IT is not all doom and gloom for some sectors on Bursa Malaysia that have to deal with the weak ringgit and sluggish economy.

Several sectors have shrugged off such concerns such as the glovemakers and semiconductor players. Another such sector on Bursa Malaysia that has been sailing through the current choppy period is the plastic and packaging makers.

Maybank IB Research says in a report that the manufacturing-based exports continue to record robust double-digit growth of 16.1% year-on-year despite external economic headwinds.

In the past, plastics and packaging companies had been under the investors’ radar because of low margins and subdued growth momentum.

But thanks to the weaker ringgit and lower oil prices, the sector has come back to life, especially for the small-to-mid cap stocks.

Counters in this sector have received a lot of attention this week with their share prices spiking to new highs, which in turn pushing up the sector’s price-earnings multiple.

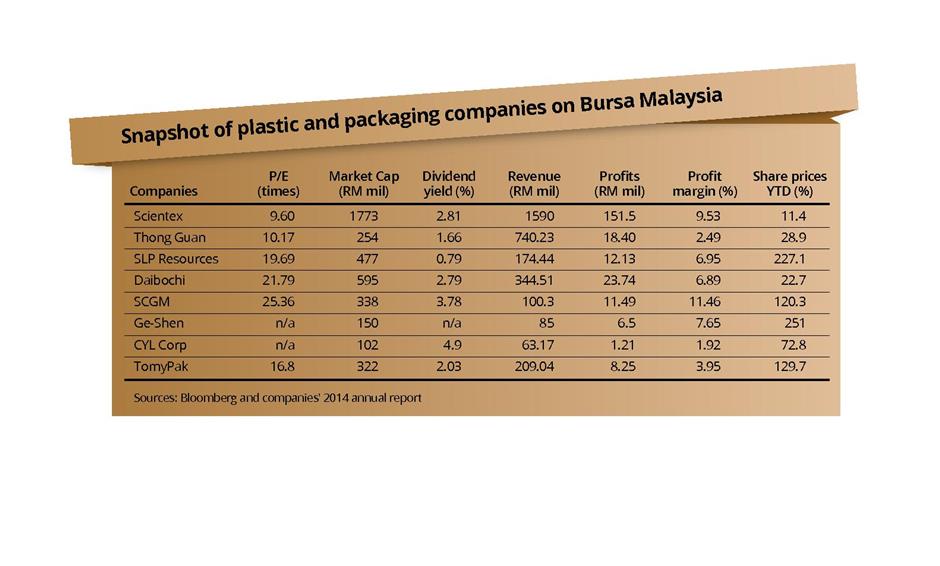

Year-to-date, shares in companies such as Scientex Bhd , SLP Resources Bhd as well as Daibochi Plastic and Packaging Industry Bhd have soared 11.42%, 227% and 22.7% respectively. Since early October, these counters have seen their share prices rising, as much as 6% for Scientex and 17% for SLP and Daibochi.

, SLP Resources Bhd as well as Daibochi Plastic and Packaging Industry Bhd have soared 11.42%, 227% and 22.7% respectively. Since early October, these counters have seen their share prices rising, as much as 6% for Scientex and 17% for SLP and Daibochi.

Daibochi and SLP are both heavily involved in consumer-related packaging industry that demand higher valuation than the companies that are heavily engaged with industry-related packaging such as Scientex and Thong Guan Industries Bhd, analysts say.

Daibochi is trading at 21.7 times forward earnings, SLP at 19.67 times, Scientex 9.6 times and Daibochi 22.79 times.

“The consumer packaging sector has higher margins compared with the industry packaging business because they provide more value-added services such as printing,” an analyst says.

Kenanga Research analyst Voon Yee Ping tells StarBizWeek the average price-earnings (PE) ratio valuation for the industry packaging sector would be between nine and 10 times, while for the consumer packaging sector about 15 and 16 times.

She says that among the companies in the plastic and packaging industry covered by Kenanga, SLP has experienced the biggest margin improvement for its second and third quarter of the financial year ending December 31, 2015.

For the third quarter ended Sept 30, SLP recorded a net profit of RM9.4mil on the back of RM42.7mil revenue. The profit margin is generally about 22% compared with 9% recorded in the same quarter last year.

“The strengthening in the US dollar, the depressed oil prices and oversupply of global resin have resulted in cheaper raw material cost, which have boosted the margins of the plastic and packaging players,” she says.

She, however, reckons that SLP’s share price is now fairly valued due to the recent rally and has rated it as “market perform” with a target 2016 PE of 16 times.

Meanwhile, analysts is not so excited about Daibochi. CIMB Research has given a “reduce” call on the counter because of the lofty valuations.

“Although raw material prices were stable in the third quarter compared with second quarter this year, the company’s earnings before interest, taxes, depreciation and amortisation for the third quarter dipped compared to the second quarter of 2015.

“We believe this was mainly due to lower economies of scale as a result of weak third-quarter 2015 revenue numbers,” it says in a report.

It reckons that Daibochi will need to boost its quarterly revenue to above RM90mil level, moving forward.

“Potential de-rating catalysts include expensive stock valuations and weak domestic demand market,” it says.

The other plastic and packaging players with lower market capitalisation are also trading at their record high ever after being relatively quite and trading at single digit previously.

Companies such as Ge-Shen Corp Bhd, Tomypak Holdings Bhd, SCGM Bhd and CYL Corp Bhd have seen their share prices spike about 250%, 131%, 120%, 73% year-to-date respectively.

Interestingly, after Ge-Shen received a takeover offer back in August, the share prices of other plastic and packaging players also went up.

Shareholders of Ge-Shen received an offer of 81 sen a share. But after the takeover attempt failed, shares in Ge-Shen skyrocketed to close at RM1.96 yesterday.

Surprisingly, CYL Corp, which has the smallest market capitalisation among the plastic and packaging players, offers a generous dividend.

According to data by Bloomberg, CYL Corp is offering a dividend yield of 5.35%.

So what will fuel the growth and what are the key challenges for this plastic and packaging industry to ensure they continue with their growth momentum?

Voon says that the players in this sector will continue to record good earnings and margins, as the sector is one of the beneficiaries of stronger US dollar and lower raw material prices. The weaker ringgit has boosted demand for Malaysian products as well and that has helped the sector.

She reckons resin cost will decline going forward due to excess resin supply in the market because China has increased its resin production capacity to support local demand, causing excess supply outside China.

“We expect this lower cost environment to persist well into 2016.

“We have accounted for lower resin prices for all plastic packagers under our coverage, although margins could continue to surprise on the upside should the resin oversupply situation worsen,” she says.

Voon says that players in the plastic and packaging industry have also been expanding their capacity to ensure growth sustainability, going forward.

She has “underperform” call on Scientex, “market perform” on SLP and “outperform” rating on Thong Guan.

She explains that Thong Guan is targeting to add a new production line in the fourth quarter that would increase 25% of its capacity for Purewrap product and expand its sales team, resulting in stronger earnings contribution from financial year 2016 onwards.

“We maintain our positive view on Thong Guan’s long-term outlook due to its continued capacity expansion into high-margin product lines, well-received 6-micron pre-stretch product especially in South Africa and Australia, and successful restructuring of its China operations, as indicated from its turnaround in the third quarter,” she says.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.