PLANNED reforms to revive the government’s finances have continued to gather pace since the start of this year.

This follows a recent announcement that, in addition to subsidy rationalisation, the government is looking at potentially abolishing the civil service pensions scheme for new employees.

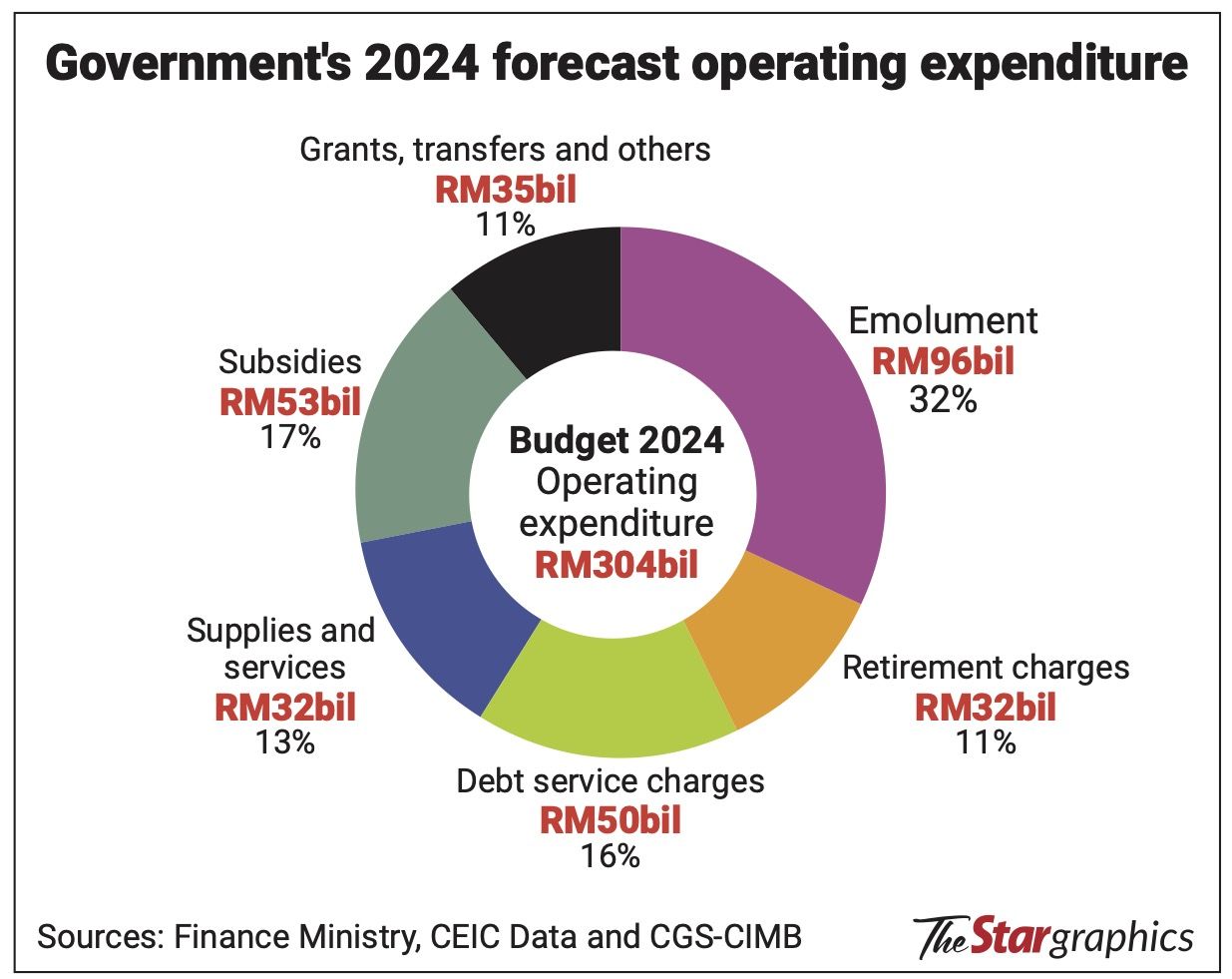

Pension payments, which are expected to make up some 10.7% or RM32.4bil of the government’s forecast operating expenditure of RM304bil this year, are among the key fixed cost components.

Data shows that the proportion of pension payments, which include gratuities, had remained constant since 2022, even though it had grown by 3.2% during the period in absolute currency terms.

