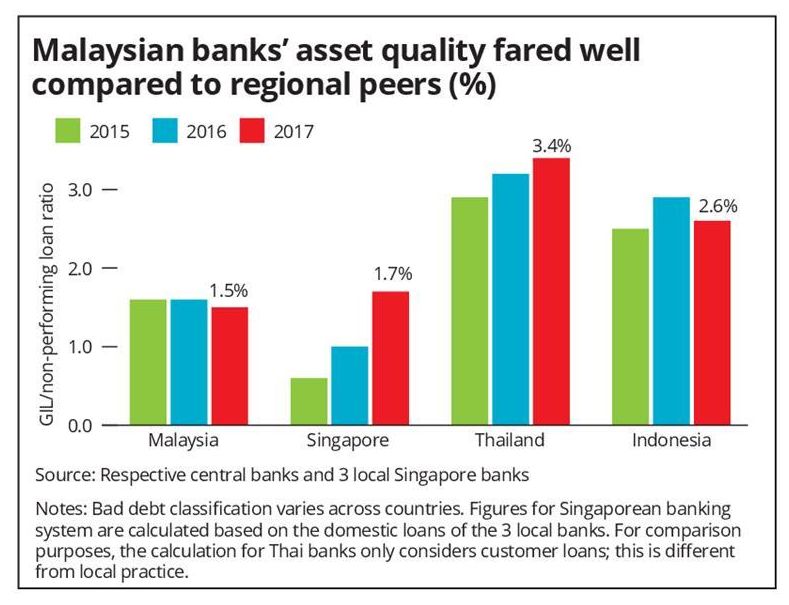

THE banking industry’s gross impaired-loan (GIL) ratio is expected to stay below 1.7% this year compared with the all-time low of 1.5% last year despite vulnerability in the oil and gas (O&G), commercial real estate and lower-income household segments.

RAM Ratings co-head of financial institution ratings Wong Yin Ching, who is maintaining a stable outlook on the Malaysian banking sector in 2018, says the Malaysian banking system’s GIL ratio ended 2017 at a historical low of 1.5%, and compares favourably against those of its Asean peers.

“Notably, Thai banks’ asset quality was affected by some large corporate defaults last year. On the other hand, Singaporean banks were dented by exposure to their local O&G sector, which has experienced more defaults than its Malaysian counterparts as the former has more offshore support service providers that have been worse hit than other sub-sectors,” she adds.

Last year, the credit-cost ratio of the eight Malaysian anchor banking groups eased to 33 basis points (bps) compared with 39 bps in 2016, thanks to lower provisioning pressure for some of their Indonesian and Thai operations. Nonetheless, provisions remained high for their Singapore’s O&G exposures.

“We expect Malaysian banks to uphold their healthy asset quality amid sustained economic momentum and accommodative interest rates, although some pockets of vulnerability remain in the O&G industry, commercial real estate and lower-income households. Despite the potential slippage from these segments, the system’s GIL ratio is projected to keep below 1.7% in the worst-case scenario,” Wong tells StarBizWeek in an interview.

She says the rating agency expect the eight anchor banks’ credit-cost ratio to edge up to 35-40 bps following the implementation of the new accounting standard MFRS 9, which generally brings forward the recognition of credit losses.

On the impact of the new accounting standard MFRS 9 on banks capital, she says for the eight banking groups, the first-day impact on their common equity tier-1 (CET-1) capital ratios is expected to range from neutral to 0.8 percentage points, which is deem manageable relative to their capital positions. MFRS 9 was implemented in January this year.

At present, the industry’s CET-1 capital ratio stands above 13%. Wong opines that MFRS 9 will reduce the cyclicality of banks’ performance. This, coupled with the continuation of regulatory reserve requirements, will bolster Malaysian banks’ loan loss coverage, she notes.

As at end-2017, the eight anchor banks’ provision coverage ratio, inclusive of regulatory reserves, had been strengthened to 102% (end-2016: 96%) as some banks had set aside additional regulatory reserves ahead of the implementation of MFRS 9.

