ALL eyes are back on the ringgit as the currency returns to the headlines, and perhaps for the first time in a long while, it is for a good reason.

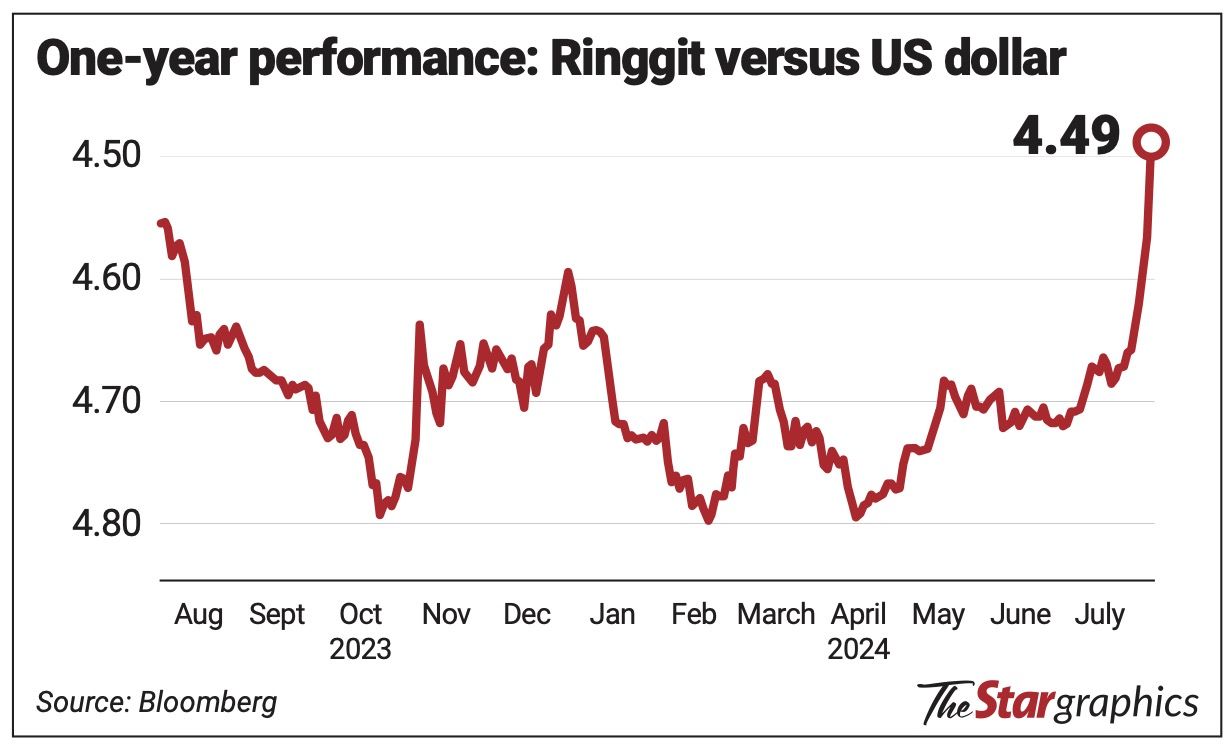

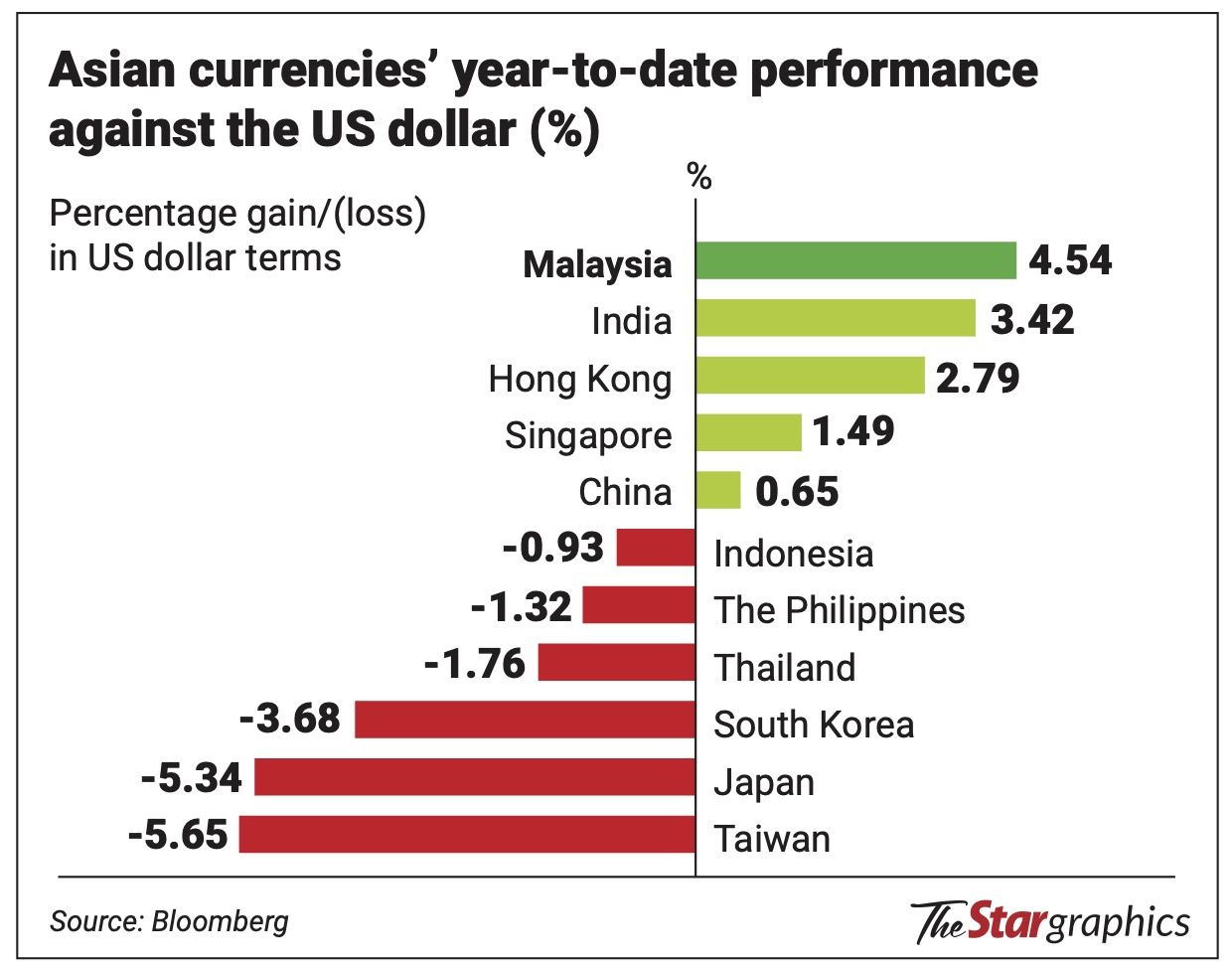

The local currency has appreciated approximately 4.5% year–to-date against the US dollar, according to Bloomberg data, but more importantly, it has notably sustained a steady level of strengthening against the greenback, especially when compared to other Asian currencies.

As HSBC Global Research’s head of Asia foreign-exchange research Joey Chew put it late last month, the relative steadiness of the ringgit has stood out as the rest of Asia continues to face weakness against the greenback. In this sense, the ringgit has turned out to be an out-performer.

Compliments for the Malaysian note has been something of a rarity in recent times, as the public can only remember all too well the familiar sinking feeling of witnessing the ringgit drop to its all-time weakest level of close to RM4.80 per dollar on Feb 20 this year.

However, as Malaysians heave a quiet sigh of relief that the local note has appreciated markedly to around RM4.49 to the US dollar and build up hope that it can maintain this positive swing, several economists who have predicted the comeback have outlined their reasons.

This comes as the ringgit has not only performed well against the American note since February, but has also gained against a basket of major currencies, including the Singapore dollar, Chinese yuan, Japanese yen, Hong Kong dollar, Thai baht and the British pound.

So, the million-ringgit question, or questions, remain: What has contributed to the recent rise of the Malaysian currency? Has the government got anything to do with it? And most importantly, can this be sustained going forward and benefit the rakyat?

According to senior economist at UOB Global Economics & Markets Research Julia Goh, the ringgit’s strong run began in July from RM4.72 earlier in the month to around RM4.49 currently against the US dollar, while observing that it can also be seen gaining momentum against other popular pairs such as the Singapore dollar, Australian dollar and British pound.

