A RECENT report citing an unnamed official reveals that the Employees Provident Fund (EPF) attracted a whopping RM13bil in voluntary contributions last year from over 1.2 million members.

That’s about 7.5% of the EPF’s more than 16 million members or 14% of its 8.7 million active contributors.

These include 400,000 members under the i-Saraan scheme, introduced in 2018 to help self-employed and gig workers save for retirement, where participants receive a 20% government incentive or up to RM500 per year on their contributions.

An economist tells StarBiz 7 that the RM13bil figure is “mind-boggling,” while another points out that the amount is just 1.06% of the EPF’s total RM1.22 trillion in investment assets.

The surge in voluntary contributions can be attributed to government support through i-Saraan since 2018 and the increase in the annual contribution limit from RM60,000 to RM100,000 in 2023.

While this trend signals growing awareness of retirement planning, it also raises concerns for banks, which may be losing a key source of low-cost funding.

Implications for banks

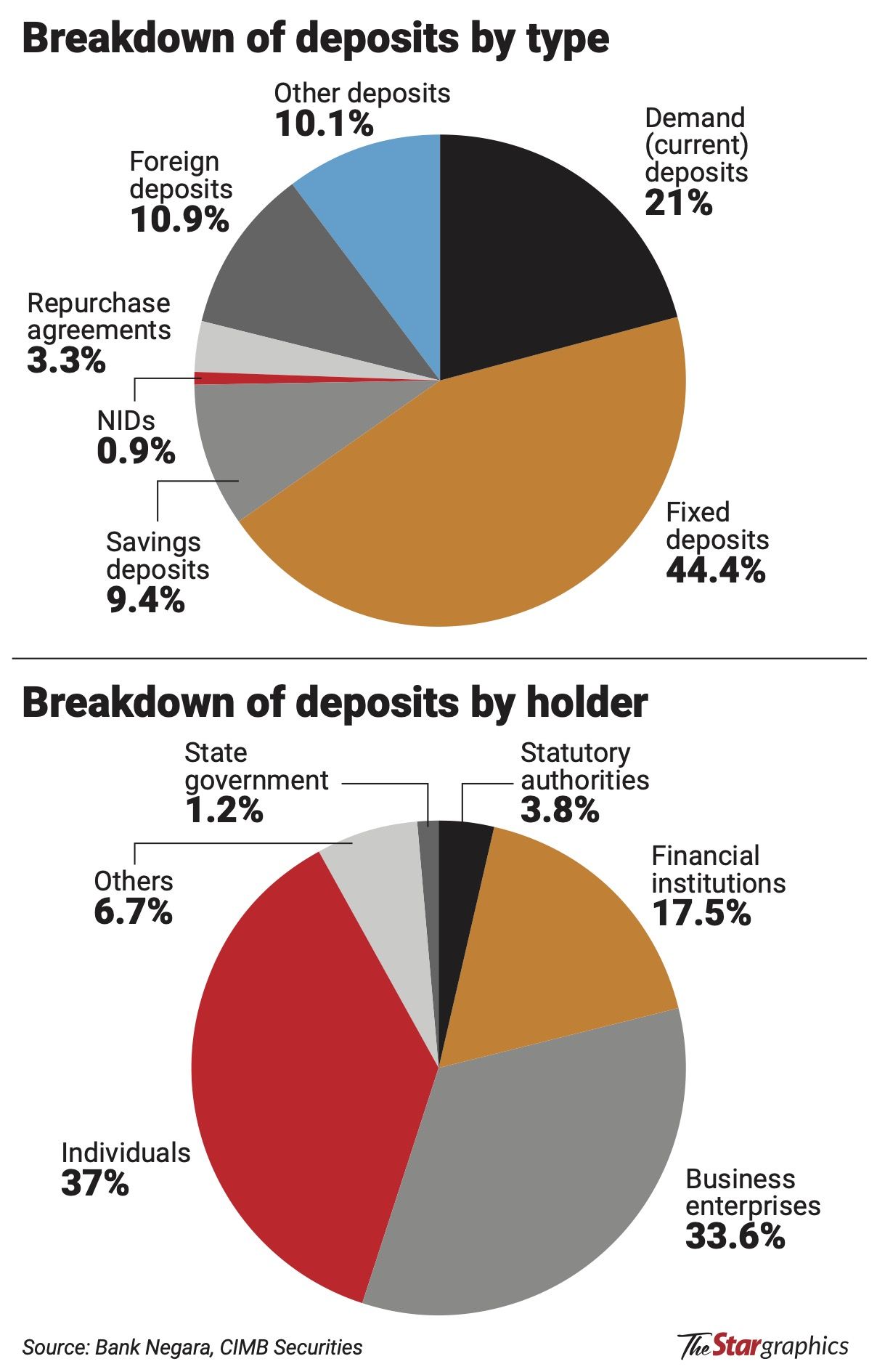

Banks typically rely on customer deposits as their primary funding source, as demand and savings deposits – especially from individuals – incur low or no interest costs and provide stable funds for lending at higher margins.

