WHEN a top banking official recently suggested that the central bank expand single customer limits of banks’ financing of the country’s energy transition, it highlighted a growing funding gap.

As Malaysia’s solar projects increase in scale, those who get awards to construct them are finding it increasingly difficult to get access to their hitherto most suitable source – the domestic banking sector.

This stems largely from the Single Counterparty Exposure Limit (SCEL), which caps how much banks can lend to a single borrower or related group.

The country’s booming large-scale solar (LSS) projects, despite being awarded to several companies, all have one common offtaker – Tenaga Nasional Bhd (TNB). (See side story)

(TNB). (See side story)

Going by SCEL rules, banks cannot have more than 25% of eligible capital exposed to any single counterparty or connected counterparties.

TNB and Petroliam Nasional Bhd or PETRONAS are exceptions, with an additional 10% allowance.

While banks still have headroom, this buffer is narrowing as more large-scale renewable energy (RE) projects enter the pipeline.

LSS6 tenders are expected to open soon and will include battery storage requirements.

Adding to the challenge are weakening “project economics”. Newer projects are not only larger in scale, but are also awarded at relatively low tariffs.

This is further exacerbated by rising construction costs, driven by higher solar panel and fuel prices.

The rise in diesel price, for example, is having a huge impact on the cost of earthworks, which is the early part of building out a solar farm.

One obvious alternative to bank financing is the bond market.

But bond issuances can be more costly and the issuer needs to get a rating, which means not all can make it, especially smaller newbies.

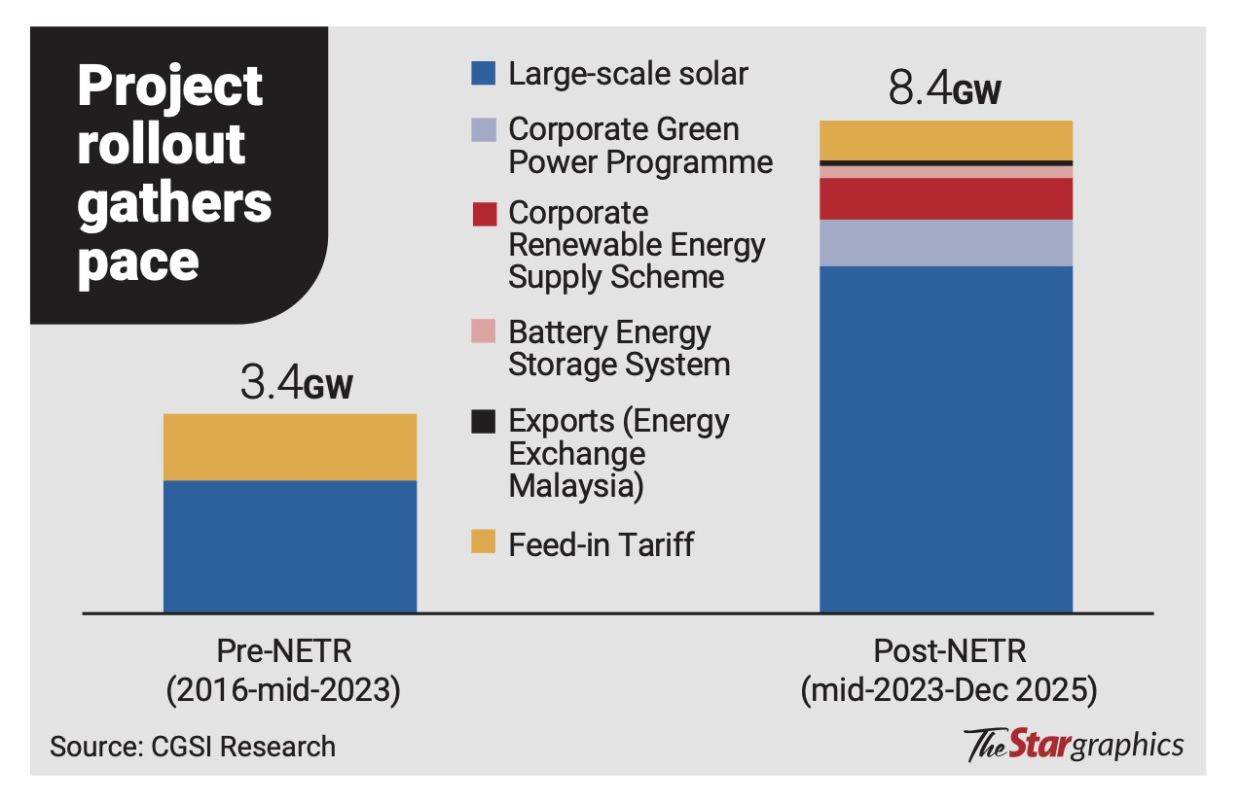

Malaysia is now in its fifth iteration of LSS development, with two tranches – LSS5 and the supplementary LSS5+ – awarded to build larger utility-scale solar plants, with projects typically around 100MW in size, with some projects larger.