Unsurprisingly, researchers and experts like her feel that the ringgit’s current appreciation – as well as its previous slump – is down to a mixture of both domestic and international causes.

External factors

Of interest, Goh tells StarBizWeek that the sharper gains can be attributed to a weaker greenback, as markets have priced in two Federal Reserve (Fed) rate cuts in the second half of the year, alongside recent gains in the Japanese yen and Chinese yuan which are key trading partners in the region.

“The rally in the yen to its strongest level since March, after the Bank of Japan’s surprise rate hike at this week’s meeting, further spurred the gains in Asean currencies including the ringgit,” she explains, while noting that the yuan has also recovered to stronger levels against the US dollar.

Professor of economics at Sunway University Dr Yeah Kim Leng predicts that the US economy appears to be heading for a soft landing, which may need an easing in interest rates to avoid a sharp deceleration in growth.

With inflation easing albeit slowly, he agrees with Goh that expectations are high for the Fed to signal a rate cut in September that will exert greater downward pressure on the US dollar.

He remarks: “Other factors contributing to the US dollar weakening include concerns over the large fiscal deficit of the United States and its ballooning government debt.”

Looking at domestic factors, Goh says her channel checks suggest higher foreign portfolio inflows into Malaysia’s capital markets in recent weeks have also contributed to the stronger standing of the Malaysian currency.

In addition, she observes that since Bank Negara initiated coordinated measures to encourage conversion of foreign currency income by government-linked companies (GLCs) and government-linked investment companies (GLICs), the ringgit has shown more resilience and stability through bouts of US dollar strength and yuan weakness.

“Besides, the government’s engagement with corporates and investors while monitoring conversion of export proceeds and import payments also helped matters,” she opines.

Moreover, she believes that the availability of a fast-track process for corporates that repatriate funds to reconvert and reinvest abroad when the need arises also instills more stability and confidence in the ringgit.

At the same time, Sunway University’s Yeah, who is also an adviser to the Finance Ministry, says improving domestic fundamentals such as stronger-than-expected gross domestic product (GDP) growth that is estimated at 5% in the first half of the year have provided support for the local note.

He elaborates that other tailwinds for the ringgit include rising exports, low inflation and strong foreign direct investment inflows along with other positive investor sentiment on the economy’s near-term outlook.

This becomes more evident if compared to the other countries in the region, he reveals, including China, who is still unable to stimulate consumer spending amidst an ongoing property market slump and local government debt woes.

On this note, leading economist professor Geoffrey Williams acknowledges that the ringgit has first stopped depreciating, then it stabilised and is now strengthening, and he believes the recovery path is firming up and should continue during the rest of the year.

While recognising that new data on economic growth and the government’s rollout of policies have played a significant role, he says the main drivers behind the ringgit’s strengthening are developments in the international markets in which economic uncertainties are priced in.

Williams comments: “Exchange rates are the relative value of one currency against another, so it is the relative improvement in Malaysian uncertainties versus other economies that matters.”

Government influence

Glancing ahead, UOB’s Goh says it is crucial to build on the positive developments in the last few months to provide grounds for further ringgit upside once external headwinds abate.

This would include enacting more proactive measures, coupled with sound domestic fundamentals that are enhanced by a persistent current account surplus and positive growth prospects.

She says expectations of the Fed possibly starting its easing cycle in September and a steady overnight policy rate (OPR) are factors which may spur further gains in the local note.

“On the other hand, risks to this view include heightened geopolitical risks particularly in the Middle East, potential implications heading towards US elections and an uneven recovery for China’s economy,” she cautions.

Meanwhile, Williams continues to be wary of external factors outside the control of Malaysian policymakers, as he emphasises that geopolitical risks are still very much present.

As such, he says policy intervention by Bank Negara, especially to encourage repatriation of profits from GLCs and GLICs as well as Malaysian exporters, has played a prominent role and has been successful in creating demand for the ringgit which strengthens the currency.

“It also shows that the central bank is managing things well, which improves confidence in the policy environment,” he says.

Aside from geopolitical factors and global political stability, Yeah points out that the high interest rate environment in the United States for the past 24 months and weak global trade were major issues dampening the ringgit that persisted until recently.

