WHILE most people assume the economic consequences from the military conflict in Iran will be much less severe, and believe that the global economy could withstand the conflict, we must not be too complacent about the economic risks this war creates.

The International Monetary Fund has cautioned that the escalating conflict in the Middle East could undermine global economic stability if it becomes prolonged, flagging risks to energy markets, inflation trends and investor sentiment.

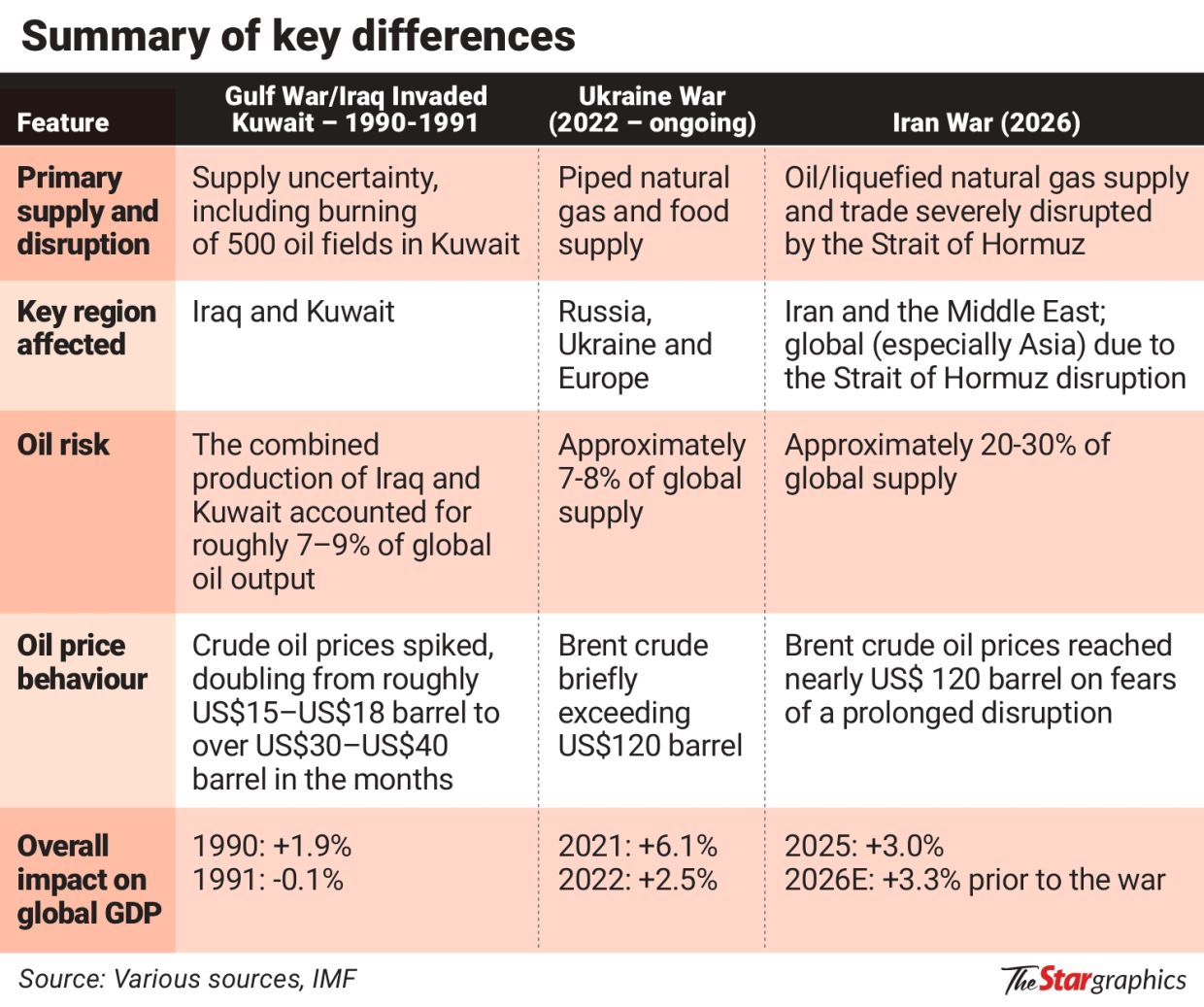

The impact of war and oil shocks on the global economy is largely determined by the degree of oil price increases (permanent or temporary) and duration of supply disruptions.

Recent episodes of conflicts in the Middle East showed that a short-lived, low-intensity shock may inflict moderate economic friction, while a prolonged, high-intensity conflict could trigger severe inflationary shock, especially for countries that are high net oil and gas (O&G) importers, thus increasing business costs, reducing spending and business activities, dampening economic growth, and, in a worst-case scenario, leading to a global recession.