Taken together, LSS5 and LSS5+ represent roughly 4GW of awarded capacity, marking one of the largest utility-scale solar build-outs in Malaysia.

This translates into materially higher capital requirements, with project costs now running into the hundreds of millions of ringgit per project.

Tariffs for LSS5 and LSS5+ projects are understood to range between 13.75 sen and 18 sen per kWh, compared with 17.68 sen to 24.81 sen per kWh under LSS4, reflecting continued downward pressure from competitive bidding.

Citaglobal Bhd head of new energy Datuk Chairil Nazri Ahmad says it is too early to fully gauge the impact of the ongoing geopolitical tensions, particularly on pricing, logistics and supply chains.

Citaglobal, together with the United Arab Emirates’ Masdar, was shortlisted by the Energy Commission (EC) to develop a 200MW floating solar plant under LSS5+ at the Chereh Dam in Kuantan, Pahang.

Drawing on the project’s experience, Chairil says several materials used in floating solar systems are petrochemical-based, leaving them directly exposed to availability of materials as well as upstream price volatility.

“Given the material and logistical uncertainties stemming from the war in the Middle East, suppliers are finding it harder to commit to firm pricing and delivery schedules,” Chairil tells StarBiz 7.

He contrasted today’s open-ended geopolitical pressures with the LSS4 round, which, while disrupted by the Covid pandemic, unfolded against a more contained and ultimately resolvable shock.

“Under LSS4, the impact was more measurable and could be assessed progressively, which allowed the EC to respond with calibrated measures, including a four-year extension of power purchase agreement (PPA) tenures.”

Drawing on industry feedback, Chairil says the current pressures could be addressed through a combination of measures – among them tariff recalibration, an extension of PPA tenures, extension to commercial operation date and a waiver of the sales and service tax on construction-related services, which was introduced only after the LSS5 and LSS5+ bids had been submitted.

As with LSS4, where tariff adjustments were ultimately not adopted, any such move may prove equally challenging for LSS5 and LSS5+, given that the awards were secured through a competitive bidding process.

As for solar panel prices, they have rebounded from their 2024 lows and are now stabilising, while inverter costs remain largely flat to slightly higher.

However, the main uncertainty lies in logistics amid ongoing geopolitical tensions.

One industry player estimates that net equipment costs will rise by about 5% to 15%, depending on procurement timing and companies’ sourcing strategies.

This, in turn, suggests that internal rates of return for LSS5 and LSS5+ projects could compress to 5% to 6%, compared with earlier expectations of 7% to 8% – levels which are still bankable but expected to keep domestic banks at the centre of financing, as they typically offer lower funding costs, players say.

Samaiden Group Bhd group managing director Datuk Chow Pui Hee tells StarBiz 7 that access to finance is key to achieving energy goals.

“Low-cost long-term financing is important, given the capital-intensive nature of RE technologies where most costs are front-loaded. If banks are unable to extend exposure due to regulatory limits, project rollout will slow regardless of underlying demand.”

Chow, whose group has participated across the LSS programme since its early iterations as an engineering, procurement, construction and commissioning contractor and secured projects as a developer under the latest LSS5 and LSS5+ rounds, says the financing landscape has evolved significantly from the initial transition away from the feed-in tariff (FiT) mechanism.

“At the time, banks were accustomed to FiT projects of around 1MW to 5MW. Early LSS projects were larger (relative to FiT), with some already reaching 20MW and costing about RM100mil,” Chow says, adding that the sharp drop in tariffs from FiT levels added to initial caution among lenders, and approvals took longer.

During this transition period, some developers tapped the bond market under early fast-track solar initiatives and LSS1 projects backed by established companies, issuing green and sustainability-linked structures

Subsequent LSS rounds saw bank financing become the dominant funding channel as lenders grew more comfortable with utility-scale solar and standardised processes.

However, as newer projects grow in size and cost, discussions are back on alternative funding structures, including sukuk, as larger projects are better able to justify capital market issuance.

