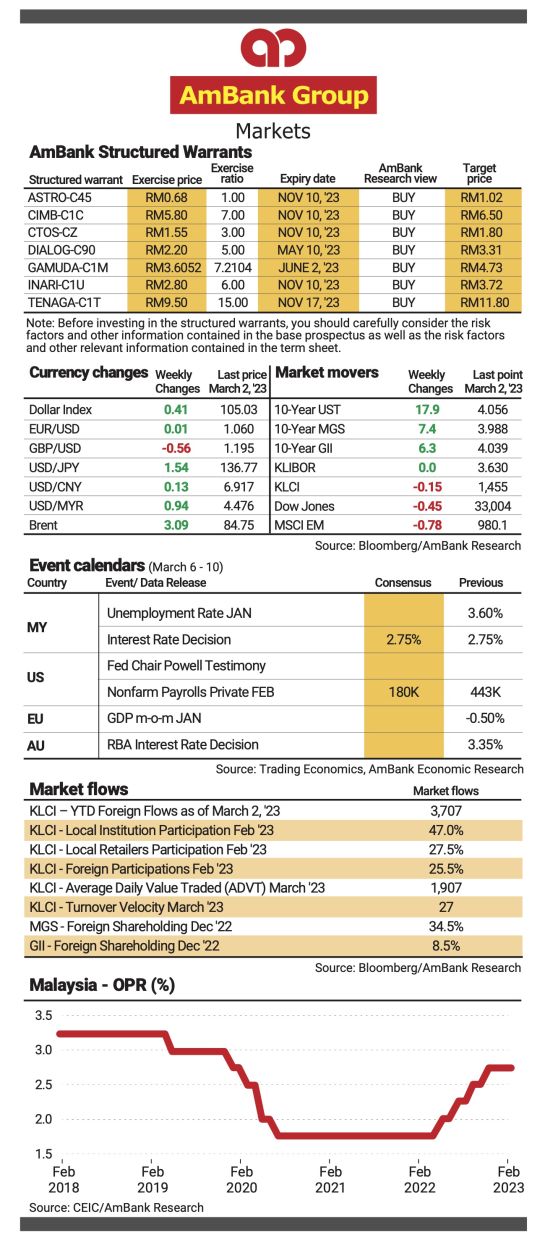

BACK in January 2023, the overnight policy rate (OPR) was left unchanged at 2.75%. This was after a cumulative 100-basis-point (bps) rate hike that had taken place since May 2022.

This is to allow the economy to adjust to the impact of the cumulative past OPR adjustments, given the lag effects of monetary policy on the economy.

Due to this reason, the probability of a rate hike in March 2023 has dissipated as compared to the earlier assessment at the beginning of 2023.

Assessment of the lag effect from the rate normalisation that had taken place since May 2022 may require a longer timeframe.

Approximately, the impact of the interest rate hikes would take effect within eight to 10 months.

Supply and demand factors

The caveat to this, however, is that the effect could be shorter or longer due to structural changes, given how the Covid-19 pandemic had affected both, supply and demand factors in the global inflationary environment.

Despite the relaxation of China’s zero-Covid policy which theoretically should boost markets’ optimism, concerns on the path of the policy rate ahead remains, as inflation in most part of the world remains elevated relative to their historical average levels.

This could also imply that concerns on a slower global economic outlook outweigh the good news from China, which is also supported by latest purchasing managers’ index or PMI numbers from the United States, the United Kingdom, eurozone, China and most of the Asean economies where they remained in contractionary level.

Inflation in most economies is easing, but at the same time, the effect from cumulative rate hikes in most parts of the world are clouding the growth outlook.

The compelling reason to keep interest rates above the inflation rate comes from the real interest rate perspective.

From past experience, it was not common for the real interest rate (defined as the OPR minus the inflation rate) to be in negative territory for two consecutive years.

The year 2022 could be an exception as global inflation rose to multiple-decades high, but there is a possibility that the real rate would return to a positive level.

Inflation receding

On prices, latest numbers showed that Malaysia’s headline inflation receded further from 3.8% in December 2022 to 3.7% in January 2023.

Core inflation (excluding volatile items and controlled prices) also slowed down from 4.1% in December 2022 to 3.9% in January 2023.

Core inflation continued its downward trend after peaking at 4.2% year-on-year in November 2022.

Guided by a historical trend analysis, it would take around 10 months for core inflation to approach the 2% levels and assuming the current trend persists, core inflation may move closer to 2% by October 2023.

Price pressures coming from the demand-side indicators are slowing down.

Wage growth in both the manufacturing and services sectors is slowing down, after peaking in the second quarter of 2022.

Furthermore, hiring activities, which are highly linked to core inflation, are also slowing down after peaking back in July 2022.

All of these point to a slower core inflation this year.

While the demand-side indicators are slowing down, the concern lays more on the supply-side.

The targeted subsidy was not mentioned during the Budget 2.0 re-tabling last week and no timeline has been given since then.

Supply disruptions

However, one thing that was noticeable was that Budget 2.0 has a wider range of headline inflation of 2.8% to 3.8% due to fluctuations in foreign-exchange rates and prolonged supply disruptions.

In contrast, the Budget 1.0 inflation forecast was between 2.8% and 3.3%.

Another concern from the supply-side is the compressed profit margins.

After two years of profit margin compression resulting from a higher consumer price index, there is concern that businesses may continue to pass-through the cost to the consumer to preserve profit margins.

Based on analysis, the profit margin (consumer inflation minus producer costs) finally went into positive territory back in November 2022.

This means that, there is a risk for businesses to charge much higher than the optimal prices to compensate for the losses of the past two years.

If this scenario materialises, inflation could remain elevated.

For FX enquiries, please contact: ambank-fx-research@ambankgroup.com. For fixed income enquiries, please contact: bond-research@ambankgroup.com.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.