Experts suggest saving a third of monthly earnings

ONE should not rely solely on his or her Employees Provident Fund (EPF) savings for retirement even though the entity has been set up with the aim to provide the best retirement savings scheme for its members.

Experts recommend that people save at least a third of their monthly salary so that they can retire with enough savings.

That’s simply because many people find their retirement funds to be insufficient to support their lifestyles after they stop working.

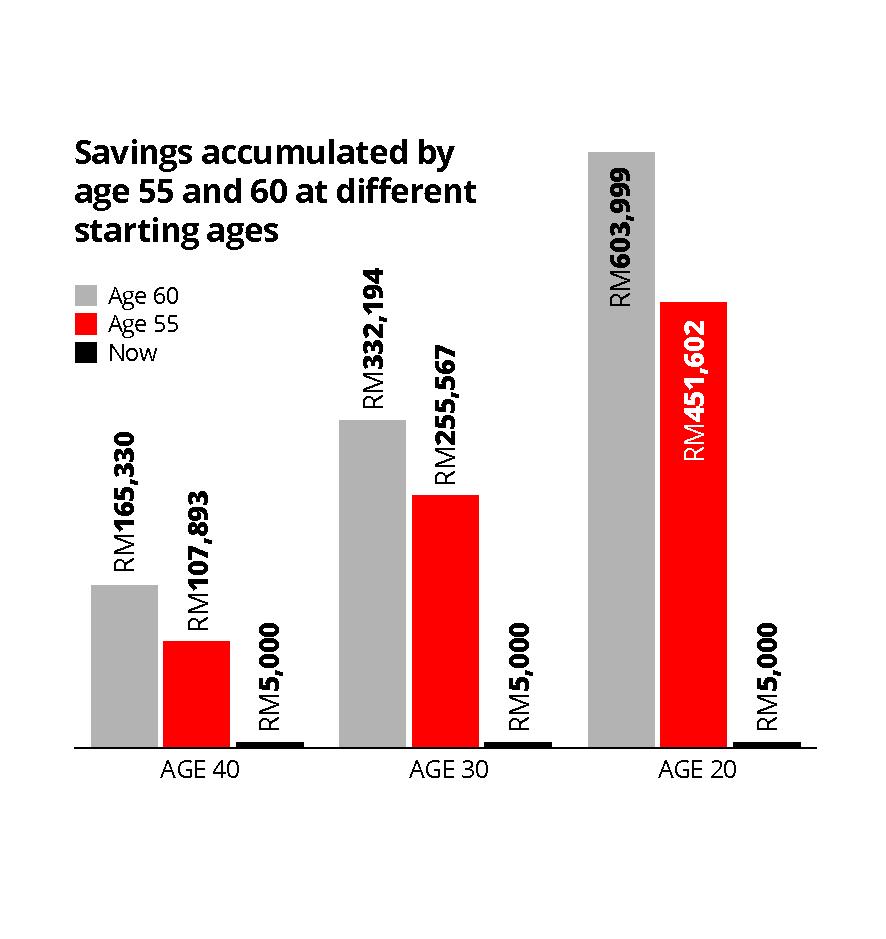

EPF encourages people to save early and to save as much as they can.

This is so that they can enjoy the power of compounding on their savings.

EPF members who start saving early will eventually accumulate more savings than those who only start saving at a later age.

It is important to remember that EPF savings are meant for retirement and members who make pre-retirement withdrawals are in fact withdrawing their future savings which will ultimately affect the adequacy of savings when they retire.

Malaysians need to take charge of their financial planning and constantly conduct personal financial health checks.

EPF advises members to create a financial plan according to one’s needs as there is no one-size-fits-all approach in developing a financial plan what with different retirement goals and needs for everyone.

When making a financial plan, it is important to think about the retirement income needed once one stops working.

This means estimating the number of one’s retirement years and determining the amount of income needed monthly to support retirement life.

Generally, women tend to lose their health in the last ten years of their lives and it is seven years for men.

Therefore, it is important for members to accumulate funds to cater to their healthcare needs during retirement especially when healthcare cost is increasing.

It is also vital to consider the number of dependents one needs to support such as parents and children, when creating the financial plan.

Saving for the golden age and rainy days

Some people find themselves poor shortly after they retire because of the rising costs of living, inadequacy of retirement savings, longer life expectancy and lack of financial literacy.

According to EPF strategy planning office head Farizan Kamaluddin, half of ex-EPF members exhaust their EPF savings in five years.

Some overlook the need to save for healthcare expenses, which are on the rise. And because of unexpected illnesses, some retirement funds can take a blow as a result of medical funding needs especially if a person does not have medical insurance or does not have sufficient coverage.

