MEENA, a 55-year-old accountant, is already looking forward to her retirement. With health issues such as backpain and arthritis, work has become physically challenging.

The only reason that keeps her working are the loans she pays on her house and car.

By the age of 60, Meena expects to retire with adequate retirement savings, a luxury 97% of working Malaysians covered under the Employees Provident Fund (EPF) cannot afford.

Latest data from the EPF shows that 6.1 million EPF contributors, 72% of them being bumiputra, have less than RM10,000 in their accounts.

This compares starkly to the EPF basic savings of RM240,000, which is the minimum amount considered sufficient to support members’ basic needs for 20 years upon retirement.

Many working Malaysians will need to play catch up but the question is, how many of them would achieve the required basic savings by the age of 55?

The EPF estimates that members will need to work between an extra four to six years to rebuild the savings that have been utilised during the pandemic.

Without working longer or having sufficient pension support, many older Malaysians would easily fall into poverty in just a few years post-retirement.

After all, Malaysians on average are living about 16 years longer after the retirement age of 60.

The World Bank calls for the country’s minimum retirement age to be increased to 65.

World Bank economist Amanina Abdur Rahman suggests that the transition to a minimum age of 65 could happen over a period of 10 years.

This means the retirement age is to be increased by about six months every year.

“After the minimum retirement age reaches 65, it could then be linked to life expectancy.”

By increasing the retirement age to 65 between 2020 to 2040, Amanina says Malaysia’s annual economic growth is expected to increase by 0.3 percentage points per year.

At a practical level, Amanina says that some jobs are more suitable to be performed by older workers than others.

“Age-management strategies, including adjustments to the work organisation, work equipment and working time policies as well as training can help to improve the suitability of jobs with the capabilities of older persons, and potentially also enhance their productivity,” she says.

Other experts who spoke to StarBizWeek also generally agree with the idea of extending the retirement age, even up to 70 years old.

The Malaysian Employers Federation (MEF), however, disagrees. It says working above the age of 60 should be on a voluntary basis, without raising the mandatory retirement age.

According to MEF president Datuk Dr Syed Hussain Syed Husman, employment beyond the age of 60 should be based on the health and performance of the employee, and if the employer still requires the services of the employee.

He says a blanket increase in retirement age would cause employers to face issues of increasing medical cost and lower productivity, especially among those employees in physical work such as the construction, plantation and manufacturing sectors.

“Employees themselves may be physically challenged to continue working in sectors that involve a lot of physical work,” he says.

Syed Hussain also warned that raising the retirement age could cause unemployment among the younger generation to increase.

“In July 2013, when the government increased the retirement age to 60 from 55, this led to the loss of about a million job opportunities for fresh graduates.

“The private sector would have about 200,000 retirees per year, hence in five years, at the material time about a million of them were retained up to July 2018,” he says.

Across Asean, the retirement age of 60 is rather common, although some countries are looking at raising the age limit.

Just earlier this month, an increasingly ageing Singapore announced that it will raise the retirement age to 63 from July 1, 2022, up from 62 currently. The public sector there already implemented it on July 1 this year.

Indonesia, on the other hand, plans to raise the age limit to 65 by 2043. For every three years, Indonesia will be increasing its retirement age by a year. The current retirement age is 57 years.

Malaysian Economic Association (MEA) president Prof Datuk Norma Mansor points out that many countries are indexing retirement age to life expectancy.

Malaysia could start by increasing its retirement age to 62, but it should be ensured that everyone is ready for the change, she says.

“The government introduced incentives for employers to hire post-retirees two years ago. It is a good start but some employers seem to be reluctant,” according to her.

A later retirement age will be good economically, Norma says, as it will help improve old-age dependency ratio.

“Less seniors rely on younger people aged between 15 to 59.

“Productivity will definitely increase and when the country is moving up the value chain, we will need the skills, knowledge and experience acquired by the baby boomers,” she adds.

EMIR Research head of social, law and human rights Jason Loh Seong Wei says it is timely to increase the mandatory retirement age.

“Increasing the retirement (and re-employment) age would enhance the self-sufficiency and sustainability of seniors in terms of financial independence and purchasing power.

“It can also allow for businesses that are run exclusively or mainly by seniors and set within self-contained townships catering for the age group,” according to him.

Given the diminishing savings of many EPF members, especially following the special withdrawal schemes of i-Sinar, i-Lestari and i-Citra, Loh says it is critical to extend the working age for further accumulation of contributions.