Household debt

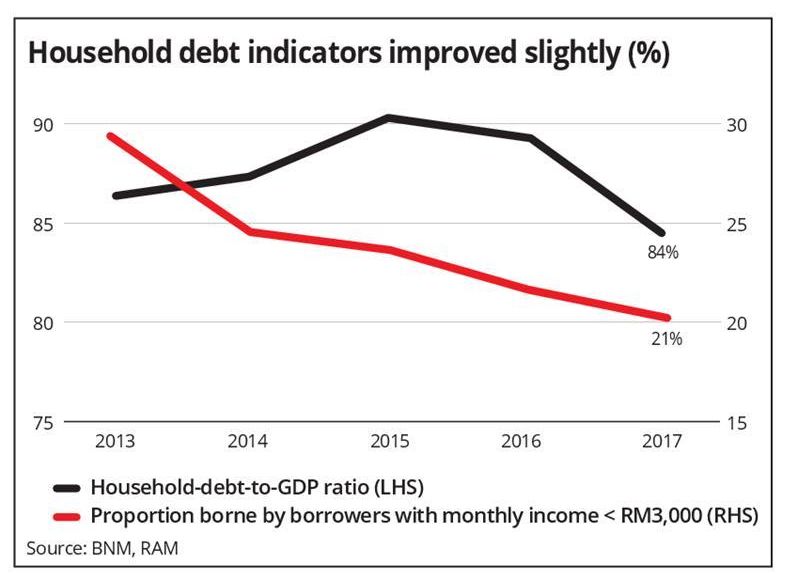

As for household debt, the rating agency’s fellow co-head of financial institution ratings Sophia Lee says although household debt continues to decelerate, it is expected to remain elevated for some time given the country’s young demographics.

About 26% of the population are aged 25-39, an asset-accumulating class that is growing at almost twice the rate of the overall population, she adds.

Lee says: “The various macro-prudential measures introduced in the last few years will help preserve the credit quality of household debt. In addition, banks have also upheld their prudent underwriting standards as most new household borrowers have debt service ratios that are below 60%.”

The pace of household debt accumulation continued decelerating to 4.9% in 2017 compared with 5.4% in 2016. This, coupled with rapid economic expansion, had further eased Malaysia’s household-debt-to-GDP ratio to 84.3% as at end-2017 (end-2016: 88.4%), compared to the peak of 89.1% as at the end of 2015. Nonetheless, this ratio is still on the high side relative to Malaysia’s per capita GDP.

She also cautions the lingering challenges from the vulnerable segment i.e. individuals earning less than RM3,000 per month in the urban areas amid the spiralling cost of living.

These borrowers, Lee says, are more susceptible to unemployment, inflation and interest-rate shocks, although the impact of any deterioration is expected to be contained as the borrowings of this segment had continued declining to 20.6% of household debts as at end-2017 from 21.9% as at end-2016.

The GIL ratio of household loans eased from 1.1% in 2016 to 1.0% last year. RAM projects the unemployment rate to remain at 3.3% in 2018 (2017: 3.3%) and expects the overnight policy rate to stay at 3.25% through the rest of the year, after the 25 bps hike in January.

On the business loan side, the GIL ratio of business loans stayed sound at 2.3% as at end-2017 (end-2016: 2.3%).

RAM Ratings remains cautious of the O&G sector, especially the support services sub-sector and expresses concern on the oversupply of office and retail space.

End-financing for offices and shopping complexes came up to a relatively small 3% of bank loans as at end-2017; working-capital lending to the same segments is also not likely to be significant, it says.

On a broader scale, the GIL ratio of loans for the purchase of non-residential properties inched up from a trough of 0.7% in May 2014 to 1.1% in December 2017.

There could be further slippage if oversupply persists, the rating agency notes. In this regard, the government has temporarily frozen the development of new shopping malls, offices and high-rise residential units costing above RM1mil, although this is not a blanket ban.