To have enough for retirement, she advises people to start saving young and to save as much as they can.

If members can afford it, they can save using other financial instruments or they can choose to top up their savings with the EPF.

Members must bear in mind that the savings serve as retirement income but not for current consumption.

She explains that most people’s EPF savings are not sufficient because they started off with very low savings when their salaries were still low. After many years, they salaries grow and their lifestyles change.

On top of that, they become the sandwich generation whereby they have younger children to take care of and older parents who need their support.

Private Pension Administrator (PPA) Malaysia CEO Datuk Steve Ong recommends that everyone sets aside a further 10% of one’s monthly salary on top the 23% that is deducted automatically from one’s salary into their EPF accounts.

He estimates a person’s retirement fund to cover two-thirds of his or her last drawn salary every month.

So, how much is needed for retirement?

“You need to save one third of your monthly pay now to get two-third of replacement income when you retire,” Ong stresses.

Ong says most people are not well-prepared for their retirement because of some “dangerous assumptions”. In a survey, only 21% of the respondents are prepared for retirement.

They are:

> My EPF savings will be enough.

> My children will take care of me.

> I’ll start tomorrow.

> It’s too early to start.

> I find it too hard to save.

> I want to enjoy now.

> I have loans and bills to pay.

Because of these beliefs, many senior citizens cannot afford to retire.

“A retirement fund is supposed to stretch over a period of time to support the person’s lifestyle after his or her retirement so that the retiree does not have to depend on other people.”

Farizan says how much is needed can be subjective too as it depends on the person’s lifestyle.

Diversification is key in saving for retirement

The private retirement scheme (PRS), for instance, is one way to complement one’s EPF savings.

Ong says putting money into PRS will ensure that a person’s savings is hedged against inflation. Otherwise, the purchasing power will shrink over time.

PRS is a voluntary savings and investment scheme that is designed to help individuals save more for their retirement. It was introduced in Malaysia back in 2012.

“The beauty of PRS is that you can start as small as RM100. That’s compared to other forms of investment, which may require bigger capital,” he quips.

On top of that, a PRS member can change the service provider if he or she is not happy with the performance or services provided.

He says PRS members should monitor the performance of the service providers so they should stick to no more than three providers at a time if they want to diversify their investments.

However, they should bear in mind that these are long-term investments and the schemes are designed to protect and grow their funds.

“It’s more important to look at the long-term average returns rather than short-term performance of the schemes.”

Currently, there are eight PRS providers that are approved by the Securities Commission.

They are Affin Hwang Asset Management Bhd; AIA Pension and Asset ManagementSdn Bhd, AmFunds Management Bhd, CIMB-Principal Asset Management Bhd, Kenanga Investor Bhd, Manulife AssetManagement Services Bhd, Public Mutual Bhd and RHBAsset Management Sdn Bhd PPA’s role is to look after the interest of all PRS members.There are 160,000 PRS members now compared to 6.66 million EPF members as at 2014.

As at October, the youth sector is the largest as they become more aware of the importance of financial planning. The Ministry of Finance is also giving out a RM500 incentive for youths aged between 20 and 31.

“Time and compound growth is your friend,” Ong says.

He says everyone including self-employed people can explore PRS as an alternative due to the vast selection out there.

“Malaysia has one of the best retirement saving systems. We’ve got one pillar right through EPF and the second one can be done through PRS.

“In time to come, all Malaysians should have more sufficient income and financial security upon their retirement.”

More options

Going forward, she says EPF is looking to introduce a syariah-compliant fund so that its members have the option to choose where they want to put their money in. The option will be open to all members and is expected to come out in 2017.

“We are still fine tuning the plans. The EPF will provide more details when it’s ready.”

On top of that, it is also looking to introduce retirement savings where members aged 55 to 60 can choose to add new contribution into their existing pension fund.

She encourages members to get free retirement advisory service from its consultants EPF RAS (Retirement Advisory Service) officers who offer impartial guidance to members on how they can make decisions on their EPF savings and make their money last longer throughout their golden years.

“Members will also be given guidelines and options to help them manage and grow their EPF savings.”

The service is one of EPF’s long-term plans to enhance its service delivery and help members achieve a sustainable retirement.

The goal is to ensure that members can make informed decisions on how they use their retirement savings before and after retirement.

The service is available in seven EPF branches, namely: Kuala Lumpur, Petaling Jaya, Seberang Jaya, Johor Baru, Ipoh, Kuantan and Kota Kinabalu.

They can also make full use of EPF Savings Calculator for their retirement planning.

The tool that is available on EPF’s website allows members to calculate how much they’ll get upon their retirement.

By planning from now, members will know how much more they need to save and whether they need to increase their savings to achieve the desired retirement fund in the future.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.