However, Malaysia University of Science and Technology (MUST) professor Geoffrey Williams says raising the retirement age is a “very weak option” from a standard Western perspective.

He also says it “lacks imagination” in solving the problem of income in old age.

“They don’t really work in the Malaysian case.

“If you earn an average salary of RM2,933 per month and you saved 24% of that in a pension, working an extra five years beyond retirement at 60 years old would add only RM235 per month extra in your pension at 65 years old,” he explains.

Nonetheless, Williams welcomes the idea of giving people the option to continue to work beyond 60 years old.

“Forcing people to work beyond 60 years of age, on the other hand, is not a solution in the Malaysian case where as many as 75% of the working age population have no pension savings and only 3% of EPF holders meet the target threshold savings for retirement,” he says.

Health a major concern

With more Malaysians identified with comorbidities, it is one’s wonder whether a later retirement age would create more health risks for senior citizens.

Health Minister Khairy Jamaluddin has called Malaysia an unhealthy nation, with one in every two people are obese and only one in 20 maintain healthy eating.

Consultant rheumatologist Prof Dr Sargunan Sockalingam of University Malaya Medical Centre says the country needs a retirement policy that incorporates ways to tackle the rising cases of cardiovascular diseases, diabetes and stroke, among others.

Sargunan says Malaysians should be allowed to work up to 70 years old, if they would like to.

“The concept of ageism where one thinks anyone above the age of 60 is not physically capable is a myth.

“A senior citizen can very well remain cognisant and provide for the community and economy.

“Some health issues such as muscle weakness can be addressed through regular exercise and proper diet. This would allow more individuals above the age of 60 to contribute productively,” he says.

Apart from health issues, another key concern is the ability of seniors to adapt to evolving market needs.

MEF’s Syed Hussain says employees above 60 years old may not be able to keep pace with the Industrial Revolution 4.0 and the digitalisation needs of today’s requirements.

“Technology is changing at a rapid rate and may favour the younger generation to master the new technology.”

Rather than extending the retirement age, Syed Hussain says the better approach is to adopt a re-employment policy for those above 60 years on a fixed-term contract basis, which would allow for more flexibility for both employees and employers.

World Bank’s Amanina says that working longer is actually beneficial to senior citizens, health wise.

“Working at older ages has also been found to be associated with a lower risk of cognitive decline, including with regard to memory and mental health, as well as with higher average physical functioning,” she adds.

Addressing post-retirement protection

As Malaysia is on track to becoming “aged” in less than 25 years, MEA’s Norma says it is timely to plan for a stronger and more comprehensive social protection system.

This includes enabling higher income through higher productivity or high value-added industries.

EMIR Research’s Loh calls for an agency to be set up either directly under the government or as a government-linked company or as a social enterprise to provide post-retirement age employment to seniors – with no maximum age limit.

In addition, the Entrepreneur Development and Cooperatives Ministry and SME Bank should develop schemes to nurture and help retirees to be entrepreneurs, he says.

Upon reaching retirement age, Loh also suggests that EPF payments are staggered in the form of monthly payments.

Currently, EPF members can withdraw their entire savings lump-sum at the age of 55, which is five years before retirement. In many cases, the amount withdrawn depletes within a few years.

“This should be complemented by an annuity scheme (made compulsory) which can also be run by the EPF, for example. The annuity scheme will take place concurrently with the EPF contributions.

“EMIR Research also calls for a universal basic pension (UBP) at the same time that is funded partly by general taxation and partly by special tax contributions,” suggests Loh.

Echoing a similar stance on the UBP, MUST’s Williams says it should be funded by direct government transfer and investment income from government funds.

To fund the UBP, he points out that the government can consolidate existing spending on the elderly, top it up with extra funds, increase higher-level income taxes and establish a new investment fund.

The government could also use privatisation proceeds to finance a UBP by introducing a responsible privatisation programme to add to a new government pension fund.

“Ideas to source funds for a new investment fund can be the National Trust Fund (KWAN) fund of RM20bil, RM90bil in existing unclaimed assets from the estates of people who passed away without dependents, income from windfall taxes and Petronas premia in times of high oil prices or many other sources.

“To provide a RM1,500 pension to a two-person household above 60 years old would cost around RM3.2bil for the bottom 10% (B10) income group, RM12.9bil for the B40 and RM16.2bil for the B50 on a very rough calculation,” he says.

Malaysia’s retirement system has been ranked third in Asia and 23rd globally under the 2021 Mercer CFA Institute Global Pension Index.

