Years of operational inefficiencies take a toll on giant planter

FGV Holdings Bhd chairman Datuk Wira Azhar Abdul Hamid faces a monumental task ahead to steer the loss-making diversified plantation group out of the woods.

chairman Datuk Wira Azhar Abdul Hamid faces a monumental task ahead to steer the loss-making diversified plantation group out of the woods.

Coming into the end of his first-year at the helm of FGV, Azhar hopes that he will be able to clean up the “unproductive and inefficient” operational issues bogging down the group within the next two years.

Not making it easy for Azhar is the fact that FGV, which is the world’s largest crude palm oil (CPO) producer is an important political cog in the government’s machinery.

Since its listing in 2012, the journey to transform FGV into a financially-viable and successful outfit has hit several speed bumps.

The track record of FGV in the past five years has been dissappointing and marred by weak leadership, breach of authorities limit, unwise investment decisions and failure to boost the efficiency of its existing core plantation operations, Azhar points out.

In the latest developments, several dubious investment transactions under the past management are subject to forensic audits and internal investigations.

This could lead to several serving and former top management officials being charged and possibly put to trial in the near future.

FGV in recent years has also been badly criticised for its massive acquisition-spree in over-priced and non-value-accretive investments, after gaining RM4bil in proceeds from its IPO exercise.

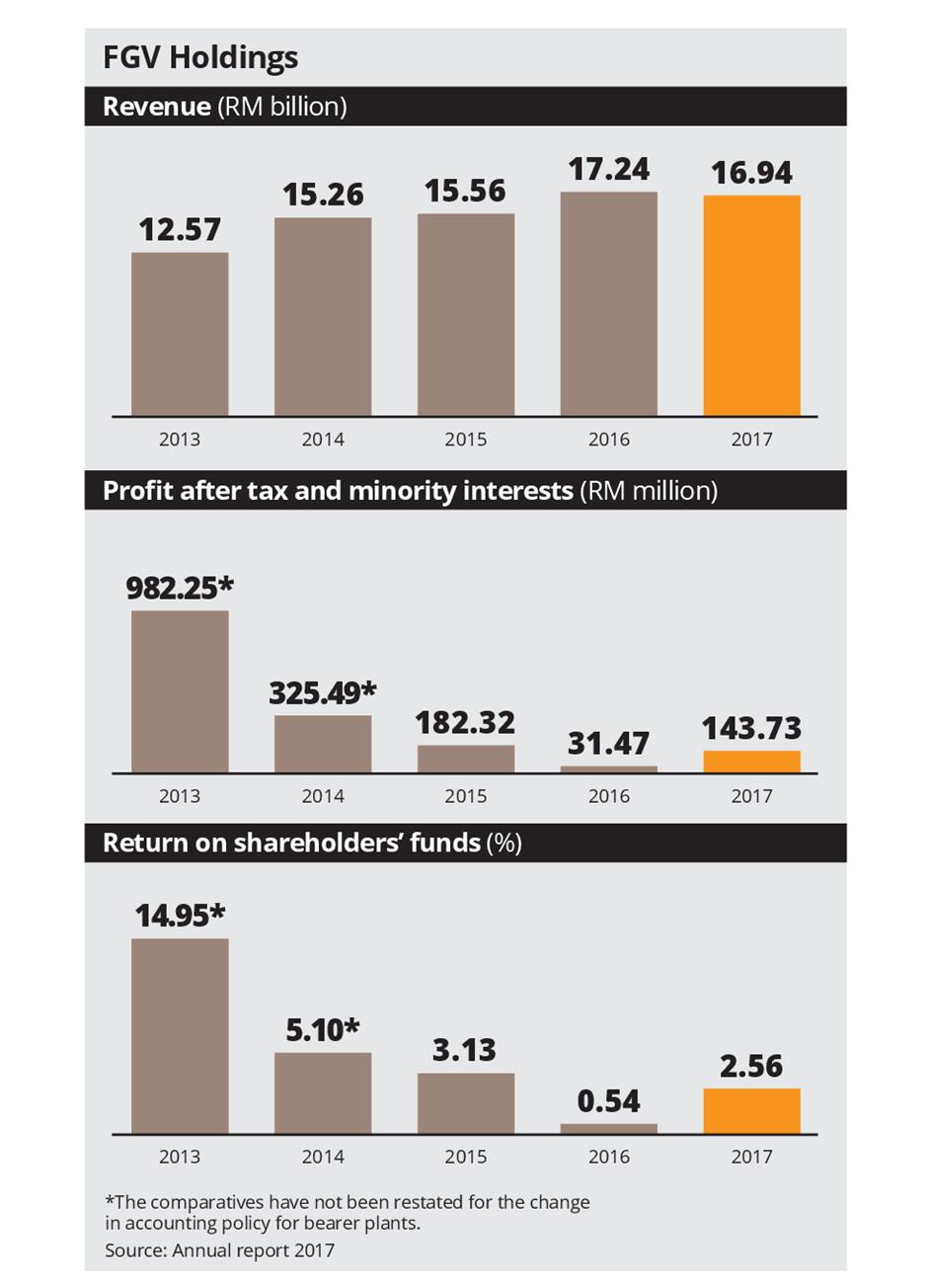

The group is now saddled with debt of about RM5.48bil of which the long term liabilities are RM2.22bil while cash in the kitty is RM1.5bil. It posted a net loss of RM23.23mil in the second quarter ended June 30 with a lower revenue of RM3.44bil.

