THE recently released property market data for the first half of 2022 (1H22) by the National Property Information Centre (Napic) showed that the Malaysian property market has found a firmer footing over the review period.

On a half-yearly basis, while transaction volume and value surged to a new record high of 188,002 units worth RM84.4bil, what was most revealing is that the overhang market trend has finally eased, while future and planned supply was reduced.

For the past four years, this column has been calling for stricter measures to control the market’s oversupply situation and for property developers to be more mindful of the market’s overhang status.

The data for the 1H22 shows that finally, some sanity has set in.

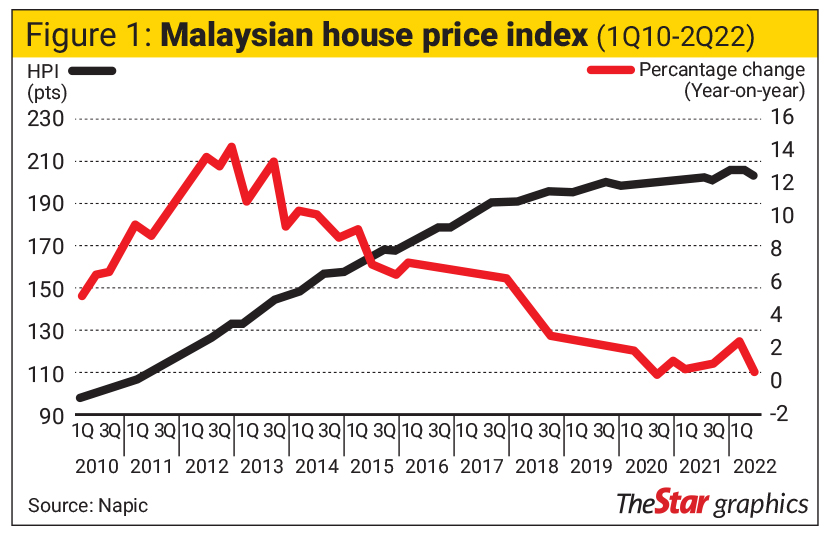

Having said that, as far as prices are concerned, the Malaysian House Price Index (HPI), as seen in Figure 1, continues to show a declining trend with the growth in the 1H22, slowing down to just 0.5% year-on-year (y-o-y), dragged by a 2.5% y-o-y drop in Penang HPI, and in terms of segment, detached homes and high-rises continue to dictate the downtrend with a 2.3% and 0.5% y-o-y drop respectively.

An improved picture

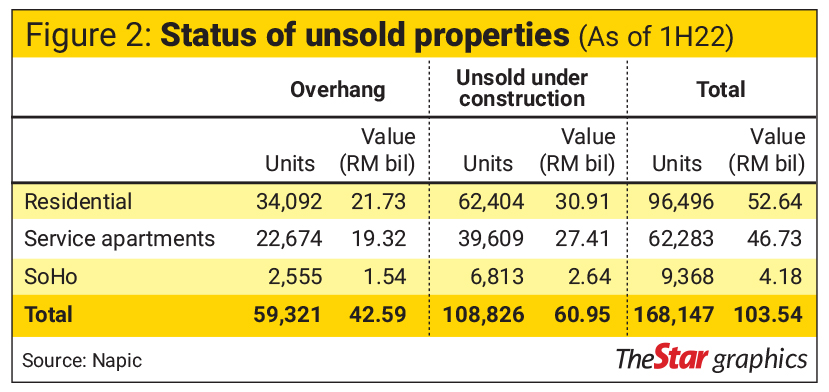

For property overhang, this column aggregates the supply in the residential segment and takes the data from both service apartments and the SoHo sub-segment to gauge the market’s overall residential overhang status.

After all, it is the combination of the three that is the real market supply in the residential market segment as shown in Figure 2.

In total, the residential overhang eased to 59,321 units valued at RM42.59bil.

Although compared with a year ago, the number of overhang units and value increased by 3.8% and 2.5% respectively, the overhang situation for the residential segment improved as both the number of units and value dropped by 6.5% and 4.4% respectively compared with six months ago.

Nevertheless, the overhang situation within the high-rise segment (which includes residential high rise, commercial service apartments, and SoHo units) remains elevated.

For the 1H22 period, Napic data showed that the overhang data is now at a new record high of 45,502 units against 44,800 units as at end of 2021.

Only in terms of value, the 1H22 figure is relatively flat at RM33.22bil against RM33.32bil six months ago.

Overall, this translates to 76.7% of the overall market overhang in volume and almost 78% of the total value.

