Rules gradually being enacted to clamp down or regulate trading of cryptocurrencies in some Asian countries

CRYPTOCURRENCIES are all the rage the world over. Based on the potentially revolutionising blockchain technology, the best-known cryptocurrency remains bitcoin, which has attracted the attention of speculative traders across the globe.

This week, though, the cryptocurrency saga hit a notable milestone, which will very likely result in changes in rules related to the trading of such currencies.

Tax authorities in countries such as South Korea and India have clamped down on cryptocurrency exchanges, wanting to know who is dabbling in cryptocurrencies and whether these customers are evading taxes.

New exchanges the world over are doing brisk business facilitating the buying and selling of cryptocurrencies.

The United Kingdom’s The Independent reported this week that Hong Kong’s Binance.com, said to be the world’s largest cryptocurrency exchange, is currently adding a couple of million members every week.

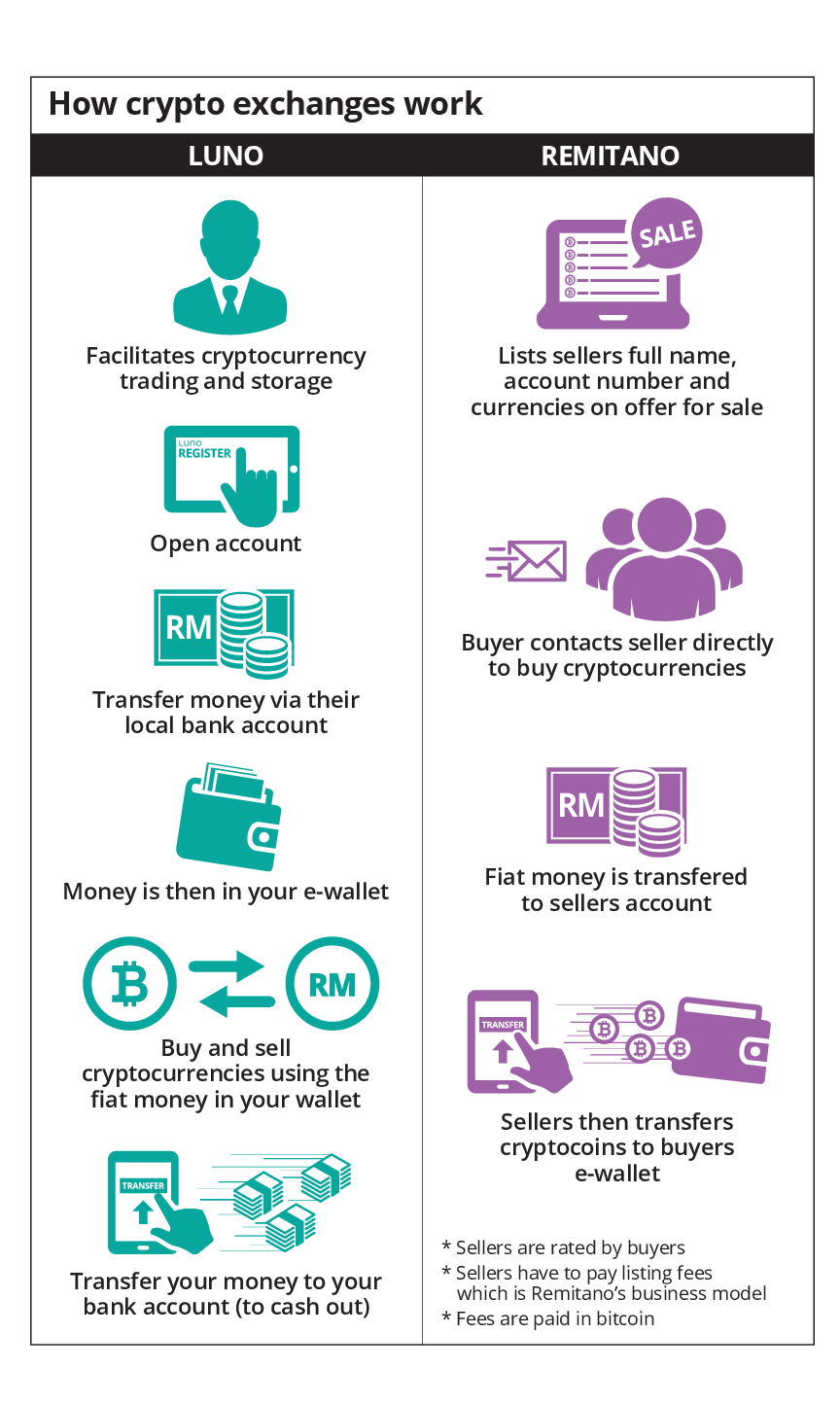

Malaysian tax authorities have also jumped into action. The largest cryptocurrency exchange in Malaysia is said to be Luno. However, over the past few weeks, its bank account in a major local bank was frozen by the authorities.

