TWO interesting documents were released by the government recently and they gave an interesting perspective as to where Malaysia is headed when it comes to employee compensation.

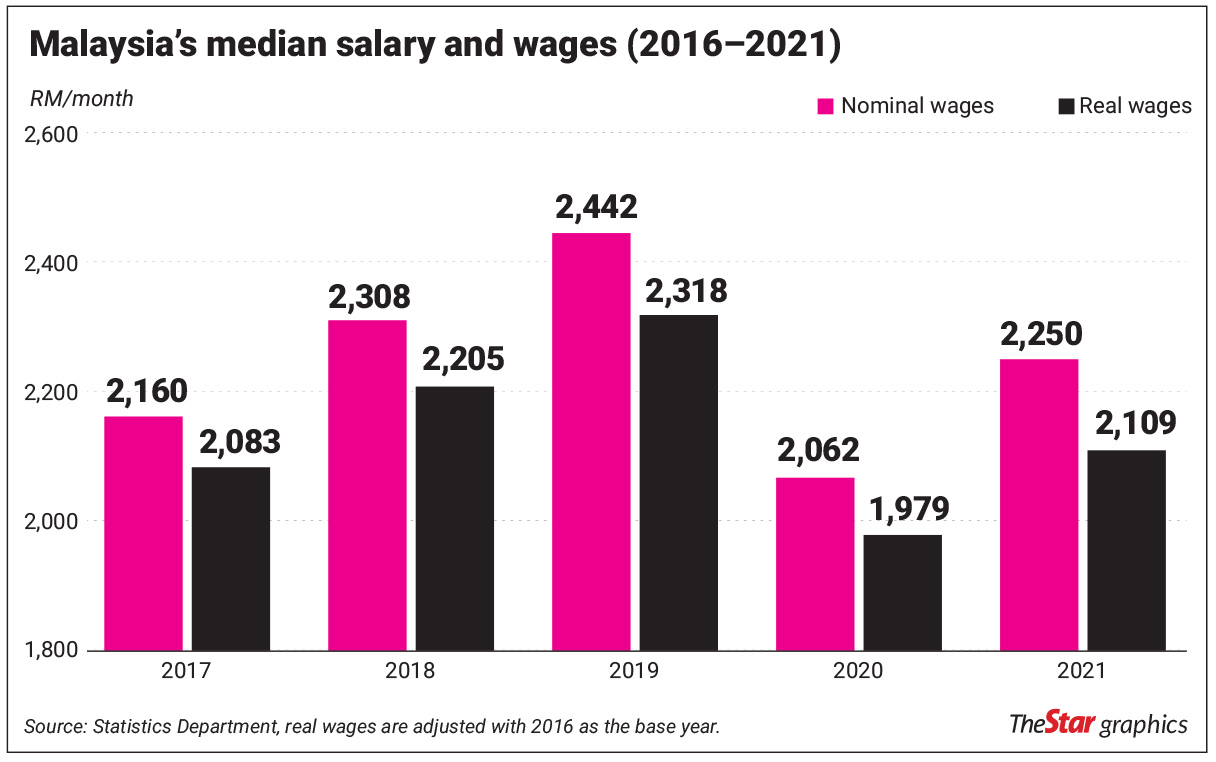

Just before Budget 2023 was released, the Statistics Department released the Salaries and Wages Statistics report for 2021, and interestingly it showed that the median salaries and wages rose by a staggering 9.1% year-on-year (y-o-y) last year to RM2,250 per month from RM2,062 per month in 2020.

As can be seen in the accompanying chart, the strong rebound last year is mainly due to the 15.6% decline in the preceding year as salaries and wages fell from RM2,442 per month in 2019 to RM2,062 per month in 2020.

The contraction and growth in wages followed the nominal gross domestic product (GDP) growth trend, which fell by 6.3% in 2020 but rebounded strongly in 2021 by 9% y-o-y.

The chart also shows that the median wages and salaries of RM2,250 per month are below the level workers were enjoying in 2018, when the median amount was RM2,308 and barely just 4.2% or RM90 higher than the level enjoyed in 2017.

This is even before taking into consideration the official inflation data. As the official consumer price index (CPI) rose by 3.7% in 2017, 1.0%, and 0.7% in 2018 and 2019 respectively, falling by 1.2% in 2020 and rising by 2.5% last year, real wages recorded a slower pace of growth.

In 2016 purchasing power terms, the 2021 real median wages stood at RM2,109, or just 5.5% higher than the RM2,000 earned in the year 2016.

On a compounded annual growth rate (CAGR) basis, real wages only grew 1.1% while the economy in real terms expanded by 2.4% CAGR over the same five years period.

In essence, the share of wages for workers as the economy expanded, has become smaller not only in nominal terms but also in real terms. In nominal terms, the Malaysian economy expanded by 4.3% CAGR between the years 2016 and 2021 but wages only grew by 2.4% over the same period.

Hence, if were to factor in the growth in wages as the economic cake grew larger, the workers’ share of wages is only at 0.55 times of nominal GDP growth and 0.44 times of real GDP growth over the past five years.