While a 60% to 70% decline in the oil intensity of gross domestic product since the 1970s, thanks to a structural shift towards services and energy efficiency, has lessened the blow, sustained soaring oil prices still create headwinds for global economic growth, especially for the Europe and Asia, which are net energy importers. The United States is a net oil exporter.

Sustained, large increases in O&G prices place net energy-importing Asian countries in a highly vulnerable position (concentration risk exposure) to the energy shock, triggering stagflationary pressures, widening trade deficits, and posing severe fiscal strain.

Countries that sourced their O&G from the Middle East include Japan (over 90% of their crude oil imports), the Philippines (over 90%), South Korea (about 70%), Thailand (about 60%), China (more than 50%) and India (60% of its liquified natural gas or LNG).

Malaysia is a net crude oil importer since 2022, as well as a net exporter of LNG and petroleum products.

The key variables in transmitting an oil shock into a recession are the duration and magnitude of the price surge, central banks’ monetary policy response, and the pre-existing state of the economic cycle.

The world economy remains fundamentally weak. The Middle East conflicts come at the time when the global economy remains susceptible to the ongoing shift in tariff policy, slower productivity growth, persistent budget deficits and soaring government debt.

There are significant, synchronised risks arising from historically high stock market valuations, often described as “priced for perfection”, combined with mounting concerns in the rapidly expanding private credit market.

While massive investment in artificial intelligence (AI) brings significant productivity gains, it also carries risks of creating an economic bubble, which could trigger a major economic shock if it bursts.

Soaring oil prices and a sharp fall in stock markets fuel significant inflationary fears, cause wealth loss and reduce net disposable income.

If the energy shock sustains, firms could face margin pressure and production cuts, while consumers could bear the burden of higher inflation, including food prices.

Higher O&G prices will depress economic activity because they act like a tax on businesses and consumers, leaving less money to spend.

Significant, ongoing disruptions to critical global shipping route will increase production cost and reduce output, as well as cripple demand.

The Strait of Hormuz is experiencing a de facto, functional closure for much international commercial traffic due to escalating conflict.

Increasing safety risks, rising insurance premiums, and military posturing have severely disrupted the transit of about 30% of global seaborne oil trade and 20% of global LNG trade passing through the checkpoint.

While releasing 400 million barrels strategic petroleum reserves from 32 International Energy Agency members, which collectively hold around 1.2 billion barrels, can help bridge supply gaps for several weeks, it does little to resolve the shipping bottleneck.

As long as tanker traffic remains constrained, markets will continue to price a significant risk premium into oil prices.

The disruption has created chain reaction and domino effects affecting shipping, insurance, agriculture, automotive, and aviation sectors, among others.

Rising odds are neither stagflation nor recession will happen. Fundamentally, three variables matter: oil price shocks duration (persistent oil spikes); the US Federal Reserve’s (Fed) reaction; and the financial stress.

While a 2026 recession is not the definitive “base case”, a full-blown Iran war and severely escalating regional conflict with sustaining high oil prices beyond six to 12 months – reinforced by the financial stresses related to an extended sharp declines in stock prices, AI investment bust and private credit markets – increase the risk of a global recession or stagflation where slower economic growth is paired with higher inflation.

Some scenarios have warned of a “guaranteed” recession if key shipping routes are permanently closed and steep market valuations, driven by high expectations of investment return and earnings, face a severe share price correction as persistent large oil shocks significantly impact operating costs and reduce corporate profits.

Higher energy costs and supply chain constraints could also delay, restrict, or “stall” AI investment.

