WHILE the market could have been “forgiving” when the fourth quarter of last year’s (4Q22) earnings report card was released in February supported by most broking firms’ view that the worse was behind, the 1Q23 earnings reporting season was a washout.

It turned out to be not only “same-old, same-old” but was probably the worst reporting quarter in recent times, which prompted almost every broking firm to cut earnings forecast as well as the FBM KLCI target level rather drastically.

Specifically, Malaysia’s bellwether companies were hit by a series of factors that were more sector-specific while margin erosion among consumer stocks was the main theme due to higher input and operating costs as a result of a jump in electricity tariff and labour costs.

The plantation sector suffered from the reduction in average crude palm oil price during the quarter as it averaged at just under RM4,000 per tonne against RM6,050 a year ago, although on a quarter-on-quarter (q-o-q) basis, prices were relatively unchanged.

Banking stocks saw robust earnings growth but the market’s concern on narrower net interest margin, which fell by 20 basis points to 46 basis points on a q-o-q basis, may persist for a while more. The technology sector did poorly as the slump in global semiconductor sales and overcapacity took its toll on the sector.

The oil and gas sector too was relatively weak on the back of shrinking margins, while the glove sector remains under pressure due to over-capacity and floored average selling price.

Businesses involved in selling big ticket items saw a mixed picture, perhaps a reflection on seasonality, as property developers tend to have a slow start in any given year,.

Meanwhile, automakers continued to benefit from the Sales and Service Tax exemption as long as motor vehicles were delivered by the end of March 2023.

Nevertheless, certain sectors did show strong performance in the 1Q23 period with the Real Estate Investment Trust companies sector exhibiting robust growth while YTL Power in the utility sector benefited from a strong uptick in demand.

The aviation sector saw better operating performance and a return to profitability, while the gaming sector, led by the leisure and hospitality sector, saw a revival based on stronger performance from companies like Genting.

Drop in nominal GDP

In the 1Q23 period, the Malaysian economy showed further strength as the economy expanded by 5.6% year-on-year (y-o-y), flatly beating market expectations of a 4.8% y-o-y growth.

Interestingly, the quarterly trend also improved as the 1Q23 gross domestic product growth of 0.9% on a q-o-q seasonal-adjusted basis was a reversal from the preceding quarter when the economy contracted by 1.7% on a q-o-q basis.

In nominal terms, the Malaysian economy expanded by 5.1% y-o-y to hit RM444bil in the 1Q23 period, but when compared with the preceding quarter, the economy contracted by 5% q-o-q.

The positive economic momentum compared with a year ago was not matched by corporate Malaysia as earnings in the 1Q23 period declined by 2.5% on a y-o-y basis, while on a q-o-q basis, core earnings fell by 4.0%.

Ten-to-three

With a disappointing set of results, the ratio of companies’ earnings that surprised the market against those that were below expectations fell sharply as only 11.4% of companies reported earnings that were above expectations against 37.6% that were below consensus estimates.

In essence, for every 10 reported quarterly earnings, seven were below estimates, while three beat expectations.

This was weaker than the preceding 4Q22 reporting season when 28.6% of companies reported results that were above expectations and 28.2% that were below expectations.

Hence, the earnings disappointment ratio jumped to 3.31 times, against the preceding quarter’s 0.99 times.

Lower fair value

Following the 1Q results, there have been major adjustments to earnings estimates for 2023 as well as for 2024 growth expectations.

For 2023, from the earlier forecasted earnings growth of 8.7% at the end of the 4Q22 quarterly reporting period, the revised estimate now shows an earnings growth of just 3.9%, a 4.9 percentage point reduction.

Earnings for 2024 are now estimated to grow by 8.9% y-o-y from the earlier estimate of 6.5% growth, an increase of 2.4 percentage points, mainly due to the lower base effect from this year’s forecast following the cut in earnings estimates for 2023.

Index-wise, except for one broking firm, which left its year-end target unchanged at just under 1,500 points, eight broking firms downgraded their FBM KLCI’s fair value by between 50 points and 140 points.

This brought the FBM KLCI fair value to 1,517 points, down by 80 points or 5% from the previous forecast of 1,597 points.

Based on Thursday’s index close at just under 1,375 points, the market has an approximately 142 points or 10.4% upside to the consensus year-end target of 1,517 points.