It is also notable that the data shows debt service charges, which is another fixed cost expenditure that is expected to be incurred for 2024, is at RM49.8bil. This is 53.7% higher than pensions payment for this year.

The task of reforming the pension scheme can be difficult to address, but if rightly done, it can help move the nation forward and brighten its outlook, with economists and industry experts saying the government should capitalise on the strong parliamentary support it possesses presently to make the changes.

It also becomes more urgent and necessary, given the prospects of the country transiting into an ageing nation very soon.

This means there will be a lesser proportion of the younger populace in their prime productive ages to support the growing needs of the aged persons in the country; and with more aged persons in number, pensions payment obligations will continue to grow further as a proportion to the entire population.

Data by the Statistics Department shows Malaysia’s aging population appears to be growing at a faster rate compared to 30 years ago. The government agency also expects Malaysia to attain ageing nation status earlier than predicted.

The decline in the ratio of crude birth rate to crude death rate is having an impact on the structure of Malaysia’s population, which will accelerate its status to being an aged nation earlier than previously projected by the Statistics Department.

The increased life expectancy on better healthcare access and lower birth rates, which is a trend seen in many other developing and developed countries, is also quickening the pace of an aging population in Malaysia.

Pensioners are retirees who are eligible for payments. These include those who have opted for optional retirement at the age of 40 and have a reckonable period of service of no less than 10 years.

Pension payments for those who have opted for early retirement will only be paid later – upon reaching 55 years old for those who were appointed after April 12, 1991 into the public service, according to the Public Service Department.

Managing deficits

“The whole idea for pension reforms was premised on the need to ensure that government finances would be sustainable. The present structure would see expenditure on pension and gratuities growing further as the number of civil servants who will be retiring is increasing,” Bank Muamalat Malaysia Bhd’s chief economist Mohd Afzanizam Abdul Rashid tells StarBizWeek.

A rising retirement figure due to accelerating ageing demographics will put pressure on government finances, he says.

“The government also needs to keep other expenditure to grow the economy, especially for development spending.

“In the grand scheme of things, pension reforms can be deemed as part of the fiscal reforms agenda that may include the introduction of new taxes and a restructuring of the subsidies programme,” Afzanizam says.

“The goal is to achieve lower fiscal deficits and by extension, lower debt level. By achieving these two parameters, the government would have more fiscal space which can be spent on capacity-building programmes such as education, healthcare and infrastructure.

“This will then become the catalyst to the country’s economic development, one that is more productive and promoting the role of the private sector as the main of growth,” he adds.

Crucial move

His comments are echoed by another prominent economist, Lee Heng Guie, who says there is a need to reform the public sector pension scheme to make it financially sustainable.

Lee, who is the executive director of Socio-Economic Research Centre (SERC), points out that spending on public sector pensions and gratuities had increased from an average of RM1.5bil per year in 1976 to 1999 to RM19.4bil per year in 2010 to 2019 and further to RM32.0bil in 2020 to 2024.

“The historical figures also show retirement charges have accounted for an average of 10.7% of total operating expenditure compared to an average of 5.5% from 1976 to 1999,” Lee tells StarBizWeek.

Based on current projections, Lee notes the relatively large size of pensions in the government budget is expected to increase to RM46bil in 2030 and will further increase to RM120bil in 2050.

“Rising life expectancies also exerts pressure on the budget allocation for these retirement charges. Overly generous public pensions affects the behavior of individuals, who will be less inclined to save on their own for retirement needs.

“Less generous public pensions can drive up private saving because they induce people to save more for their mainly self-funded retirement,” he says.

“Pension reforms can avoid the need for even deeper cuts in pro-growth spending such as public investment for the healthcare, education, food security and elderly community services. It can also help to boost potential growth and may prevent a worsening of intergenerational equity,” Lee adds.

He notes proposals for reforming pensions systems is not just peculiar to Malaysia but other countries with similar demographics trends as well.

“Many countries have enacted significant pension reforms in recent years to contain the growth in the number of pensioners given the fiscal funding challenges brought about by the ongoing demographic transition.

“These include changing key parameters of the pension system, such as increasing the statutory retirement age and tightening eligibility rules,” Lee says.

Among them include a recent reform proposal in France which aims to raise the full-pension retirement age to 64; in Brazil where it increased retirement ages to 65 for men and 62 for women from the ages of 56 and 53, respectively.

“While in some countries, such as Cyprus, Denmark, the Netherlands and Portugal, the statutory retirement age is legislated to increase in line with rising life expectancy,” Lee says.