This sent shockwaves across the cryptocurrency scene in Malaysia.

Luno currently trades the two most popular cryptocurrencies – bitcoin and ethereum.

StarBizWeek reported last month that Luno had one million customers or wallets registered. The exchange had revealed that Malaysians traded over 900 bitcoins on the Luno exchange in a single day last December, which worked out to some RM40mil.

A source had told StarBizWeek in December that one of the popular exchanges had hit a trading volume of some RM500mil from Malaysian trades last year alone.

As for Luno, rumours began circulating as to what was the reason for the freezing of the account, and many had believed that it was linked to the central bank’s rules relating to anti-money laundering.

However, sources now say that the main party that had requested for the freezing of Luno’s account was the tax department.

“Essentially, they want to know who are the parties conducting the trades on Luno, their source of funds and whether sufficient tax has been paid by the owner of those funds,” says the source.

Last month, Bank Negara revealed that an average of RM75mil in transactions of bitcoin and other cryptocurrencies were transacted each month in Malaysia, on four digital currency exchanges.

Besides Luno, the other exchanges in Malaysia are Coinhako, XBit Asia and PinkExchange.

It is understood that Coinhako has also temporarily stopped taking deposits and new account registrations.

Currently, digital currencies are not legal tender in Malaysia, and the central bank has said that it was not stopping the trading of bitcoin.

However, due to the anonymous nature of the transactions and the ease with which large sums of monies may be raised in a short period of time, the concern is that cryptocurrencies are vulnerable to money laundering and terrorist-financing risks.

The traditional anti-money laundering framework requires fund-raising companies and brokers to do their due diligence in areas like knowing the customer, validation of their identity and tracking their sources of wealth.

To be noted is that Bank Negara had recently come out with an e-KYC framework and has been piloting its application in its sandbox with local fintech company MoneyMatch that uses a video conference model to conduct its KYC protocols. This allows for the ability to reach customers from all over Malaysia remotely. This is something crypto exchanges could do in the future to enhance their KYC aspects.