In contrast, alternative funding sources such as interbank loans, bonds and foreign borrowing carry higher costs due to market-driven interest rates.

With RM13bil flowing into the EPF – where members benefit from a consistent 5%-6% dividend yield – are banks at risk of losing a segment of their traditional deposit base?

Data from Bank Negara shows that while core deposits for the Malaysian banking system, which include demand, fixed and savings deposits, grew 27%, fixed deposits specifically declined by almost 10% to RM611.3bil in December 2024 from a peak of RM676.2bil in April 2014.

However, this decline was offset by demand deposits, which almost doubled to RM530bil over the past decade, while savings deposits grew by about 75% to RM238.5bil.

Total deposits, fortunately, grew by almost 60% to RM2.44 trillion, mainly driven by the faster growth of non-core deposits, which surged by 133%.

Economists believe the shift in deposit patterns could affect banks’ funding strategies.

“The returns on the EPF savings are much better than at banks, and with (EPF) Account 3 offering the same returns with immediate access, there should be an outflow from banks to the EPF in voluntary contributions,” says founder and director of Williams Business Consultancy Sdn Bhd, Geoffrey Williams.

Former investment banker Ian Yoong Kah Yin notes that the EPF’s dividend rates have consistently outperformed fixed deposits, making it a more attractive savings option.

“In 2023, the EPF paid a dividend of 5.5% and 5.4% for conventional and syariah savings, respectively, significantly higher than the 2.5% to 3.5% interest rates offered by banks for fixed deposits,” he says.

He expects the EPF to pay between 5.5% and 6% for 2024, further reinforcing the shift.

Banks have been adapting by focusing more on fee-based income rather than interest-based income. “Fee-based income is now preferred as it has a greater impact on improving return on equity (ROE), which is a key performance indicator for banks,” Yoong says.

Socio-Economic Research Centre executive director Lee Heng Guie describes the RM13bil in voluntary top-ups as a “mind-boggling number”, but sees it as part of a longer-term shift in savings behaviour.

“Those who withdrew during the pandemic now feel things are more stable and want to top up more,” he says.

“At the same time, the EPF continues to sustain a reasonable dividend rate.”

Still, Williams points out that the RM13bil represents just slightly over 1% of the EPF’s total fund.

“There has been a surge, but this is likely to stabilise as people get back on track to achieve their target retirement savings,” he adds.

Impact on EPF’s

investment strategy

Lee says that with more capital at its disposal, the EPF faces pressure to deploy funds effectively both locally and internationally to maintain strong dividend yields.

“The pool of investible funds will grow, so that also means pressure to invest the money, either locally or abroad, and give a reasonable dividend,” he says.

Yoong cautions that the surge in voluntary contributions could strain the EPF’s ability to maintain strong performance, especially when it is compelled to channel more of its investments locally.

“The majority of Malaysians are disillusioned by the stock market. That January 2025 was the worst performing first month for the past three decades is telling.”

Will the trend continue?

Economists largely agree that the trend of increasing voluntary contributions to the EPF is likely to continue. Lee points out that people are becoming more aware of the need to safeguard their retirement savings.

Asked whether voluntary contributions should be further incentivised, Lee says: “Yes, definitely. I hope that in the future, the RM100,000 limit can be increased.”

He emphasises two critical priorities for the EPF – first, how it can help build more retirement savings for contributors, and second, how to ensure the fund is invested in the right asset classes to deliver sustainable dividends.

Williams sees more self-employed individuals and people in informal sectors contributing to the EPF.

He believes, however, the trend will taper off as people get back on track with their savings targets. However, he stresses the need for greater participation.

“There’s still a lot of room for more people to contribute. The EPF should also allow foreign members to make voluntary contributions,” he adds.

Kah highlights the loan-to-deposit ratio (LDR) of Malaysia’s banking industry, which stood at 87% in 2Q24, noting that a lower ratio could pose challenges for banks in extending loans.

“A low LDR of say 70% would present a headache to banks as it would indicate a challenge to extend loans to credit-worthy borrowers and lack of demand for loans, as it was during the global financial crisis of 2007-2008. The current LDR of 87% is ideal for banks,” he notes.

“The RM500 incentive has compelled many to save with the EPF. There is no doubt that the socioeconomic benefits are substantial and should be continued.”

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.