Root cause

However, AmBank Group chief economist Firdaos Rosli had a different point of view and believes dealing with the present pensions system will not address the root cause of the issue the country is facing now.

“I think the root cause of our discussion on this issue is that Malaysia’s revenue-to-gross domestic product (GDP) has been dwindling since 2003.

“It is imperative that we discuss this first, as this metric has been on a steady decline from 15.5% in 2003 to a projected 12.4% in 2023 and further to 12.3% in 2024,” Firdaos tells StarBizWeek.

He notes that it is concerning that Malaysia’s revenue-to-GDP is expected to be one of the lowest among the Asean member countries by 2025.

“This trend will make government expenses, including pension charges, appear ‘expensive or large’ as they cannot keep up with the economy. The mid-term review of the 12th Malaysia Plan projects the ratio to come in at 14.6%, which is even lower than the International Monetary Fund’s earlier projections of 15.5% by 2025,” Firdaos says.

He believes there are four ways the pension issue can be addressed but all of these require massive political will.

“The options are by making the average monthly cost of retirement “cheaper” in the future with controlled inflation, to increase the retirement age, to increase the defined contribution rate and to consistently maintain high GDP growth rates until the country reaches the ageing nation status,” Firdaos says.

Market rate

SERC’s Lee also notes that other reforms include a review in the size of pension benefits by reducing their generosity.

“This can be done by modifying the benefit calculation formulas, such as the inflation indexation component; rewriting valorisation rules or the adjustment applied to past earnings to account for changes in living standards between the time pension rights are earned and when they are claimed,” Lee says.

It may also include changing the accrual rate or the rate at which pension benefits build as member service is completed in a defined-benefit plan, he notes.

Meanwhile, a path to public pension reform might likely involve a transition to a defined contribution plan through the Employees Provident Fund (EPF) for new hires.

SERC’s Lee says this move will eliminate the potential risks in underfunding long-term pension liabilities.

However, there are also concerns among some quarters that such a system would penalise lower income earners among the civil service.

It is also learnt that the option to contribute to the EPF similar to a private employment setting is also given to civil service hires in recent years in place of pensions.

“If there will be a change in civil service renumeration schemes for a soon transit away from pensions, perhaps the government should consider paying salaries which are closer to the market rate.

“The government could also incentivise workers by topping up the employers EPF contribution for example as an added incentive,” says management consultant and formerly retired global managing director for Korn Ferry Datuk Tharuma Rajah.

Tharuma feels strongly against raising the retirement age further as this would deprive younger employees opportunities noting new employees can’t be brought into the system then.

“In reforming the public pension, we have to ensure a continued interest to pursue a career in the public service. In this regard, credible civil service reforms are needed to improve the quality and value of public services-based performance and productivity-linked salary system,” Lee says.

“The review of Public Service Remuneration System, including a new civil service hiring policy, should include rightsizing civil servants and accelerating digital government,” Lee adds.

New structure

On how the EPF compares with the present pensions structure, Afzanizam believes it will greatly hinge upon the whole remuneration structure.

“This may include the pay scale, opportunities for promotion and bonuses. Therefore, there is a need to review the remuneration scheme that can really promote a high performance culture,” Afzanizam says.

“Perhaps, once the EPF is in place it will then be more fluid and flexible in the sense that private sector employees would also be interested and can consider joining the civil service sector due to greater opportunities for learning and networking,” Afzanizam adds.

Similarly, he notes public sector employees can also venture into private sector employment as they may have already gained certain skillsets which will make them valuable from the prospective employer’s point of view.

“In a way, this may create a healthy competition for talent which can provide limitless opportunity for the public sector employees. I suppose the changes only apply to the new recruits and therefore, the changes shouldn’t create unnecessary pressure to existing staff,” Afzanizam says.

Meanwhile, the role for Retirement Fund Inc (also known as Kumpulan Wang Persaraan Diperbadankan or KWAP) will remain intact, given that they are only financing a fifth of the government’s pension obligations presently.

Pension obligations will still need to be paid even after any revamp as it had been stated the changes will not impact civil servants which have opted for pensions under the current system.

KWAP which is an active investor, especially in the local markets, was established in March 2007 to assist the government in financing its pension liabilities.

It was reported KWAP’s gross fund size stood at RM184.5bil at end-July 2023, with gross investment income of RM3.8bil from the January to July 2023 period.

KWAP’s 2021 annual report shows the fund recorded a gross investment income was RM6.33bil in 2021, which is slightly over a fifth of total pensions and gratuities payments of RM29.1bil in that year.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.