PICTURE this scenario.You’re stepping outside your office for a drink at a cafe that you’ve been visiting for over a decade.After your drink, you walk up to pay.

But now, instead of giving the cashier cash like you’ve been doing all this while, you make your payment via your e-wallet, which is essentially an app residing in your mobile device that can be loaded with money and used to pay for goods and services.

And that’s not all. The same company responsible for supporting that e-payment is also the one lending you money to start your very own business and helping you facilitate cross-border remittances, bypassing all the red tape that traditional lenders have come to be associated with.

Welcome to the world where banking has a new face – and its technology.

In Malaysia, this exact scenario is not that far off.

“I’d say in 12 to 24 months’ time, this could be a very likely scenario,” says a keen industry observer.

At the moment, cashless payments still make up a relatively small portion of total payments in the country at about 20%, with only half of that comprising e-wallet transactions.

Even in neighbouring Singapore, a country perceived to be technologically sophisticated, cash remains the current choice when it comes to paying for stuff.

Over in countries like China, it’s been a slightly different story.

Probably the poster boy for the concept of an e-wallet society, China has been one of the earliest adopters of such a trend using mobile phones fitted with scannable quick response (QR) codes which facilitate such transactions.

In the world’s most populous country, even some beggars have started using QR codes to collect their alms.

Needless to say, it is now one of the world’s largest cashless marketplaces, with everyone from street vendors to posh malls having jumped on the bandwagon.

As of 2016, mobile payments in China stood at US$9 trillion, compared with US$112bil in the United States, according to reports. For the first 10 months of last year, it totalled some US$12.8 trillion.

Mobile phone services like WeChat and Alipay are enabling such transactions to take place, with Internet giants like Alibaba Group Holding Ltd and Tencent Holdings Ltd behind the entire ecosystem.

Analysts say part of the reason why cashless, specifically e-wallet payments have become so big in China is because the country is home to the highest number of mobile phone users in the world.

As the pioneers, Alibaba and Tencent are not contend with getting consumers, both in China and globally, to just use their e-wallet services.

Having made their payment apps global via partnerships with domestic payment networks and by buying stakes in local financial technology (fintech) firms, these two Internet giants now want to offer financial products and services like loans, money-market funds and other wealth-management products, not only to Chinese consumers but also to consumers worldwide.

In other words, they want to take over the role of traditional banks.

To be sure, they are already providing such services in China via their apps, Alipay and Tenpay.

This is possible partly because of their sheer consumer base size and balance sheet strength, which opens up many opportunities.

In the case of Alibaba, its affiliate Ant Financial has developed Alipay, which already has more than 500 million users worldwide, while Tencent’s Tenpay has about 400 million consumers.

Collectively, they control more than 90% of China’s US$5.5 trillion mobile payment market, Forbes reported, citing data from Beijing-based consultancy iResearch.

To consumers, tech firms seem an attractive financing option compared to traditional lenders, which often undertake long, stringent processes before disbursing their products. Notwithstanding a host of issues, often regulatory in nature, these tech firms are slowly but surely becoming a huge threat to lenders worldwide.

The local scene

Malaysia, much like the rest of the South-East Asian region, has been relatively slow in the high-tech payment game.

