THE Bursa Malaysia Property Index (BMPI) was last seen at 618.08 points and at this level, the index is down some 85.57 points or 12.2% year-to-date and languishing near a two-and-a-half year low seen in November 2020.

The index is also an underperformer when compared with the FBM KLCI, which is down by 7.2% year-to-date.

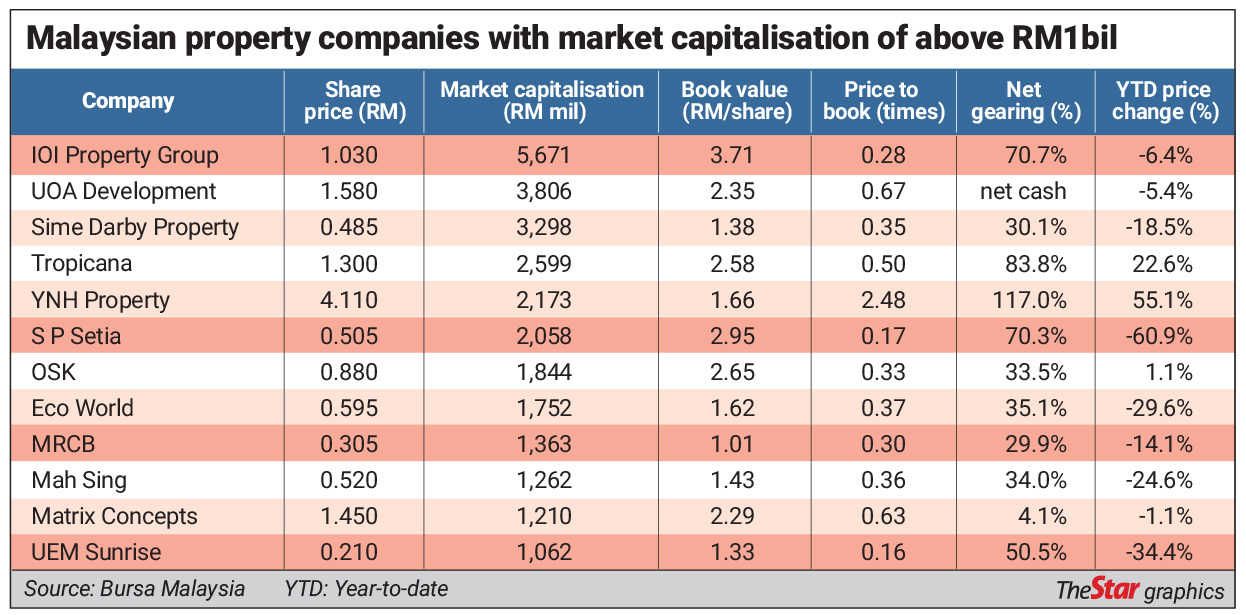

The weak performance of the index itself must be due to the weakness of the underlying stocks within the sector and dragged mainly by a few large property companies.

The table summarises the performance of selected top 10 property companies year-to-date and up to Oct 27, 2022.

As can be seen from the table, selected stocks have been a big drag on the BMPI, led by a 60.9% decline in the share price of S P Setia Bhd, followed by a 34.4% decline in the share price of UEM Sunrise Bhd and 29.6% fall in Eco World Development Group Bhd’s share price.

and 29.6% fall in Eco World Development Group Bhd’s share price.

Other notable decliners were Mah Sing Group Bhd, which is down by 24.6% year-to-date, and Sime Darby Property Bhd’s 18.5% drop.

However, there were also some strong performers among the top property developers, led by a 55.1% jump in the share price of YNH Property Bhd and a 22.6% jump in Tropicana Corp Bhd’s share price year-to-date.

What causes this divergence and why is it that, despite the stellar property market as claimed by many developers with resounding sales performance and strongly echoed by property consultants, the share prices of some of these companies are near all-time lows?

Gearing level is rising

Other than UOA Development Bhd, which has a net cash level of about RM1.87bil, all the other large property companies have seen deterioration in net gearing level, including perpetual papers which are classified as equity.

Net gearing level ranges between 4.1% for Matrix Concepts Holdings Bhd to as high as 117% for YNH and overall, among the big property boys’, excluding UOA Development, average net gearing is at about 54.5%.

Interestingly, we are also seeing some corporations raising capital for the sole intended purpose of retiring previous debt papers that were raised.

S P Setia has proposed a renounceable rights issue of up to 3.07 billion new Class-C Islamic redeemable convertible preference shares (RCPS-i C) at an issue price of RM0.38 per RCPS-i C on the basis of 67 RCPS-i C for every 100 SP Setia shares held with the ex-date on Nov 1, 2022.

Proceeds from the new RCPS-i C will be used to retire the earlier tranche RCPS-i Class B. The new RCPS-i C are convertible into new SP Setia shares on the basis of 32 new SP Setia shares for every 67 RCPS-i C.

In essence, the new SP Setia shares issued pursuant to the conversion of RCPS-i C are at a 79.56 sen per share or 38.3% premium from the theoretical ex-rights price of 57.55 sen based on last Thursday’s closing price.

Investors dislikes rights issues

While majority shareholders may have no choice but to resort to equity funding to retire old debts, minority shareholders may have a different view altogether.

Since the first announced proposal on April 27, when SP Setia was trading at RM1.22, the share price of the company has dropped 58.6% to its current level.

Clearly, the proposed rights issue has been a drag on the company’s share price, although fundamentally, SP Setia has performed reasonably well in 2022, with property sales of RM1.67bil while unbilled sales as at half-year was an astonishing RM8.71bil – equivalent to 2.3 times of its first six months annualised revenue.

With the trading of rights on the rights issue commencing on Nov 3 and the date of cessation of trading of rights a week later, there is also an arbitrage opportunity for SP Setia shareholders to switch to the lower-priced RCPS-i C, which is convertible to SP Setia ordinary shares, depending on the price of the traded rights.

Undeniably attractive

At its current share price, SP Setia, which has a book value of RM2.95 per share, is trading at an amazingly low price-to-book ratio of just 0.17 times.

In essence, an investor is buying a property company at an 83% discount from the net book value of the company’s assets.

Not only SP Setia is seeing such a low valuation, even UEM Sunrise is on par too with a price-to-book ratio of just 0.16 times while six other companies are in the range of between 0.28 times and 0.37 times.

UOA Development and Matrix Concepts are trading at a reasonable price-to-book level of more than 0.6 times mainly due to their healthier balance sheets, while YNH is an outliner with a very rich price-to-book ratio of almost 2.5 times.

Another undervalued stock is indeed OSK Holdings Bhd as the current market capitalisation of RM1.84bil is only 77% of the value of its 10.2% stake held in RHB Bank Bhd worth some RM2.39bil, based on the bank’s current share price.

In conclusion, with the BMPI down by more than 12% year-to-date, some large property companies have emerged at levels not seen in a long time when viewed on a price-to-book basis or in terms of simply too cheap to ignore.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.