Viewing from a different perspective, he explains that proactive efforts to shore up the local currency include policy makers’ explicit communication to the market on the ringgit’s undervaluation and the strength of the financial system to cope with volatile short-term capital flows.

He says Bank Negara’s call to GLCs and GLICs on their repatriation of overseas profits and proceeds has also helped to forestall further currency slides by strengthening the demand for the ringgit, as well as reducing unwarranted speculative ringgit trading.

Long may it continue

Like Williams, Nouri Chatillon, Asia Pacific economist at credit insurer Coface, reckons that there are a plethora of reasons why the ringgit should sustain its momentum going forward.

“Among these are the ongoing improvements in the trade balance, liquidity withdrawal by Bank Negara, the repatriation of profits by state-owned enterprises, the scaling back of outward investments by government-linked agencies and the potential easing of the dollar strength,” he says.

Chatillon notes Malaysia is also benefiting from the technology cycle boost, and exports are set to gain momentum and further support the ringgit.

“The ringgit’s strength appears to be the result of a combination of positive catalysts. Most importantly, Malaysia’s solid economic fundamentals have shielded the currency from excessive volatility seen in other Asian currencies caused by a stronger US dollar,” he says.

To note, MIDF Research in a write-up released on Thursday expects sales for the consumer sector to remain stable with the appreciating ringgit, but says export revenue in US dollars will translate to lower ringgit revenue.

Nevertheless, it says the primary positive factor for the companies in this industry is the reduction in costs for imported raw materials, ingredients, packaging and equipment, which can improve profitability.

“While there may be some revenue pressures for companies with significant export operations or dollar-denominated revenue, these are generally outweighed by the cost savings from a stronger ringgit,” it writes.

The research outfit says most consumer companies under its coverage will benefit from better local sales and cheaper imports of raw materials, packaging and machinery, and as such, reduced input costs could lead to improved profit margins.

Citing the example of Nestle (M) Bhd , MIDF Research says despite its parent company operating in dollar-denominated products, the group imports most of its raw materials in dollars but sells its goods in the ringgit, with the domestic market making up approximately 80% of its sales.

, MIDF Research says despite its parent company operating in dollar-denominated products, the group imports most of its raw materials in dollars but sells its goods in the ringgit, with the domestic market making up approximately 80% of its sales.

“Nestle’s earnings are estimated to increase 1% for every 5% depreciation of the greenback. However, Nestle is susceptible towards buyer sentiments following changes in the global geopolitical environment,” it says.

Moving to the travel industry, the research outfit says local airlines also stand to gain if the ringgit continues to strengthen against the greenback.

“For Capital A Bhd, nearly half of its aviation operating costs are in dollars, predominantly due to jet fuel expenses. In terms of its currency profile for borrowings, approximately 50% are in dollars. A 5% change in our dollar-to-ringgit assumption affects its earnings for the year ending December 2024 by 10%,” says MIDF Research.

An analyst from a local think tank, commenting on the effects of a stronger ringgit on the public, says Malaysians should gain on many fronts, some more immediately than others, but warns that it could also prove to be a double-edged sword.

“Ultimately, it depends on who you talk to,” he laughs.

The analyst says if companies in the consumer sector can breathe easier, it should logically mean they can manage their costs better with the stronger currency, instead of having to pass them on to consumers.

From an immediate perspective, he is of the view that individuals who are travelling and parents who are sending their children overseas for tertiary education will definitely appreciate the ringgit’s recent gains.

He pictures: “Just imagine that a mere six months ago, we were staring at a dollar exchange rate of RM4.80 and now it is around RM4.49. Of course, parents who have children in the United States or elsewhere will feel a difference to their pockets.”

On the other hand, he says institutions that cater to retirement such as the Retirement Fund Inc and the Employees Provident Fund, which holds approximately 38% of its total assets overseas, a persistently strong ringgit could mean lower realised profits for the year.

Williams feels that a fair value for the ringgit might be RM4.20 to RM4.30 by year-end to the US dollar if fundamentals are strong, but concedes that a more reasonable estimate might be in the RM4.50 to RM4.60 range, while predicting the local note to average around RM3.10 to RM3.20 to the Singapore dollar by December.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.