FORTUNES for auto players operating within the supply chain of the industry could take a turn for the better should the National Automotive Policy 2014 (NAP2014) take off as intended.

A recent statement by the International Trade and Industry Minister Datuk Seri Mustapa Mohamed largely went unnoticed by the market but a possible award of four more licences for the production of energy efficient vehicles (EEVs) in the country may breathe new life for these intra-supply chain operators.

Indeed, the status quo today shows that most of these companies are now operating in a challenging industry environment judging from latest statements released by Perusahaan Otomobil Kedua Sdn Bhd (Perodua) which recently lowered its sales target for the year.

Perodua said it reduced its target to 193,000 units from 197,000 units on intense competition and tightening of the country’s financing guidelines.

‘Overweight’ call

In a client report last week, AmResearch said that it was reviewing its “overweight” call on the sector via the bottom-up approach.

“There is developing risk in the sector of demand moderation given recent macro policy developments and uncertainties on disposable income created by the GST (goods and services tax),” AmResearch’s auto analyst Hafriz writes in his report.

“However, we are still quite bullish on the auto parts sector. More completely knocked down (CKD) licences are good as they will source for auto parts from within Malaysia,” Hafriz says when contacted by StarBizWeek.

Hong Leong Investment Bank’s auto analyst Daniel Wong says that sentiment towards buying vehicles will most likely impact demand for A-segment cars as they cater most to the lower income group that are the most sensitive to any increase in the cost of living.

CKD licences

“Any move to grant further CKD licences will be positive for auto parts manufacturers, although Bank Negara’s move to raise interest rates is a more concerning issue for now. We will know in the next monetary policy committee meeting if there will be any further rate rise,” Wong says.

TA Research’s auto analyst Angeline Chin says that the impact from the recent interest rate will not be that pronounced for the higher priced C-segment cars and above and notes that there are still not much changes to total industry volume forecasts now.

TA’s Chin says that while the introduction of new CKD licences is positive, there is the possibility that the new EEV car makers in Malaysia would insist on more competitive pricing for their components. This in turn she says would impact the component makers margins. But she adds, “Those who are able to derive economy of scale benefits would do well”.

Another analyst reckons that car manufacturers may instead of seeking lower prices for components, would require the value additions to these products. “The car manufacturers are under competitive pressure so they may opt to deliver products with more features and require the component suppliers to deliver on that, without necessary asking for lower prices on the components,” the analyst explains.

Key auto component

Auto component companies have seen their shares at subdued levels due to what analysts put down as margin pressures stemming from car makers themselves looking to price their products more competitively.

The component manufacturers generally trade at a discount to the broader market and FTSE Bursa Malaysia KL Composite Index. Indeed investors have been cautious toward the sector as the latest regulatory bank lending guidelines and the move to gradually raise interest rates have put a dampener on sales expectations.

