HOUSING and the other segments of the property sector make up an important part of the economy.

Its influence goes beyond just a share of the national economic pie or how much loans the sector is generating for financial and lending institutions.

There is the social aspect of it. Unlike some developed countries, where its population are quite happy to rent, in Malaysia, home ownership is important.

Amid the current issue about affordability, ironically there is today the issue of completed but unsold units.

Socio Economic Research Centre executive director Lee Heng Guie looks at housing, which has gone beyond just a roof and a floor:

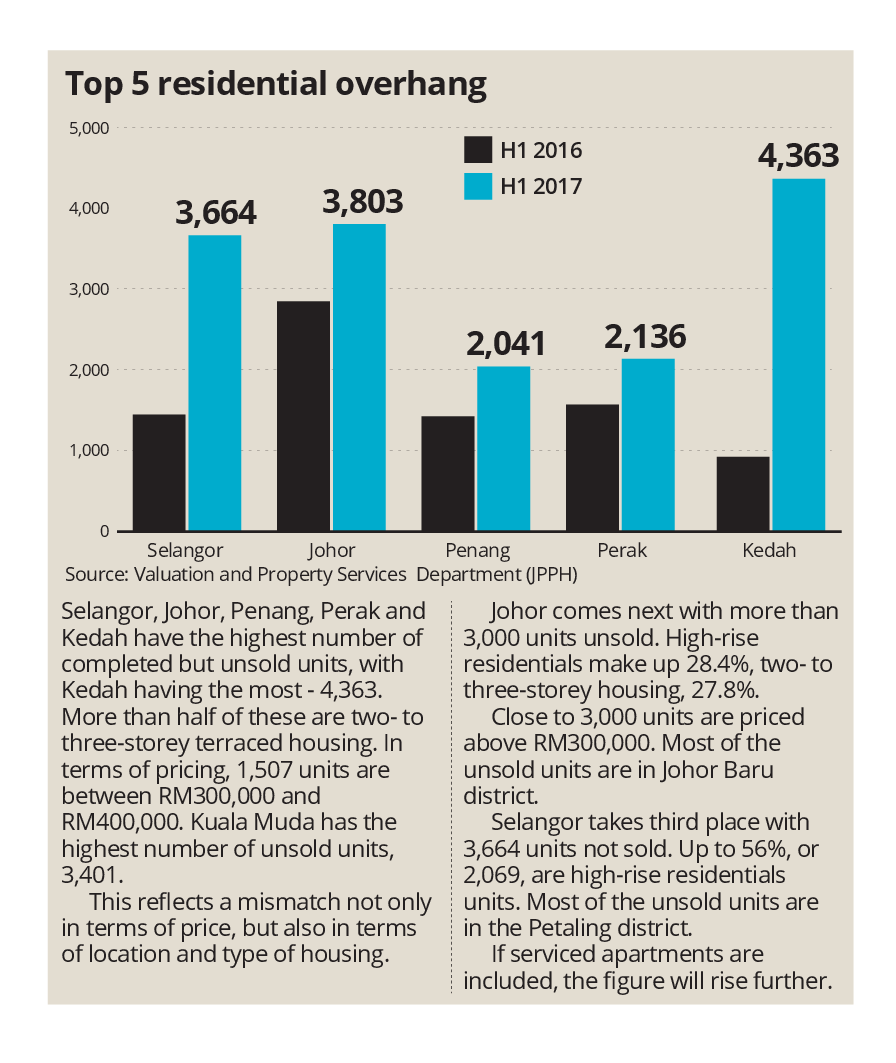

Napic has just announced overhang units to the tune of RM12.26bil, up from more than RM8.5bil as at the first half of 2016 and RM4.9bil for 1H2015. Besides the Napic explanation of a mismatch of price, location and type of property, is there any other issues why the overhang continues to grow even among prices less than RM500,000, although RM500,000-RM1mil segment form the bulk of the overhang.

It’s also about income-price affordability. For households with monthly income of between RM6,000 and RM7,999 and between RM8,000 and RM9,999 respectively, the affordable house price ceiling is RM408,500 and RM493,500 (based on Housing Cost Burden approach which deems it is affordable if housing costs are within 30% of net monthly income).

In 2016, the mean income of middle 40 (M40) household was RM6,502 per month, meaning that the household can only afford to buy houses costing between RM350,000 and RM400,000.

Buyers remain cautious, and sentiments are weak on concerns about the employment and income stability as well as economic prospects.

Buying property is a long-term commitment, and hence, the buyer must have good financial planning before committing to a big ticket item.

While the economy has performed better than expected this year, the “feel good” sentiment was not fully felt as rising prices of goods and services as well as higher cost of living had dampened income growth.

We are still lacking a sense of confidence that the economy is really gaining ground.

Perhaps, it takes some time for consumers to convince themselves that the weak economic environment has stabilised and gained momentum. The ringgit is stabilising.

Why is there this huge difference of opinion between a property crash after Chinese New Year 2018 and the other bullish view that China’s Belt Road initiative will help to drive more investments, and more need for top grade office space and residentials in Malaysia?

Everyone is entitled to his own opinion, based on rational assessment and fundamental analysis.

Malaysia’s residential property sector has been consolidating for a couple of years since late 2014. Overall house price index, which measures aggregated price indices for all types of residential properties have moderated for four consecutive years to 6.9% in 2016 from 11.0% in 2012.

The house price index remained stable at 6.9% in the first half of this year.

Residential property transactions volume continued to decline by 7.0% year-on-year (y-o-y)-to 94,992 units in the first half of 2017, albeit slower when compared to a sharp drop of 13.9% in 2016 and -4.6% in 2015.

In terms of value, residential property transacted value rose marginally by 0.5% y-o-y to RM32.85bil in the first half of 2017 after contracting by double-digit rates of -10.5% and -10.7% in 2015 and 2016.

Looking at current and forward market and economic conditions, the probability of a crash in the property market is small. Intervention policies have already been introduced to reduce financial stability risks associated with high household debt (at least 50% for the purchase of residential property).

Property prices are still growing but at a more moderate pace, thanks to the macro-prudential and property cooling measures. The well-contained property overheating risk market environment would shelter the sector from the negative spillover if there is economic or financial shock.

On the economy, the global economy is expected to continue growing, underpinned by a broadening recovery in advanced and emerging economies.

Our domestic economy is expected to grow decently by 5.1% in 2018, supported by the 2018 Budget’s pro-growth, investment and consumption measures and initiatives.

The unemployment rate is estimated at 3.3%-3.4% in 2018. Retrenchments totalled 18,539 persons in the first half of 2017 and retrenchments are expected to be milder compared to high retrenchment of 38,499 persons in 2015 and 37,699 in 2016.

The risk factors that would dampen buyers’ sentiment is the expected small rise in interest rate, rising cost of living, lower income growth and job loss.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.