MALAYSIA’s most unloved sector in recent times must surely be the glove sector as all the glove producers have seen the share prices of their companies plummet to levels not seen in years, and for some of them, at less than half the value they were trading at before the outbreak of the Covid-19 pandemic.

This column had written about the glove sector twice, “THKS – The (G)Love Story” (Starbiz, July 18, 2020), just as the pandemic had emerged and share prices of the glove sector were going to the moon, and the second article, “Valuation is an Art” (Starbiz, March 13, 2021), just as share prices were beginning to correct and as analysts were then quick to adjust earnings expectations.

The writing was on the wall

As the pandemic resulted in a significant jump in demand, glovemakers were the darlings of Bursa Malaysia two years ago as share prices of these companies skyrocketed to unimaginable levels with Top Glove Corp, Hartalega Holdings, Kossan Rubber Industries, and Supermax Corp leading the way.

The stars were all aligned for the glovemakers as average selling price (ASP) surged on rising demand.

Higher demand also meant that glovemakers were set to realise an increase in earnings by multiple folds as operating profits surged to as high as 70%.

The rise in profits not only invited newbies to the market but established market players also set in motion plans to expand their respective glove production capacity with some seen even planning to double theirs.

While Malaysian glovemakers are dominant internationally, the super margins also saw the emergence of Chinese manufacturers in a big way.

As the pandemic subsided with the rise in the number of people vaccinated, demand for gloves too fell off the cliff.

Just like any other commodity, ASPs started to fall and prices are not only back to the levels seen pre-pandemic level but now are seen headed even lower than before the pandemic.

The glove industry is now suffering due to multiple reasons other than the issue related to global supply exceeding demand.

Firstly, end-buyers have a significant level of stock and thus negating any pick-up in demand despite the new Covid-19 waves or even the emergence of monkeypox.

Second, market players are sitting on an idle capacity to the extent some glove producers are only running at half or at best at about 60% capacity.

The issue of labour shortages is also plaguing the industry while the minimum wage cost has increased total operating costs. Even utility cost has increased due to the higher tariff for gas and water.

Before the pandemic, glovemakers were able to pass on these additional costs to buyers but due to the oversupply situation of the market, the flexibility to raise prices has been diminished and hence margin erosion has kicked-in.

Looking back, and as this column has highlighted before, the glovemakers are producing a commodity where the law of demand and supply will dictate ASP and margins.

But post-pandemic and into the endemic stage, the glovemakers have turned from being price makers to price takers – whereby they have lost their pricing power due to an abundance of supply and are no longer able to influence the market.

Exiting the FBM KLCI

Hartalega was the first glovemaker to be included in the prestigious 30-stock KLCI index in the June 2018 semi-annual review when its market capitalisation then hit RM20.5bil.

Top Glove followed suit six months later when its market capitalization hit RM15.6bil in the December 2018 semi-annual review.

The rally among glove stocks was indeed phenomenal in 2020 as Supermax became the third glove company to be added to the FBM KLCI when its market capitalisation hit just above RM20bil in December 2020.

However, Supermax’s entry was short-lived as, by the time the next semi-annual review was carried out in June 2021, Supermax’s market capitalisation has already dropped to well below RM10bil and was booted out.

This was due to MR DIY Group’s auto-inclusion, which was then ranked above the 25th position based on the full market capitalisation ranking of the 30-stock index.