Net interest margin

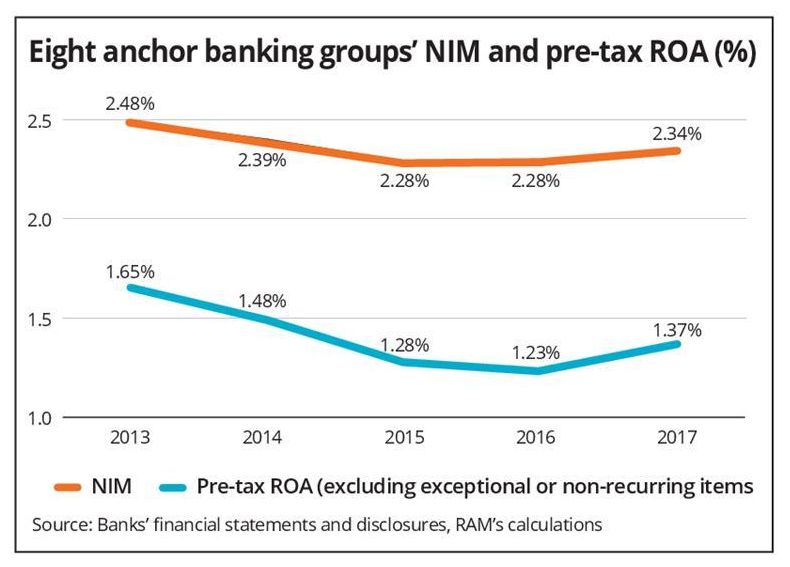

Meanwhile, Wong says the OPR hike in January will boost net interest margins (NIMs) in the short term, especially for banks with higher proportions of floating-rate loans as well as current and savings account deposits.

However, she says there could be some mild downside for NIMs closer to the upcoming Basel III net stable funding ratio (NSFR) implementation date.

NSFR is expected to be implemented no earlier than Jan 1, 2019.

The NSFR measures a bank’s funding stability over a one-year period and complements the liquidity coverage ratio (LCR) requirement, which measures liquidity over a 30-day horizon.

In view of the NSFR, she says banks have to either compete for retail/SME deposits, source for long-term wholesale funding or hold more liquid/short-term assets, all of which will affect their funding costs or asset yields.

“Besides, the NIMs of Malaysian banks with Indonesian exposures will be compressed slightly by the two rate cuts (summing up to 50 bps) in Indonesia in the second half of 2017 where the full-year impact will be reflected in 2018.

“As such, we expect the eight anchor banks’ NIMs to remain relatively unchanged in 2018. This, coupled with our view that loan growth will pick up and the incremental credit cost arising from MFRS 9 will be manageable, reinforces our expectation of a stable pre-tax return on asset (ROA) this year,” says Wong.

The aggregate pre-tax profit of the eight anchor banking groups (excluding exceptional or non-recurring items) increased 15% in 2017, translating into a satisfactory pre-tax ROA of 1.4% (2016: 1.3%).

As the NSFR favours long-term or stable funding, Lee says banks are likely to continue diversifying their funding sources through the capital markets. “There has been an increase in banks’ issuance of senior notes/sukuk, both in terms of the number of issuers and issuance value,” she says.

All said, she adds customer funding (i.e. customer deposits and investment accounts from customers) still account for the lion’s share ie more than 80% of banks’ interest-bearing funds.

The growth of customer funding accelerated to 3.5% in 2017 (2016: +3.1%), thanks to a recovery in corporate earnings. To a small extent, customer funding growth was also underscored by an estimated capital inflow of RM2.8bil (equity market: +RM10.8bil; bond market: -RM8.0bil) in 2017 – the first full-year net inflow since 2013. The banking system’s loans-to-deposits and loans-to-funds ratios were largely unchanged at a respective 89% and 84% as at end-January 2018.

Based on the latest figures, the rating agency noted that the banking system’s funding and liquidity conditions are sound, with a Basel III NSFR of 107% (latest available position as at end-June 2017) and a LCR of 135% (monthly average for 2017).

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.