As for Samaiden’s LSS5 project to develop a 99.99MW solar farm in Pasir Mas, Kelantan, Chow says sukuk financing was considered but, due to structural issues, the group proceeded with bank financing instead.

“We may be revisiting sukuk financing for our 99.99MW solar plant in Segamat, Johor, under LSS5+ (which it partnered with JBB Builders (M) Sdn Bhd), but potentially combining bank facilities with sukuk for capital expenditure.”

One other consideration is gearing. Heavy reliance on bank financing increases group borrowings, which in turn affects gearing ratios and credit profiles.

This is something which also needs to be managed by players, Chow adds.

She expects financing structures to become more mixed, but says execution would depend on cost, timing and each company’s balance sheet strategy.

Sharing on recent LSS5 funding, RAM Rating’s co-head of Infrastructure and Utilities Ratings Chong Van Nee notes only a limited number of projects have come to the bond market.

“That suggests banks are still quite willing to finance these projects. They are now offering longer tenures, sometimes beyond 15 years,” Chong says. .

Private equity, however, is generally considered less suitable for long-gestation infrastructure assets due to its shorter investment horizons.

“Ultimately, financing outcomes hinge on project economics. If there is a mismatch between tariffs and costs, it becomes difficult to secure funding from either banks or the capital markets.”

According to Chong, larger issuances tend to attract stronger investor demand, as deal size is key to market liquidity, while smaller deals may face weaker demand or pricing pressure.

“Where a sponsor lacks a strong track record or the project structure is less robust, attracting investors can be challenging.

“However, newer players can still tap the market if they bring in experienced contractors,” she adds.

Banks stay active in RE financing

CIMB Group wholesale banking chief executive officer Chu Kok Wei says the group has active exposure to RE within its financing portfolio and “retains sufficient capacity to grow this further” given ongoing demand and supportive market fundamentals.

For utility-scale projects, Chu says the challenge is less about whether capital is available and more about whether the project is consistently “deliverable” at scale given cost volatility, varying contractor delivery capabilities, performance and completion risk.

“At the same time, Malaysia’s electricity needs are rising, particularly with faster data centre rollouts, which means the system will need more RE and, over time, energy storage solutions, and that naturally increases overall funding requirements.

“What would help unlock faster growth is greater standardisation in contracting and risk allocation, alongside policy refinements that expand effective balance-sheet capacity so intermediaries and end financier can support a larger pipeline without running into concentration constraints,” CIMB’s Chu adds.

Malayan Banking Bhd group chief sustainability officer Datuk Shahril Azuar Jimin says the bank has been using structures such as project finance, sustainability-linked loans, green financing, as well as Islamic instruments including green and sustainability sukuk to finance a broad range of RE assets including hydroelectric and utility-scale solar projects.

Financing within prudential limits

Ernst & Young Consulting Sdn Bhd Malaysia financial services consulting leader and partner Ling Kay Yeow says Malaysia’s large exposure framework is broadly aligned with the Basel Committee on Banking Supervision large exposures standard, which came into full effect globally in 2019.

He notes that where prudential limits constrain single-counterparty lending, the solution is “not to relax the standards, but to build financing structures around them”.

“Jurisdictions facing the same tension between regulatory concentration limits and large-scale infrastructure financing need have structures that distribute risk, recycle capital, and bring in non-bank sources of funding.

“These approaches are particularly relevant for capital-intensive sectors where funding needs are concentrated among a small number of large counterparties – precisely the dynamic playing out with energy providers and the RE pipeline in Malaysia.”

Ling notes that one key approach has been the scaling of sustainable debt markets, including green bonds and sustainability-linked loans.

These instruments enable banks to originate and distribute exposures to a wider investor base, thereby reducing concentration risk while continuing to support large projects.

Ling cites the Asean Catalytic Green Finance Facility (ACGF), led by the Asian Development Bank, as an example of blended finance structures that combine concessional, multilateral and private capital to improve project bankability and crowd in private investment.

“For Malaysia specifically, the most immediately actionable pathways are deepening the domestic green bond market, expanding Multilateral Development Banks co-financing partnerships through platforms such as the ACGF, and developing infrastructure investment trust (InvIT)-style structures for operating solar assets,” he adds.

InvITs are pooled investment vehicles like a mutual fund that allow infrastructure assets owners to monetise their assets by pooling multiple assets under a single entity via a trust structure.

Investors can invest in these assets without having to directly own them, in return for distributable cash flow of the InvIT.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.