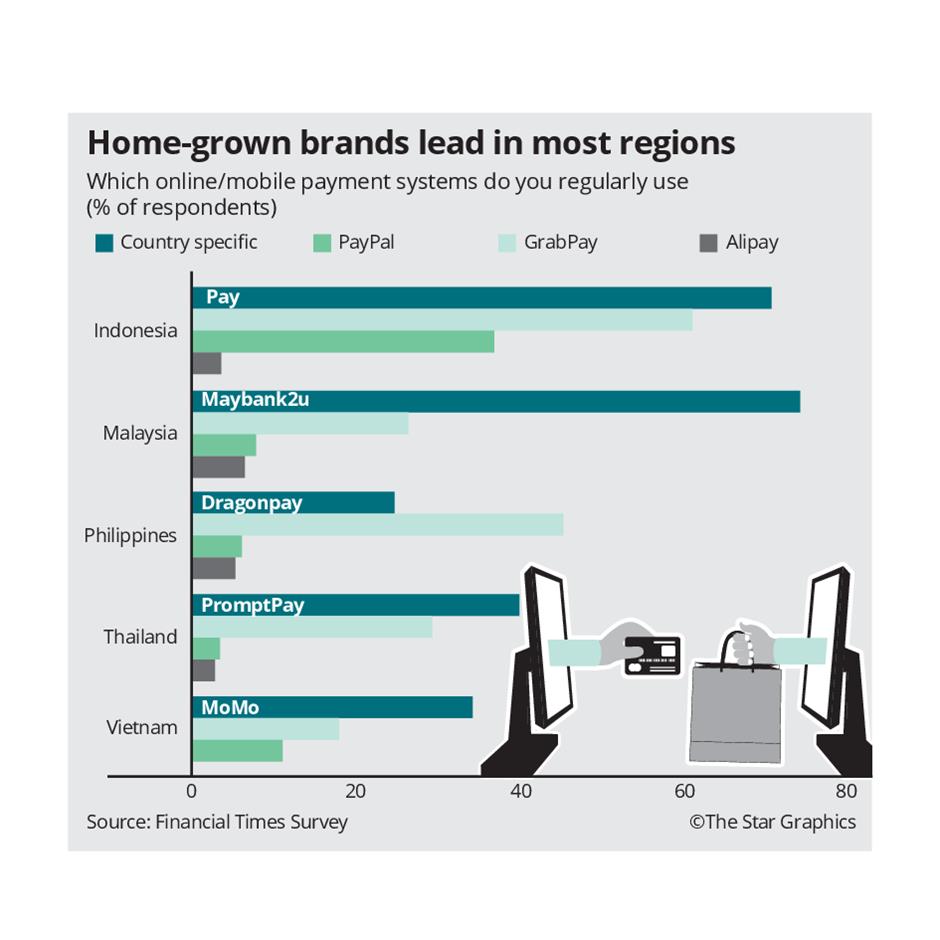

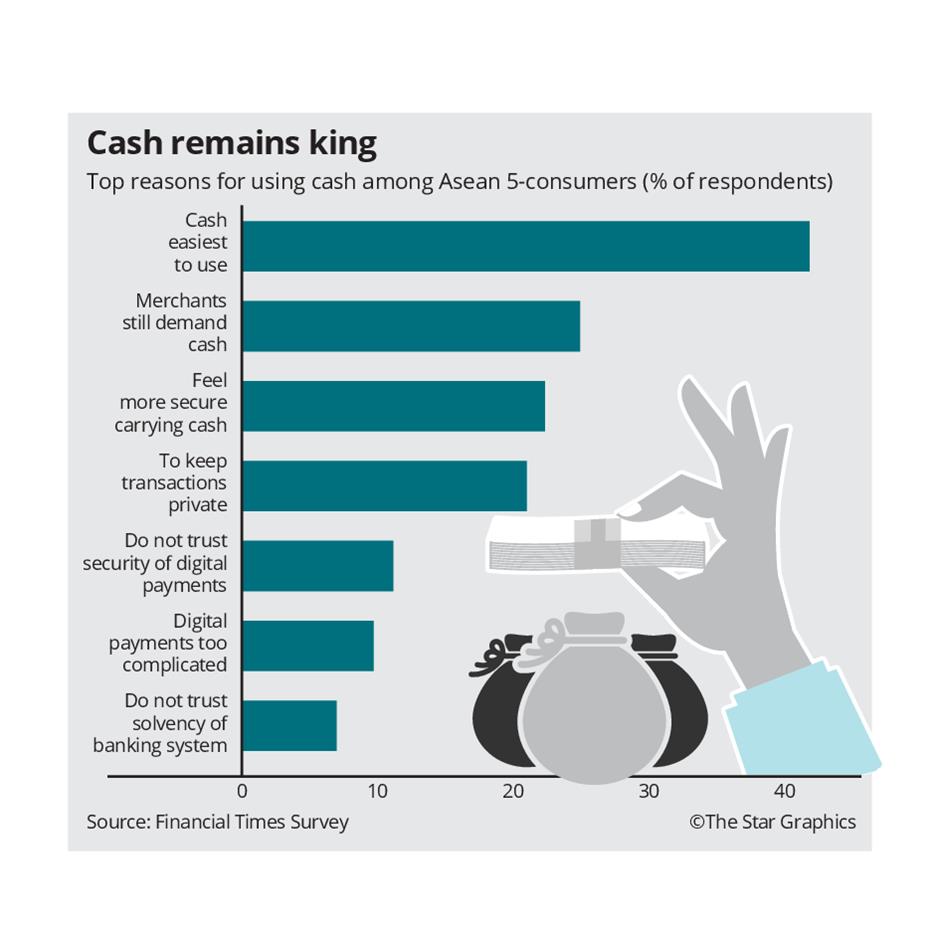

Consumers still prefer to use cash or bankcards in South-East Asia and banks here have had “limited success” when it comes to promoting a cashless revolution, according to a recent Financial Times article.

It blames this on technology rather than bank penetration, which is relatively high in countries like Malaysia and Singapore.

“For mobile payments to be successful, one needs a combination of factors, including interest and eagerness from customers to use mobile as a device to pay, a broad merchant network availability where customers can pay and network effect that can ensure a seamless user experience,” says CIMB Group Holdings Bhd group chief executive officer Tengku Datuk Seri Zafrul Aziz.

group chief executive officer Tengku Datuk Seri Zafrul Aziz.

Adoption remains a critical success factor in the development of new technology, he says, pointing out that developing and deploying new fintech has been weighed down mainly by legacy issues, practices, systems and corporate culture.