Azhar tells StarBizWeek in a recent interview that FGV has been plagued with too many legacy issues.

It can even be made into a Harvard Business School case study, he adds.

“The unproductive and inefficiency issues are like a shackle on us, with FGV not having enough funds for investments amid the low productivity in the estates and low profit environment.

“But we have been busy putting things right and are now almost reaching the tail-end,” he points out.

Next year, Azhar is confident that the group’s upstream operation has the potential to improve in terms of its fresh fruit bunch (FFB) yields and is likely to achieve its target of 20 tonnes per hectare per year.

The targetted FFB yield is 17 tonnes per ha per year for 2018, compared with 15.4 tonnes in 2017. FGV will also continue with its aggressive replanting of 15,000 hectares per year, which soaks up about RM300mil per year.

Azhar admits that the yield performance at the group’s estates has not been good in the past years, as “serious replanting was only undertaken beginning 2016”.

“We actually inherited old plantations (from Felda), which are badly in need of replanting. This is among the issues which affected our performance and has been holding us back,” Azhar explains.

FGV’s estates are largely the 355,864ha of plantations that were under Felda prior to the listing in 2012.

The plantations were transferred to FGV under a land lease agreement (LLA) to pave the way for FGV’s listing exercise. However more than 40% of the plantations the FGV received under the LLA were more than 25 years old.

According to Azhar the management repeatedly has not addressed workers’ housing problems and overcome the unprecedented labour shortage situation.

“When I stepped in (last year), FGV was facing a shortage of 10,000 workers. Just imagine FGV stands to lose some RM2mil per day from the shortage of harvesters in the estates,” he adds.

This is also another main issue why FGV has not been performing up to mark compared with its peers in the industry.

Azhar says, “We will no longer compromise on this matter and are already putting the right discipline into actions such as the collection of loose fruits, the right harvesting cycle and an on-time fertiliser programme in our estates.”

Also, at fault is the past leadership in the investment decisions. Azhar points out that “the only good deal was the RM2.2bil acquisition of Pontian United Plantations Bhd (PUP), while most of the the past acquisitions are sub-quality and non-value-accretive investments that only depleted FGV’s cash reserves.”

In January 2018, the FGV board officially appointed forensic investigators to look into six transactions and/or investment decisions, of which four have been completed and the `findings are adverse’. The investigations which have been completed include the acquisition of Asia Plantations Ltd (APL), the investment in FGV Cambridge Nanosystems Ltd and the acquisition of the Troika condominiums near the Kuala Lumpur Twin Towers area.

In the case of APL, FGV acquired the London-listed company for RM1.1bil including its debts.

“We can hardly use half of the hectarage for planting oil palm. We also found out that 700ha there do not even belong to the seller, and now, we are tangled with the Native Customary Rights land issue,” says Azhar.

APL owns 24,622ha of oil palm plantations through its five wholly owned estates in Sarawak.

During former chairman Tan Sri Isa Samad and former group president and CEO Datuk Emir Mavani leadership in FGV from January 2013 until March 2016, the plantation company went on an acquisition binge, completing seven transactions worth RM4bil. Among the estates purchased were PUP APL and Golden Land Bhd.

Given the group’s poor performance, the FGV board is undertaking internal investigations into six matters relating to its operations.

They broadly covers poor purchasing and trading practices that have led to bad debts of RM100mil, the direct awards of procurement contracts and financial losses exceeding RM170mil from the shortage of workers between May 2016 and April 2018.

“All these boil down to the current leadership within the FGV Group,” quips Azhar.

The board is also reviewing all the findings of its forensic audits and internal investigations, he says, adding that it has sought legal advice on the possible legal recourse.

He expects that the next course of action against the relevant individuals will likely be announced in the coming months.

Azhar is optimistic about the group’s ongoing critical turnaround plan despite the challenging tasks ahead.

“We will need to generate profits for the group and start to build our reserves again,” he adds.

“Every year, FGV will need to fork out RM300mil-RM400mil for replanting and also commit to pay Felda a sum of RM250mil annually and 15% of its annual profit as part of the LLA, among others. Felda currently owns about 34% in FGV.

Meanwhile, CGS-CIMB in its recent FGV report “No pain, no gain” is positive on the steps taken by the FGV board to identify and improve on the company’s existing practices.

However, this is offset by concerns that the improvements will take time and this could lead to write-offs in the near term.

The call by CGS-CIMB essentially sums up the task ahead for Azhar.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.