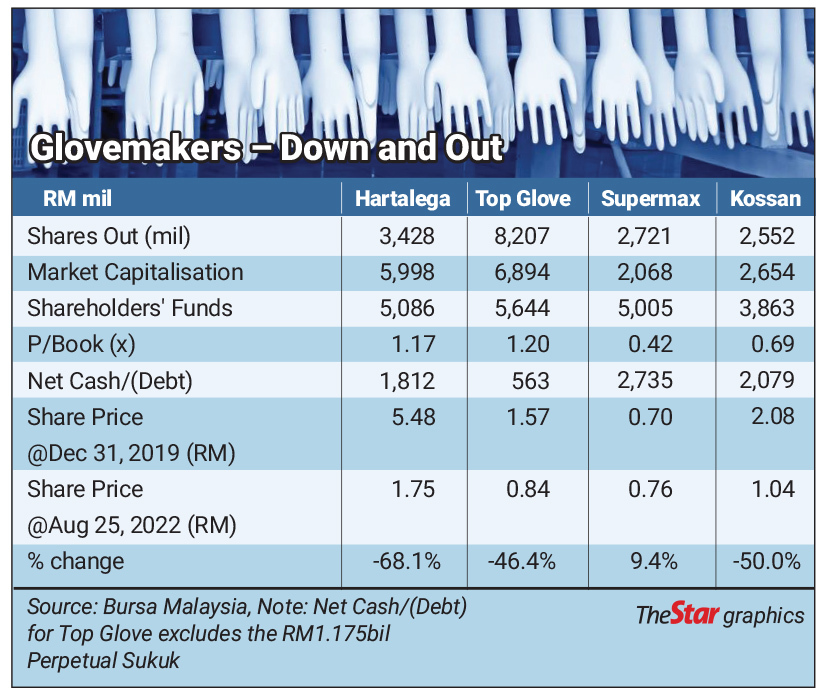

Both Hartalega and Top Glove has been under intense selling pressure over the past year, mostly on disappointing earnings as well as a bleak outlook. The table provides a snapshot of the top four glovemakers and their respective key financials and market statistics.

and Top Glove has been under intense selling pressure over the past year, mostly on disappointing earnings as well as a bleak outlook. The table provides a snapshot of the top four glovemakers and their respective key financials and market statistics.

Glovemakers – down and out

As Top Glove and Hartalega have a market capitalisation of RM6.9bil and RM6.0bil respectively as of Thursday’s close, both of them will likely be booted out at the next semi-annual review date on Nov 21, 2022.

This is based on the fact that both the glovemakers are ranked well below the 35th ranked constituent of the FBM KLCI, which is the cut-off position to remain in the prestigious index.

FBM KLCI loses 57 points

When Supermax was removed from the FBM KLCI, the net impact on the index was that it took away some RM8.4bil in full market capitalisation of the KLCI itself and this translated to about 16.5 index points on the FBM KLCI, after taking into consideration the free-float factor.

Now, both Hartalega and Top Glove are about to do the same and the net impact is that some RM23.3bil in total market capitalisation of the FBM KLCI will be lost as this is approximately 40.5 index points between the time of entry into the index and exit out of it.

In essence, the FBM KLCI itself loss 57 index points due to the drop in the three glove companies’ market capitalisation between the time of entry and exit in the FBM KLCI.

Taking it private

Interestingly, all four glovemakers are rags to riches stories of the men behind the companies and continue to hold significant ownership of their listed entities.

The table also provides the current price-to-book value of the four glovemakers with only Hartalega and Top Glove still trading above their respective book values while Kossan Rubber and Supermax, at 0.42 times and 0.67 times, are prime candidates for the companies to be taken private.

Interestingly, the cash per share of Supermax at RM1.01 is 32.3% higher than its market price, making it an ideal candidate for a potential Selective Capital Reduction (SCR) exercise.

The owners of Supermax, which have a combined stake of 38.4%, would only need to use some RM1.27bil of the company’s cash to take the company private under the SCR route based on its current share price.

Of course, the minority shareholders will not accept the current share price as a fair and reasonable price under the SCR rule and a more palatable price to them would be closer to the net asset value of the company.

However, that will likely drain all the net cash that is available in the company as an SCR at RM1.82 per share will cost the company some RM3.05bil, which is more than the company’s net cash of RM2.73bil.

Hence, a more reasonable SCR price would be the mid-point between the share price and the net asset value, which is at RM1.29 per share or an almost 70% premium over its current share price of RM0.76 per share.

This will cost Supermax some RM2.16bil, leaving the company with some RM572mil in cash after the exercise.

As for Kossan, an SCR exercise for the remaining 51.2% shares not already owned will cost the company RM1.36bil based on the current market price and thus leave the company with some RM721mil in the kitty.

However, similar to Supermax, Kossan probably would need to raise the price for a potential SCR to between the current market price and its net asset value of RM1.51 per share.

At the mid-point, a fair SCR price is at about RM1.28 and this translates to about RM1.68bil in total cash outlay. Under this scenario, Kossan will be left with some RM395mil in cash after the exercise.

In conclusion, the pandemic has brought newfound wealth to the shareholders of the glovemakers.

Some were generous with aggressive share buy-back programmes as well as huge dividend payouts while minority shareholders made huge capital gains from the rally that peaked in 2020, provided they exited at the right time.

However, for companies that were neither aggressive in buy-back programmes nor engaged in huge dividend payouts, the cash left in the company today provides an opportunity for the owners to take the companies private via the SCR route.

Pankaj C Kumar is a long-time investment analyst. The views expressed here are the writer’s own.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.