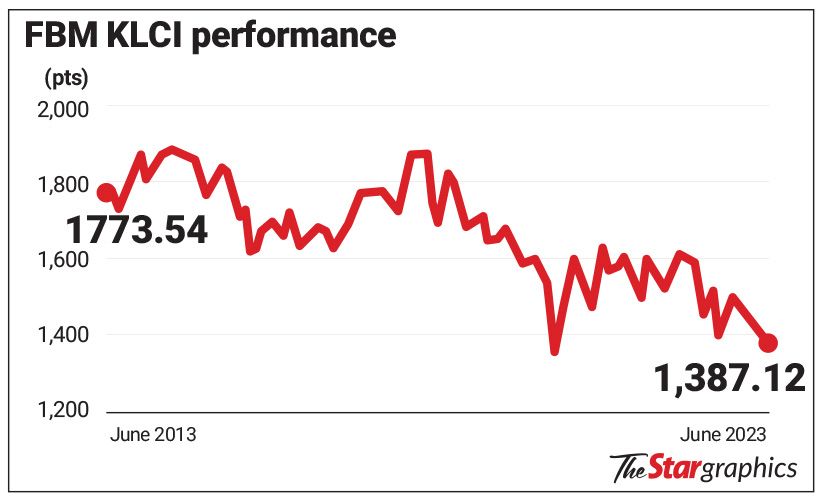

The unloved Bursa

Over the past decade, if one were to measure the performance of the local bourse by taking the FBM KLCI as a reference point, an investor will be likely very disappointed with the outcome.

The FBM KLCI ended last month at 1,387 points and fell further in the first five trading days in June and was last seen at just under 1,375 points on Thursday.

Over the past 10 years, the FBM KLCI has dropped almost 400 points or 22.5%, while measured against the peak of 1,893 points that was achieved in July 2014, the index is now trading 27.4% lower.

The local bourse has been an unloved market among foreign investors for a while now with foreign holding down to just 20% as at the end of May 2023 from as high as 25.2% exactly ten years ago.

Between 2013 and Thursday’s closing market data, foreigners have been net sellers in the market to the tune of RM65.9bil. Other than the 2013 net inflow of RM2.6bil and last year’s net inflow of RM4.4bil, foreigners have been net sellers in the market every year with an average net outflow of RM8.7bil a year between 2014 and 2021. Year-to-date, net foreign selling amounted to RM3.32bil and should the selling pressure persist, soon enough, we will likely see the foreign shareholding dipping below the 20% threshold.

Non-strategic interest at 6.3%

According to the Securities Commission’s Capital Market Stability Review 2022 report, as at the end of September 2022, foreign shareholding on the market stood at 20.6%, of which some 68.7% of that are those related to strategic interest, leaving behind non-strategic stakes or those that trade in the market at 31.3% of the total foreign shareholding.

In essence, this suggests that foreign shareholding on the local bourse is barely 6.5% as at the end of September last year. This figure may have dipped further to about 6.2% to 6.3% now as foreigners net sold another RM5.55bil between October last year and last Thursday’s close.

Rising political temperature

The immediate concern for the market will be the upcoming six state elections with expectations that these state elections will likely be held between the end of July to early August.

The current base case scenario is for the status quo to prevail but the opposition coalition of Perikatan Nasional (PN) is expected to make some inroads in states like Selangor, Negri Sembilan, and Penang.

PN is expected to maintain its stronghold in Kelantan, Terengganu, and Kedah. However, should the unity governments in Penang, Selangor or Negri Sembilan fall to PN, there could be re-jigging at the federal level and the two-third super-majority presently held may be subject to some major horse-trading exercise, involving one or more political parties switching alliance. The political risk of another change in government cannot be entirely ruled out should the state polls swing towards the opposition decisively.

It’s all about rates

Into the sixth month of 2023, the issue as to where inflation and interest rates are heading remains a concern for markets as inflation rates globally remain stubbornly sticky and elevated despite the numerous tightening measures deployed by most, if not all central banks. The recent 25 basis points hike each by the Bank of Canada (BoC) and Reserve Bank of Australia (RBA) to 4.75% and 4.1% respectively basically suggest that the central banks are still concerned about inflation impact although some easing has occurred.

Although the US Federal Reserve may hold rates in its meeting scheduled for next week, there is still a probability that it may still raise rates in its July meeting. After all, minutes of the last meeting revealed that members of the Federal Open Market Committee (FOMC) remain divided if further rate hikes are necessary to cool down red-hot inflationary pressure as Core Personal Consumption Expenditure Index has remained elevated at between 4.6% and 4.7% for the past six months.

Locally, as confirmed by Bank Negara and as highlighted by this column before, the surprise 25 basis points hike in May was essentially a pre-emptive strike by the central bank to ensure it is ahead of the curve and not re-active should inflation pressure persist, especially in the second half of this year.

Nevertheless, the rate hike did little to help the ringgit to recover the lost ground, which is down 4.9% year-to-date. Among Asian currencies, other than the yen’s year-to-date decline of 6.3%, the ringgit’s weakness seems to be correlated to the yuan’s weakness, which has dropped 3.2% year-to-date.

With the FBM KLCI’s year-to-date decline of 8.1%, the local bourse is the worst-performing market among Asia-Pacific countries, not only in local currency terms, but also in dollar terms, as it is now down by 13% year-to-date.

In conclusion, given the poor 1Q23 earnings report card, the internal headwinds as far as the political climate is concerned, and external uncertainties with respect to rate hikes and the relative strength of the dollar vis-à-vis the ringgit, it looks like it will take a while before the market finds its footing, despite the relative attractiveness of the market, trading at a price-to-earnings ratio of just under 13.5 times for 2023.

Pankaj C Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.