The overhang situation within the high-rise segment has indeed increased as more than three out of four unsold properties are high-rise units.

A steep drop

Figure 2 also shows the property market’s unsold units that are under construction.

From here, one would note that the 1H22 data showed a total of 108,826 units remained unsold valued at RM60.95bil, down by 12.5% and 9.6% compared with a year ago, and lower by 9.7% and 6.4% when measured against the market’s position six months ago.

With the lower overhang and those under construction, overall, the market saw total unsold properties down to 168,147 units worth some RM103.54bil.

Compared to a year ago, when the figure was 181,460 units worth RM108.93bil, the data for 1H22 saw a drop of 7.3% in volume and 4.9% in value respectively.

When compared with the 183.918 units worth RM109.69bil as at end of 2021, the 1H22 data showed a reduction of 6.4% in volume and 8.6% in value respectively.

For the residential segment by state, the key overhang is located in Kuala Lumpur and the states of Selangor, Johor, and Penang as they account for 59% of total overhang units worth some RM16.2bil, which translates to 74.5% of the total overhang value in the residential segment.

In terms of price points, properties marketed at above RM500,000 account for 43.4% of the market’s overhang.

For service apartments, Johor, Selangor, and Kuala Lumpur are key geographical areas with the most overhang with a total of 96.8% of the segment’s overhang in terms of units and 97.5% in terms of value.

Johor alone accounts for 68% of the segment’s total number of units and nearly 69% of the segment’s total value at RM13.34bil.

Interestingly, in terms of the number of units, 89% of service apartment overhang in Malaysia are priced at RM500,000 and above, valued at RM18.36bil, and they represent 95% of the total service apartment overhang valued at RM19.32bil. Seeing some light

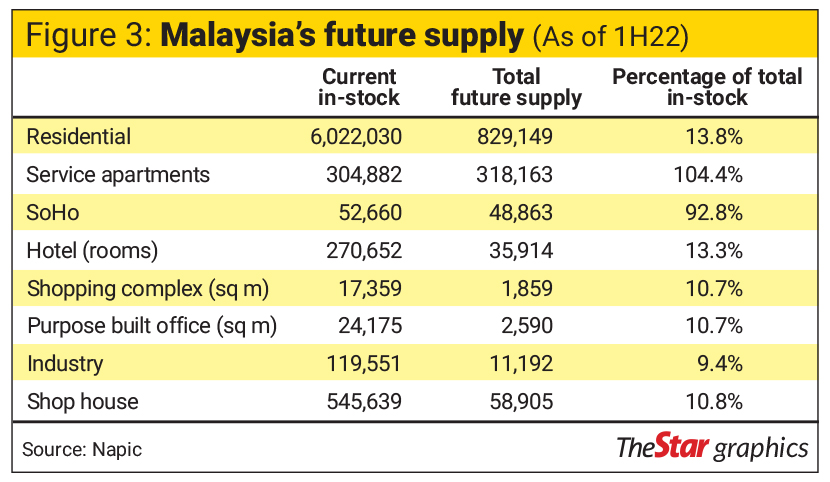

As this column has repeatedly highlighted in the past that Malaysia has a serious overhang issue, we are now finally seeing some light at the end of the tunnel as the market has now seen a drop in future supply.

For easy reference, the data in Figure 3 for future supply includes starts, incoming supply, planned supply, and planned new supply.

Overall, other than a 34% jump in purpose-built office space to 2.59mil square metres, all other segments are seeing a downtrend in future supply with a reduction in the total number of units by between 8.1% for the industrial segment to as much as 26.2% in future hotel room supplies.

The residential, service apartments and the SoHo segment saw a reduction of 16.3% in the total number of units to 1.196mil units from 1.430mil units six months ago.

As a percentage of total in-stock, the future supply is lower by between 0.8 percentage points (pps) for the industrial segment to 21.1 pps for the residential segment. A word of caution though. Despite the reduction in future supplies, the incoming supply for both the service apartment segment and SoHo remains significant at 104.4% and 92.8% respectively.

Malaysian property market remains challenging

Despite the positives, the property market remains challenging as we are still saddled with a high overhang as well as incoming supply. While the positives are there based on the 1H22 data, it is not time to pop the champagne just yet as it will still take a while (three to five years) for a more positive trend to emerge.

Overall, the Malaysian property market is still up against a massive over-supply situation and prices too are not expected to improve much, as evident from the flattish growth or worse, negative, in the Malaysian HPI.

Given the higher borrowing cost with an increase in the overnight policy rate, homebuyers are expected to remain cautious.

Pankaj C Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.