Thematic plays come and go but management stays

PHILLIP Capital Management Sdn Bhd chief investment officer Ang Kok Heng readily admits that spotting thematic plays aren’t his strengths and he still believes in a bottoms up approach when picking stocks.

“Thematic plays isn’t something we really focus on. They come and they go. For now, the export-based companies are doing well because of the weak ringgit. But once the ringgit starts to strengthen, that play will be over. This is the same for plantations, oil and gas and tech. What is here to stay though, is the management of the company. That’s what we pay a lot of attention to,” says Ang.

Ang is no stranger in the fund management world.

While some recognise him for his ability to identify growth stocks, his credibility was built simply because he could averagely give a constant return of 10% per annum. He has made a name for himself simply by delivering results.

“I knew he was okay when my friend told me that he gave Ang some money to manage, and he delivered more than 10% return a year over an 11-year period,” says an industry observer

It is no secret that many brokers peddle their stock ideas to Ang in the hope that his buy-in into the stock will translate into a stamp of approval, and thus attract a lot more interest from other investors.

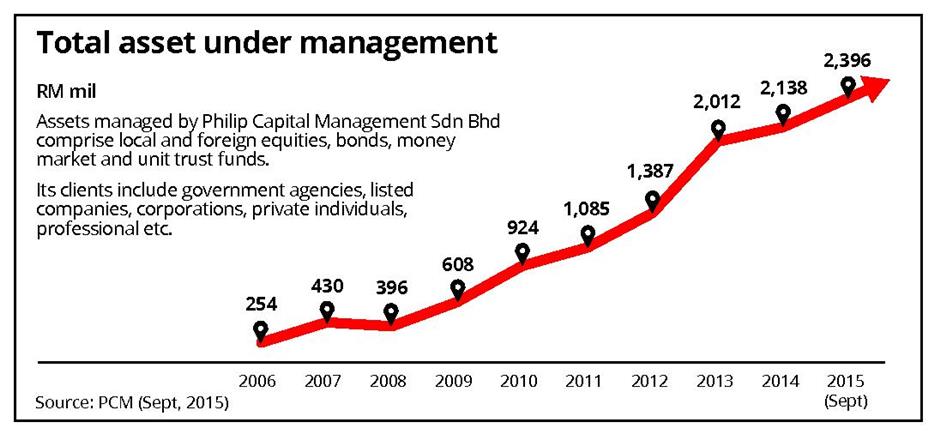

“Yes, I know there are people who track what we buy and what we like,” laughs the soft-spoken Ang who currently oversees some RM2.3bil over 10,000 accounts.

A third of the funds comes from the Employees Provident Fund. The bulk of the funds though are individual accounts. Ang diversifies his holdings and currently holds a mixture of 30 big cap and small stocks for his various funds.

He is currently 65%-70% invested in the market. He feels there isn’t a need to always be fully invested in the market as opportunities come when there is volatility.

Over the last eight years, Ang has delivered an average annual return of 8.4%.

When prodded what his “secret” or “trademark” is that has yielded some level of reverance in the industry, Ang is obviously uncomfortable with self gratification.

“I think investors know that we are hands on. We are in this business because of our passion for the financial markets,” says Ang, a mechanical engineering graduate from the University of Malaya. He also holds a Master Degree in Business Administration from Universiti Kebangsaan Malaysia.

Ang feels that he has an added advantage having worked in the Malaysian Investment Development Authority (Mida), formerly known as Malaysian Industrial Investment Authority, between 1980 to 1986. This was where he got his first taste of the investing scene.

The six years in Mida exposed Ang to the many different industries and businesses. He was in the licensing department where he analysed new projects and assessed whether they were deemed fit for approvals.

This experience gave him an immense advantage and thus when he joined TA Securities Bhd in 1988, he was immediately made head of research in the equity research department. He headed the department for seven years before being appointed as the chief investment officer of TA Asset Management in 1995.

Ang joined Phillip Capital Management Sdn Bhd in January 2007.

Below are excerpts of the interview with Ang Kok Heng:

On the stock market

Why do people lose money in the stock market?

When one fails to make money from investing in the stock market, he or she may doubt that the stock market is the right place to invest. If the stock market always provides higher return as claimed by many investment gurus, why do investors lose money from time to time?

One of the many things I have learned from our chairman of Phillip Capital Group in Singapore is that when something fails, it is either due to Type 1 error – not the right thing to do, or a Type 2 error – the task is right but was not executed correctly.

Based on our past experience, we know that the stock market is still one of the best places to grow wealth. We need to constantly improve our strategy to minimise losses in order to reduce the Type 2 error.

What are the things you look out for when investing?