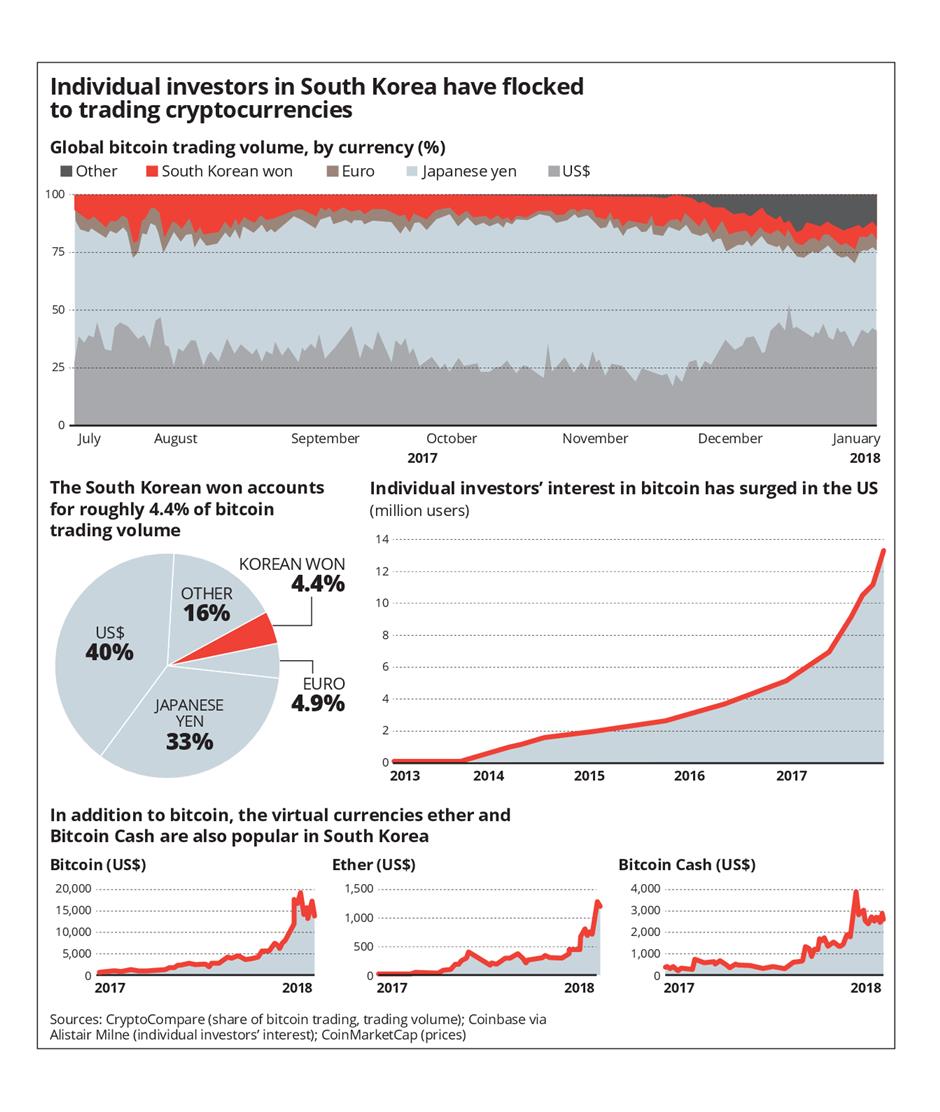

On Thursday, South Korea’s government said it plans to ban cryptocurrency trading, sending bitcoin prices plummeting and throwing the virtual coin market into turmoil, as the nation’s police and tax authorities raided local exchanges on alleged tax evasion.

South Korea is one of the biggest markets for major coins like bitcoin and ethereum, after Japan and the US.

CoinDesk reported that last month, the Indian tax department visited several bitcoin exchanges across the country seeking to identify users. The operation was carried out over suspicions of tax evasion by some exchange customers.

But cryptocurrencies generally still lie in the grey area of the law.

From a tax perspective, aside from the issue of traders’ sources of funds, there are other issues on whether trades, profits and the exchanges’ profits should be taxed.

Incidentally, the government is also looking to tax global digital platforms that operate in Malaysia such as Uber, Grab and Airbnb.

Revenue authorities around the world are finding it hard to track trades made using cryptocurrencies.

Back to Malaysia, Luno head of Asia Pacific Vijay Ayyar tells StarBizWeek that it is “working with Malayan Banking Bhd (Maybank) and the tax people on a few things and hence for the time being, we’re not allowing any transactions”.

(Maybank) and the tax people on a few things and hence for the time being, we’re not allowing any transactions”.

“A lot of it will become clear over the next month once the regulations come out.

“A lot of the issues seem to be around the interpretation of bitcoin regulation in Malaysia.

“We are working closely with Maybank to resolve the current deposit and withdrawal restriction and we are confident that we will resolve the matter soon.

“All existing customer deposits – ringgit and bitcoin – remain safe with us,” he assures.

This week too, the Securities Commission (SC) shut down an initial coin offering (ICO) in Malaysia and says it will not hesitate to rein in others who try to contravene securities laws.

ICOs take place by parties producing white papers detailing their business plans for raising funds via the issuance of new tokens or cryptocurrencies, all purportedly to be built on the blockchain technology.

Last month, the SC said it was working closely with Bank Negara to release a cryptocurrency framework for the country within three months.

The SC has created a number of legalised avenues which would serve the fund-raising needs of small tech firms, including equity crowdfunding, peer-to-peer lending and the Leading Entrepreneur Accelerator Platform Market.

Even so, the red-hot fund-raising trend remains cryptocurrencies.

And strong interest remains among individuals wanting to dabble in cryptocurrencies.

Challenges in curbing trade

While it is easy for the authorities to clamp down on large cryptocurrency exchanges, it is more challenging for them to curb peer-to-peer trades.

This is where individuals wanting to buy and sell cryptocurrencies meet on various sites on the Internet and agree to do direct deals, with monies going into the seller’s bank account, who then transfers his cryptocurrency into the ewallet of the buyer.

Some exchanges operate merely as matching platforms, charging a fee to sellers (paid for in you guessed right, bitcoins) to post their offerings online. Sellers are also given “trust” ratings, not unlike how sellers are also rated on sites like eBay.

One such active exchange locally is Remitano.

Regulated exchanges

With Luno’s account frozen, trading activity in cryptocurrencies in Malaysia is likely to have slowed. “But that will not be for long as other exchanges remain open,” says an active trader.

Aside from the possibility that a crash could hit the value of cryptocurrencies worldwide as many quarters are predicting, it will be unlikely for interest to wane.

Going forward, one likely solution is for exchanges here to be fully regulated and licensed. A good example is Japan, which has come up with a national regulatory framework around cryptocurrency exchanges.

It has been reported that Japan had looked at the issue from the payments perspective and revised their Payments Act to incorporate virtual currency exchanges into that, with specific guidelines and regulations in place.

That will ensure all the necessary knowledge of customers and anti-money laundering safeguards will be in place, and cryptocurrency trades will become a well-governed and possibly taxed activity.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.