He feels that the organisation providing new modes of payments will essentially own the customer relationship.

“So, the challenge is not about fintech, but about the customer experience.”

In Malaysia, CIMB has a controlling stake in Touch ‘n Go and via that, it is building a new business with the Alibaba group through Ant Financial.

“We are excited about the prospects and in some ways, we could be disrupting ourselves and that is a path we have consciously taken, as it provides a tremendous avenue to be at the cutting edge of innovation and disruption.”

Tengku Zafrul says that in Malaysia, as reported by Fintech Singapore, digital wallet penetration accounts for only 11%.

“Clearly, Malaysia has room to grow its offerings and services of smartphone e-payment solutions. This is further supported by initiatives taken by Bank Negara to reduce the usage of cash in the nation, with the Reduced Merchant Discount Rate policies in place.”

Some critics have said that CIMB’s tie-up with Ant Financial is akin to letting the “devil” into the market because of obvious reasons.

However, others argue and say that if CIMB doesn’t disrupt itself, others will.

“Banks have gone on the defensive and rightly so. If they don’t join the fray, they will lose out and that’s putting it mildly,” quips a banker.

As it stands, there are now more than 20 local licensed e-wallet companies which are in the race for the same pool of customers.

Specifically, five Malaysian banks and as many as 28 non-bank entities have e-money licences issued by Bank Negara, which enable them to issue e-wallets. Most are not active in the e-wallet space and are focused instead on loyalty and petrol cards. Still, more are expected to enter into this space for fear of missing out.

Just earlier this week, low-cost carrier AirAsia Bhd group CEO Tan Sri Tony Fernandes said he wants to expand his BigPay debit card and mobile app, which was recently launched in Malaysia, to other regional countries, adding remittance and money-lending services to it.

Green Packet Bhd group CEO Tan Kay Yen, however, believes that the local market’s size is big enough to accommodate multiple players.

Green Packet has its very own Kiple app that functions as an e-wallet for offline payments.

Not all bad news

Tan also reckons it’s not all bad news for banks.

“There is the business-to-business market, big-ticket transactions and more sophisticated financial instruments that are still the domain of the banks.

“Banks are skilled in risk management and have vast amounts of customer data they can use to develop better services. Tech firms have been slower to impinge on financial services because they have to navigate a fortress of financial regulations,” he says.

In terms of Kiple, Tan says figures have shown “tremendous growth” in the Kiple wallet usage since January 2017, and its list of merchants “has tripled in the last one year, showing increase of confidence in the Kiple brand”. “Our focus for Kiple is to offer more solutions and features to the users.”

Malayan Banking Bhd (Maybank), which is a pioneer in the e-wallet game here, says that the competitive advantage banks have over technology companies moving into financial services is trust and adoption.

“Tech firms need to address these challenges of trust and adoption, both of which are expensive to obtain and maintain, while being very easy to lose,” says its group chief strategy officer Michael Foong.

“Banking brands engender trust in customers’ minds and this will remain our differentiator.”

Nonetheless, he says the bank is not taking the potential threat lightly, opting to proactively work with these tech giants where it makes sense to serve common customers together.

For the concept to work, Foong says it is vital for all parties, especially the new players, to adhere to the same requirements that existing financial institutions must follow to maintain the level of standards and integrity expected from the industry.

“We cannot afford lapses in financial governance for the sake of fanciful convenience that could lead to irreparable damage to the country.”

Maybank can lay claim to being the first in the country to launch a mobile wallet payment platform in the form of MaybankPay. Consequently, the lender partnered Samsung to launch the Samsung Pay mobile wallet.

AMMB Holdings Bhd group CEO Datuk Sulaiman Mohd Tahir admits that in the near future, “the only businesses that will survive in almost every industry will look and behave like technology companies”.

“Banks need to be agile, innovative and committed to transformation,” he says.

But he’s not overly anxious about tech firms taking over the role of banks.

“Tech companies may not be strategically inclined to penetrate the end-to-end spectrum of a universal bank. Even if they were, we must be conscious that success in one industry does not necessarily guarantee success in another.”

Having said that, Sulaiman says there is an untapped opportunity for collaboration between e-wallet providers and banks and says that towards this end, it is exploring options as it “gears up to tap into the exciting opportunities that this collaboration can bring”.

Over on the regulatory side, in order to encourage the use of the QR code, Bank Negara has introduced an Interoperable Credit Transfer Framework.

Via this, customers of banks as well as non-banks will soon enough be able to transfer funds across a common network using a mobile phone or identification number or a QR code.

Similarly, Singaporean regulators are also working on introducing a common QR code network for e-payments into its market, where digital wallets by and large have seen some increase in consumer uptake last year.

To sum things up, while it will be different scenarios for each bank operating in different parts of the world in the future, one thing is for sure – the face of the traditional bank is slowly fading, their profitability is being challenged even more and for sure, those who choose to remain idle will become irrelevant.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.