A low CE ratio

As wages are growing slower than economic growth, naturally the ratio of compensation of employees (CE) has been trending lower at the expense of rising Gross Operating Surplus (GOS).

According to a featured article in the Economic Outlook Report 2023, Malaysia’s CE to GDP ratio stood at 34.8% in 2021, down 2.3 percentage points (pps) from the preceding year’s level of 37.1% while GOS to GDP expanded by 2.8 pps to 62.9% last year from 60.1% in 2020.

Malaysia’s low CE ratio is worrying as it is the lowest level since 2014 when the CE ratio stood at 34.3% and a far cry from the expected CE ratio of 40%, which was pencilled in the 11th Malaysia Plan that was tabled in 2015.

Of course, this pipe dream of a 40% CE target was again repeated under the 12th Malaysia Plan and is now expected to be met by 2025.

For Malaysia to achieve the expected 40% CE ratio, wages would need to increase at a faster rate than the nominal economic growth in the future and not at half the pace as it is now.

Malaysia’s low CE was also recognised in the same report which not only showed the low CE ratio against several nations, which had a range of CE ratio of between 36.7% for the Philippines to as high as 54.2% for the United States.

Interestingly, Malaysia’s GOS of 62.9% in 2021 is the highest among the surveyed nations with the rest having a GOS ratio of between 37.1% and 58.6%.

The GDP measurement using the income approach also provides the balance of claim to the government in the form of taxes less subsidies.

Here, Malaysia fails miserably as that ratio stood at just 2.3% in 2021, well below the range seen in the surveyed countries of between 4.8% to as high as 10.2% in South Korea.For this year, according to the Economic Outlook 2023 report, CE for 2022 and 2023 is expected to improve marginally to 34.9% and 35.2% while GOS is expected to increase to 64.4% this year before easing to 62.2% in 2023.

As for the government’s share of national income, the tax collection net of subsidies as a percentage of GDP is expected to drop to a paltry 0.7% this year, mainly due to the surge in subsidies, and recover to 2.6% in 2023.

In essence, Malaysian employees are underpaid while the government is not collecting enough taxes or providing too many subsidies.

The result – the corporates are laughing their heads off to the bank with a huge operating surplus, which is later channelled back to capital providers, the shareholders, in the form of dividends or even huge capital gains when a business is sold – untaxed.

A big burden

If half the working population is only earning RM2,250 per month and below, it has a significant impact on the government’s finances. The first thing that comes to mind is that none of these employees are taxpayers as only those earning RM3,111 per month (under self-assessment or married with no children) are subjected to income taxes.

If married couples opt to be assessed separately, the threshold goes up to RM3,444 per month for those with two children, and for couples that opt to be jointly assessed, the taxman only comes knocking at the door if the couple with no children earns more than RM4,000 per month.

With no direct taxes collected from these taxpayers, the government has no choice but to assist the B50 group with all sorts of assistance programmes. Under Budget 2023, some RM7.8bil will be spent to assist the lower income group based on various categories defined by the government.

Second, with low wages and with inflation prints north of 4%, this group of employees is hardest hit as real income has dropped much more, eroding their purchasing power and impacting their living standards.

Third, low wages also impedes half of Malaysians’ ability to purchase a roof over their head. According to Bank Negara’s 2021 Annual Report, house prices are seriously unaffordable across most states as the house price to income ratio of 4.7 times (i.e. the median house price of RM295,000 divided by the 2020 Annual Median Income of RM62,508) is well above the acceptable threshold of 3 times.

Bank Negara also highlighted that the main reason for this is due to the low wage CAGR of just 2.1% between 2014 and 2020 against the rise in home prices, which expanded by a CAGR of 4.1% over the same period.

Higher wages is an economic booster

With such a high GOS, it is natural for owners of capital to feel threatened whenever a discussion on higher wages is brought forward. From increasing the cost of doing business to threatening business closure, employers will naturally like to compress wages as low as possible. Not only do Malaysian employers prefer to pay as little as possible, the hiring of foreign labour workforce too, which comes at a cheaper cost, has resulted in them resorting to having a greater preference in hiring foreigners than locals and thus depressing wage growth.

However, based on an article that was published in the Economic Outlook 2023 report, wage growth of between 3% and 5% has shown a positive correlation not only to the economy with higher GDP growth of between 5.6% and 6.5%, labour productivity too will improve by between 4.2% and 5.4%. Higher wage growth will also lower the income inequality index between 2.2% and 2.5%.

In conclusion, while Malaysia still aspires to achieve a high-income nation, which is presently defined as a gross national income per capita of US$12,535 (RM59,165), the weaker ringgit against the greenback and slower growth in wages is certainly delaying the time frame as to when Malaysia will be joining the elite club of nations with high income.

Having said that, while the World Bank expects Malaysia to achieve the target between 2024 and 2028, the devil is really in the detail, especially if half the working population is barely surviving with an income of less than half of what the high-income threshold suggests.

The prosperity of the nation lies in paying our workers better and not depressing wages via low-income structure and hiring of the cheap foreign labour force.

Pankaj C. Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.