As such, we maintain our view that the OPR has reached its peak at 3%, which is the pre-lockdown level, in line with the move by other regional central banks to end their rate hike cycle this quarter.

“There are less compelling reasons justifying a need for a further rate hike or a rate cut by Bank Negara going into 2H23, unless the global and domestic conditions take a swift turn.

“Hence, we project the OPR to stay on hold at 3% for the rest of the year,” say Goh and Loke.

The larger economic outlook

Looking at the broader picture beyond numbers and figures, Centre for Market Education chief executive Carmelo Ferlito tells StarBizWeek that the increase in the OPR is executed to withdraw money from the local economic system, which like those of many other countries, has experienced an “excess of money creation and therefore inflation”.

This is in addition to the well understood idea that a higher interest rate would encourage savings, and as such, dampen demand, theoretically leading to a drop in the prices of goods and services.

“While there have been countless debates about how this latest OPR increase will tighten the cost of living, make large segments of society poorer, or elevate the cost of doing business, we must recognise that this OPR hike is necessary, albeit a slightly painful price we have to pay,” he says.

He explains that increasing the supply of money – a commonly used monetary policy tool – as well as engaging in other expansive fiscal and monetary policies are a direct consequence of lockdowns that many countries had participated in over the past three years.

Describing the OPR increase as medicine that is to help the recovery from a disease, Ferlito says such moves are not sufficient in themselves, but necessary all the same in the fight against inflation.

He goes on to comment that the effects of the rate increase will not depend on the move itself per se, but rather on how it is being interpreted by economic agents such as the government itself, corporations, households and individuals, as well as enterprises and their subsequent response – in short a subjective link to an objective fact.

He points out: “If these economic agents see this move as a necessity to put a handle on inflation, it could maintain a generally optimistic attitude and economic activity would not be affected much.

“But if they interpret it as depressing and that it would cause the economy to go into a downturn, then it probably would.”

Monetary phenomenon

With the Fed also having raised its fund rate by the same degree as Bank Negara at its Federal Open Market Committee or FOMC meet this week, ostensibly also to stay guarded in its fight against rising costs, Ferlito says inflation – being a monetary phenomenon – cannot be tamed by merely adjusting interest rates.

Instead, he reiterates the necessity of a serious programme to reduce government spending, plus the reminder that inflation is easily created, but like a disease, not as easily removed.

“There is no overnight cure or magic wand for resolving this.

“It is a combination of sound fiscal or monetary policies, and one effective way would be the reintroduction of balanced budgets with no more deficits,” he says.

More crucially, he says effective communication between monetary policy decision-makers – such as central banks – and other economic agents is essential to ensure a healthy interpretation of moves such as OPR adjustments.

However, as to the question of whether Bank Negara would fine-tune the OPR with further moves this year, Ferlito offers an alternative opinion to UOB’s Goh and Loke, instead projecting that the country may not have seen the end of rate adjustments in 2023.

While agreeing with the generally held viewpoint among economists that the removal of government interference exercises such as price ceilings and subsidies benefit the country over the long term despite the inevitable teething pains, he opines that Malaysians are too used to such government assistance.

Moreover, he cautions that if such interventions are removed, the initial results would be more inflation, at least on official statistics, before adding that Malaysia’s consumer price index data has been moderated by price controls and subsidies.

Impact on markets

Chief executive of fund management firm Tradeview Capital, Ng Zhu Hann, thinks that Bank Negara’s surprise move on Wednesday has been premised on the confidence that Malaysia has little risk of entering a recession and that its gross domestic product (GDP) growth will remain resilient compared to regional markets.

On the other hand, he comments that Malaysia’s equity market has been under-performing global markets, and although there was a strong rebound towards the end of 2022 and early 2023 following the resolution of the political uncertainty with the formation of the unity government, the momentum did not continue entering April and May.

Ng says: “However, in terms of the fundamentals and earnings performance of our listed companies, I believe there is definitely upside compared to downside.”

After maintaining the OPR in January and March, Ng posits that the central bank likely determined that it is safe to adopt the proactive measure of hiking rates in 1H23, as inflation data moderates, coupled with strong signals of underlying economic strength.

Year-to-date, he says the country has seen positive foreign fund inflows into the bond market, despite a net outflow from equity markets.

Tightening quantum

Casting a look at international markets, Ng believes that global indices have largely factored in the latest rate hike – the tenth consecutively – by the Fed, as the tightening quantum has gone on for the past two years.

He attributes the lacklustre performance of global equity markets for all of 2022 to tightening monetary policies worldwide, which he says also impacted bonds, as the price of bonds would decline in a high-rate environment, causing yields to spike and bondholders to sit on unrealised losses.

“With risk-free rates rising to a very attractive level, there is little incentive to look for higher risk investments to justify returns. This would naturally cause a pullback in the capital markets as a whole.

“The biggest concern has always been the hawkish tone that was adopted by the Fed, whereby it is going to hike rates at all cost to bring down inflation back to the 2% level.

“However, following the moderation of the CPI data and inflationary pressure, including the regional banks crisis, the Fed has taken a step back to assess the situation,” he observes.

Ergo, seeing the continued normalising and slowing down of the rate hike quantums in 2023 and 2024, Ng says investors are expected to see less volatility in both global equity and bond markets this year compared to 2022.

He adds that the forward guidance is that next year may even see a potential rate cut again by the Fed if inflationary data becomes more favourable.

He says inflation has embarked on a healthy moderating trend in 2023, underpinned by retreating commodity prices, plunging freight rates and the cessation of supply disruptions, which contribute to relieving upwards inflationary pressures.

Ng remarks that one other factor that would further drive down prices across the board and normalise things to pre-lockdown levels is the possible resolution of the Ukraine-Russia conflict this year.

“This would definitely help with pausing rate hikes altogether and bring forth a case to provide liquidity to the market for recovery and growth.

“In Malaysia’s case, undoubtedly inflation has been rather well controlled – with the exception of food prices – because of the price control and subsidy mechanisms put in place by the government,” he says.

On a separate note, economists at Maybank Investment Bank Research (Maybank IB), like UOB’s Goh and Loke, forecast Bank Negara to keep the OPR at the present level.

Fluid policies

This is especially amid “fluid” policies on price subsidies and controls, which are exemplified by the implementation of targeted electricity subsidies at the start of this year; indication from the retabling of Budget 2023 of blanket fuel subsidies staying for the time being; and the plan to float chicken and egg prices in July.

Maybank IB says while high-frequency economic indicators such as its monthly GDP tracker, manufacturing purchasing managers’ index and external trade data signal moderating GDP growth, wages and salaries growth have remained elevated at levels consistent with an OPR of 3% to 3.25% in the past.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.