While it is important the company doesn’t take on too much debt, what is more important is the company’s ability to generate cashflow to service its loans.

Debt can be necessary for growth, especially when interest rates are low. With the current environment of low interest rates, companies should be borrowing. If they aren’t borrowing, I don’t think they are maximising shareholder value.

We also like business models that comprise high margins or high recurring incomes.

The profit margins can be high either on a relative or absolute return. For example, if a certain sector generally commands margins of 10%, and a particular company generates 15%, then this is good. Tune Insurance Malaysia Bhd is one example of a company which commands high margins.

While it would be good to find a stock with a low price earnings ratio, sometimes that is not always the case.

A recent stock we bought into was MyEG Services Bhd . While valuations aren’t exactly cheap (at about 51 times price earnings ratio), there is a lot more upside in the company especially with its project to register migrant workers in the country. This will enable them to diversify into other businesses such as selling insurance and SIM cards.

. While valuations aren’t exactly cheap (at about 51 times price earnings ratio), there is a lot more upside in the company especially with its project to register migrant workers in the country. This will enable them to diversify into other businesses such as selling insurance and SIM cards.

How important is management?

That is probably the most important thing to watch out for. Management must have integrity, be focused and hands-on in the business. It also needs to take care of shareholders. Many companies have management that is just a caretaker.

What about red flags?

Companies that are not making money or if their profits have been flat for years and margins are very thin. When margins are very thin, their risk of posting losses is higher. A company’s market capitalisation is not really an issue as most growth stocks are typically the small to mid cap stocks.

How long do you typically hold on a stock?

Averagely when we invest in a stock, it could be between 9 and 15 months. We have bought into TSH Resources Bhd and QL Resources Bhd in 2008 and are still holding till today.

In TSH’s case, this plantation company is planting new trees every year, and hence earnings and output continue to grow.

When we bought into QL in 2008, it was trading at PE of 10 times, and management had said it was looking to grow 20% every year. While QL’s growth today is not like how it used to be, it has a diversified business base with steady earnings.

On rates and oil prices

Do you foresee the Fed raising interest rates in December?

Whether or not the Fed increases interest rates, this is already priced into the market. The market is more worried about something that is out of expectation. The Fed hike is already expected by the market.

There is no hurry for the Fed to raise interest rates especially when inflation rates are low. This is more so with the low oil prices. However, the US will eventually need to increase rates as its been capped to low and too long. Hopefully the rise will be gradual and mild.

Oil prices

I think the price will range between US$40 and US$60 over the next few years. I think the worst has yet to come for some of our Malaysian service support companies. With contract prices and charter rates among others being slashed, earnings of some of the companies are going to get hit.

On the ringgit

Has the ringgit reached its tipping point?

The sharp fall in the ringgit (close to 20%) is impacting Malaysians. Many people have become fearful and some have started to unload their investments. Comparing with the previous crises, I find that the present currency crisis has little impact on our economy.

I think the Malaysian economy is doing quite well. Growth is not strong, but we are also not in a recession. While our ringgit is down some 20%, the stock market is down less than that, only about 8%. I feel the ringgit is oversold, and the worse is probably over.

For example, during the Asian financial crisis, our stock market plunged while the economy suffered for more than two years of severe recession. At the same time, the ringgit plummeted by 46%, causing many corporations to default on their US dollar loans and subsequently triggered a default on local banks loans.

Then during the 2008 Lehman Brothers crisis, our economy also fell into recession for nearly a year with the GDP contracting by 5.7%. Consequently, the FBM KLCI nosedived by 42% while the ringgit only declined by 12% against the ringgit. So as for the present crisis which was triggered by the collapse in oil prices, our economy continues to perform well. Our exports remain strong, the current account stays in surplus, banks continue to lend and the economic fundamentals remain intact. The economy is expected to grow at 4.5% to 5.5% despite the 8% fall in the FBM KLCI as at end-September.

Overall, the devaluation of the ringgit has forced the foreign funds to sell their shares and bonds which consequently caused the ringgit to fall further. Overall, the local bourse has corrected, but not as much as our neighbouring countries.

Despite the weaker ringgit, there is no sign of recessions. Investors should not be overly concerned with the current market weakness as it will recover as soon as the ringgit stabilises.

Why did the ringgit fall so much?

The sharper than expected drop in the ringgit is likely to be caused by speculators who are taking advantage of the domestic political uncertainties and the fear of default by 1MDB, forcing down the ringgit in order to make short gains. Malaysia’s second quarter gross domestic product grew by a strong 4.9%, so actually the ringgit should not have declined more than other commodity-based currencies.

Furthermore, foreigners do not view Malaysia as a high risk country. There is no sudden change in the ruling party neither are we taken over by the military.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.