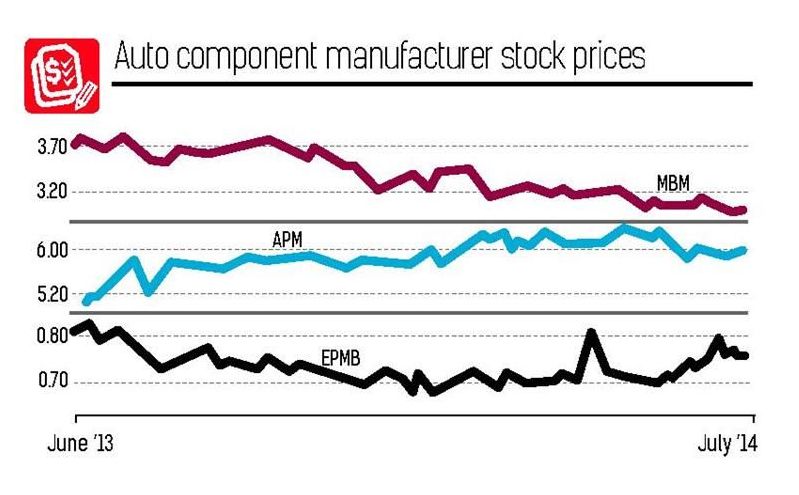

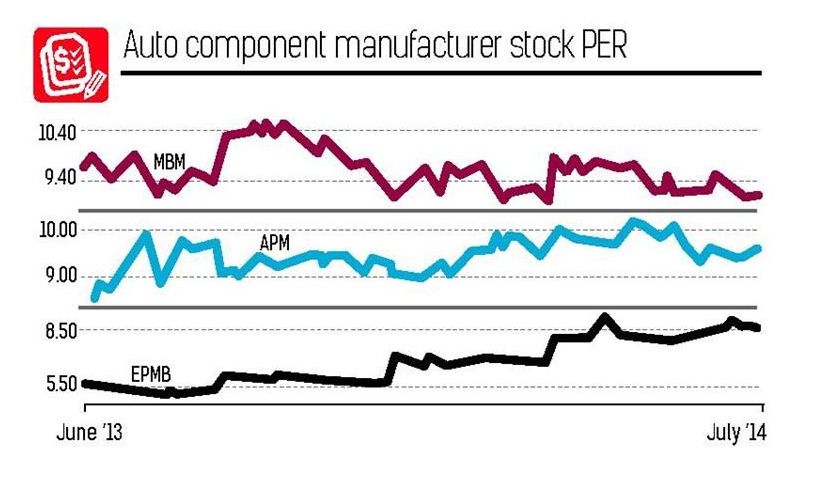

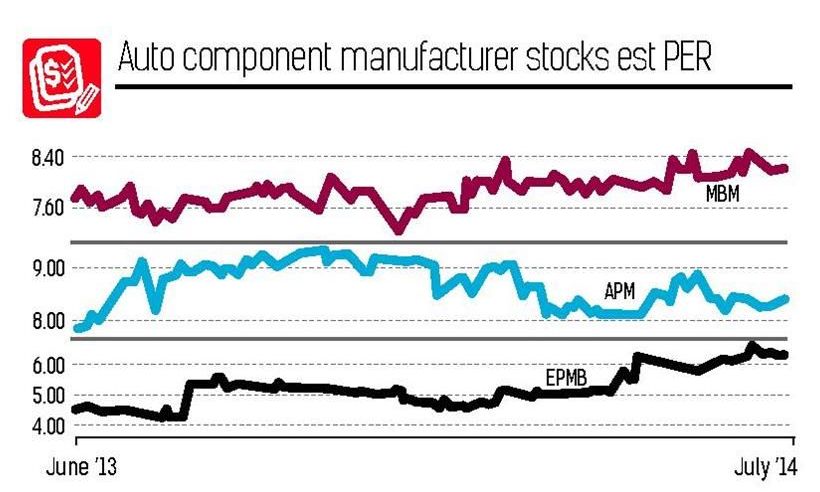

It is notable that key auto component manufacturers such as APM Automotive Bhd, MBM Resources Bhd and EP Manufacturing Bhd (EPMB) have seen their trailing and forward price to earnings ratio (PER) hovering at single digit levels for the most part of the year. (see charts)

Bhd, MBM Resources Bhd and EP Manufacturing Bhd (EPMB) have seen their trailing and forward price to earnings ratio (PER) hovering at single digit levels for the most part of the year. (see charts)

An analyst said that these stocks are now hovering at “palatable valuations” and they may suit those who have been harping on the excessively high valuations on the broader market but also noted that their prospects had been crimped by rising interest rates.

APM is presently trading at 9.6 times PER (price-earnings ratio), MBM at 9.1 times PER and EPMB at 8.66 times PER.

The bigger car manufacturers are however trading at higher valuations, closely following the benchmark FTSE KLCI with Berjaya Auto Bhd (14.23 PER, 5.81 price to book ratio (PBR)), Tan Chong Motor Holdings Bhd (17.2 PER, 1.3 PBR), UMW Holdings Bhd (19.5 PER, 2.12 PBR) and DRB Hicom Bhd (9.52 PER, 0.60 PBR).

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.