The country’s scores were well above the Asian average in each of the three sub-indices, namely, integrity, sustainability and adequacy.

However, the inadequacy of retirement savings is a growing concern in Malaysia, especially among homemakers and informal sector workers.

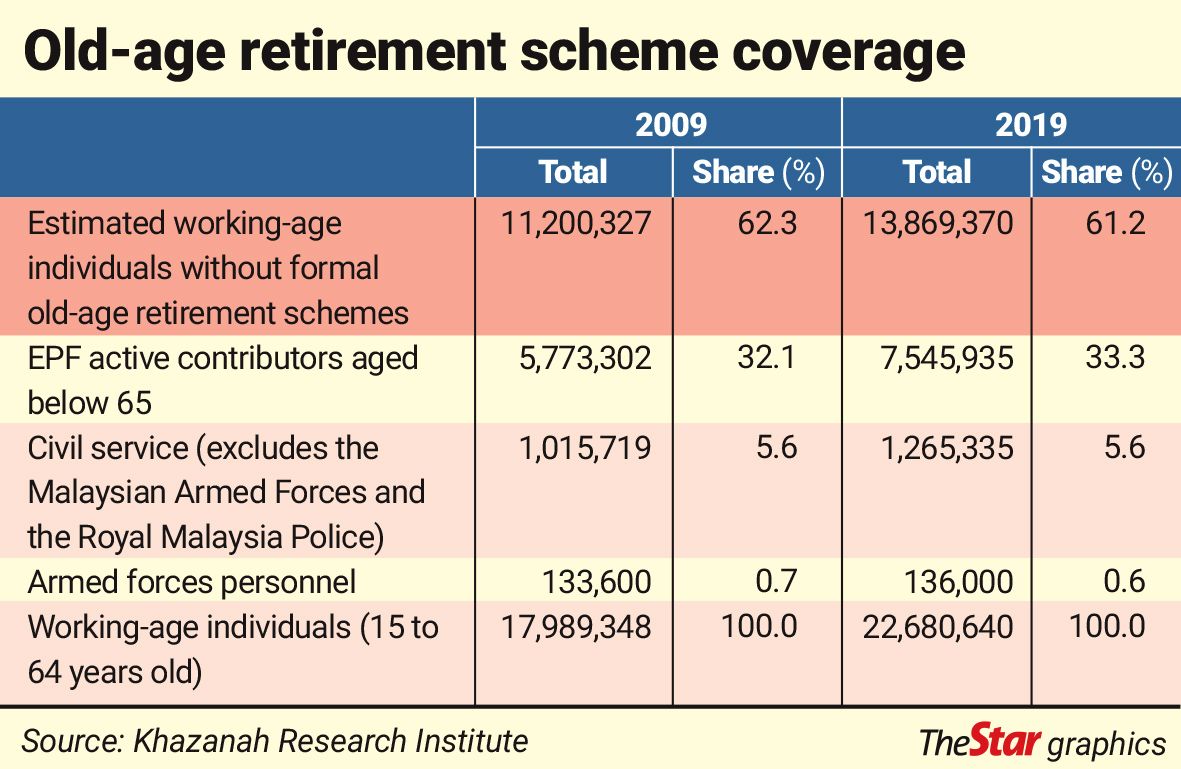

World Bank’s Amanina says that informally employed workers, including the self-employed, gig economy workers and workers in the agricultural sector, are largely uncovered by retirement savings schemes.

These individuals are, therefore, vulnerable to having low retirement savings.

“Increasing the coverage of the retirement schemes to cover these workers will, therefore, go a long way in terms of providing Malaysians with some form of retirement savings,” according to her.

According to the Allianz Pension Report – Asia Special 2021, Malaysia’s pension coverage for the population aged above 65 is only 18.6%.

In Singapore, the coverage is higher at 33.1%, while in Thailand and Vietnam, the coverage is 89.1% and 40.9%, respectively.

MEF was asked by StarBizWeek on whether employers should chip in more for EPF or a pension-like scheme, in order to remedy the low retirement savings.

In response, Syed Hussain believes the existing rates of employees’ and employers’ contributions to EPF are adequate.

“Employers are struggling to revive their businesses and generally would not be in a position to chip in more for the employees’ retirement savings.

“The EPF is a retirement savings and withdrawal should be allowed only when the contributor reaches the retirement age.

“If such a rule is implemented strictly, then the target that each contributor should at least have RM280,000 in the EPF account would be achieved,” he says.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.