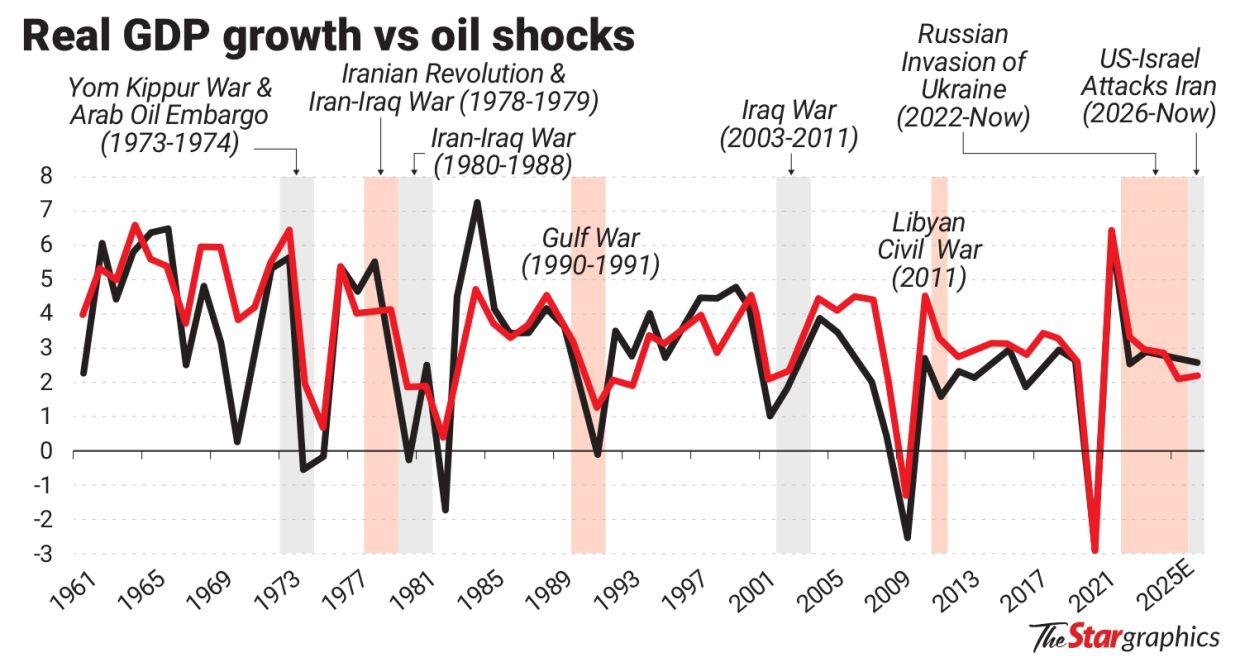

Four major oil price shocks since the 1970s were generally responsible for triggering or severely exacerbating global recessions.

These are the 1973 to 1974 Yom Kippur War and Arab oil embargo, the 1979 Iranian Revolution, the 1990 Gulf War, and the 2007 to 2008 oil price spike, coupled with an implosion of the US subprime crisis and the euro-zone debt crisis, which all preceded sharp economic downturns.

The 1970s oil shocks-driven recession were amplified by the Fed’s aggressive monetary tightening.

This time round, three factors potentially put the Fed in a bind.

One, higher O&G prices increase inflation risk, adding to a stubbornly inflation above the Fed’s 2% target, which is partly contributed by US President Donald Trump’s tariff policy.

Second, there is also risk of fuelling expectations of future inflation.

Third, weakening labour market conditions amid relatively resilient wage growth.

These three factors compel the Fed to navigate a delicate calibration of its monetary policy – either to keep interest rates on hold for longer, or even to weigh a rate cut if the risk of a sharp economic downturn outweighs transitory cost-driven inflation.

Higher fuel price acts as a tax on consumers and businesses, and could slow down consumption and spending.

Asian countries are responding to the energy shock to soften the blow on their domestic economy.

Some regional countries hold strategic petroleum reserves (SPR) to buffer against global supply disruptions: Japan (254 days), South Korea (208 days), China (about 200 days), India (about 74%), Thailand (61 days), the Philippines (60 days), Indonesia (20 days), and Vietnam (15 days).

Japan and South Korea are prioritising supply security through SPR releases. South Korean authorities are planning to introduce a cap on domestic fuel prices, calling for the expansion of the 100 trillion won (US$66.9bil) market stabilisation programme, and vowed to look for other energy sources.

China has temporarily suspended issuance of export permission certificates for refined oil products, focusing on ensuring domestic supply security.

The Malaysian government has announced austerity measures, including the cancellation of official Aidilfitri open houses.

It will also maintain RON95 at RM1.99 per litre, compared to unsubsidised price of RM3.27, reiterating that fuel supply is sufficient and guaranteed for at least two months (up to May 2026).

Thailand has suspended its exports of petroleum products, mandated an increase in oil traders’ reserve obligations from 1% to 3%, and boosted its oil reserves through imports from the United States and West Africa.

The government also approved urgent measures such as work-from-home policy, energy-saving measures in offices, and suspension of oversea trips, as part of efforts to cope with the energy crisis and restrain budget spending.

The Philippine government has ordered a temporary four-day work week for selected government offices to reduce electricity and fuel consumption by 10% to 20%, while reducing excise tax on petroleum products.

Meanwhile, Vietnam has proposed to reduce the tariffs on several petrol and oil products to zero.

Lee Heng Guie is the executive director of the Socio-Economic Research Centre. The views expressed here are the writer’s own.