But analysts optimistic on outlook of turnaround for AirAsia associates in Indonesia and the Philippines

WHEN AirAsia Bhd released its first quarter results of its current financial year on May 28, most analyst reports the next day highlighted nothing out of the ordinary.

Consensus earnings estimates were trimmed over the next few days but no alarm bells rang over the state of the low-cost carrier’s financials.

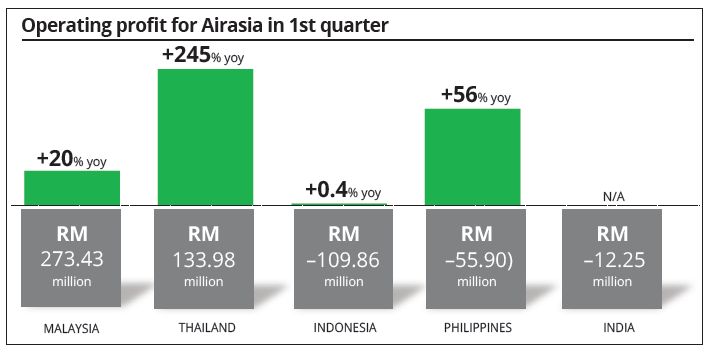

The one beef the market has with AirAsia is the money owed by its affiliates in Indonesia and the Philippines to the parent company, and that found space in a few reports. That sum is large and growing and analysts have wondered if there is going to be an impairment of those advances.

But things took a turn for the worst after June 10 when little known research outfit from Hong Kong, GMT Research, came out with a 39-page report and a sell call.

It was the business links parent AirAsia has with Indonesia AirAsia (IAA) and Philippines AirAsia (PAA) that concerns GMT the most as it didn’t pull any punches at poking holes at AirAsia’s financials.

The report goes into great length to point out the weaknesses of AirAsia’s financials, starting with the related party transactions it has with its associates in Indonesia and the Philippines. It says that conditions were far from good at the end of the first quarter as those two associates were a big drag on AirAsia.

It casts further doubt on AirAsia’s accounts by saying that transactions with AirAsia’s Indonesian and Philipine associates had over the years boosted returns through lucrative aircraft leases, maintenance contracts and other services from the parent company. The report by GMT obviously rankled investors, particularly foreigners who own 54% of AirAsia’s stock.

Selling of AirAsia stock was swift as the report found its way through the inboxes of investors and fund managers, many spending some time to digest what GMT was saying.

Analysts tracking AirAsia’s stock say the revelations were not new and that the fraternity has known about the links for some time. Despite their reaffirmation of their mostly “buy” recommendations on the stock, AirAsia’s shares slipped for five consecutive days from RM2.20 on June 10 to a five-year low of RM1.53 on June 17.

AirAsia’s bosses were quick to respond to the falling share price, appearing on business TV channels to say all is well.

The company on Wednesday issued a business update where it indirectly addressed the issues raised by GMT. AirAsia told the stock exchange it intends to raise fresh capital for IAA and PAA also with plans for an initial public offering of both its subsidiaries.

AirAsia has a similar arrangement in Thailand where its affiliate is now listed and profitable.

GMT’s report

Reports by research outfits highlighting reasons to sell is not the norm in the industry but there is money to be made from both going long and shorting a stock. Iceberg Research wrote a report on Singapore’s Noble Group to voice its concerns over accounting issues with the company some months ago and the stock has fallen about 40% since. That report brought into focus accounting analysis, which later GMT too touched on.

The report by GMT on AirAsia is similar in vein, and by most accounts sparked the selldown in AirAsia shares. In it, the author Gillem Tulloch, says that AirAsia is boosting its profits and cashflow through its links with its associate companies.

It broadly says that real profits have collapsed and AirAsia needs a recapitalisation.

The report argues that the use of related party transactions has boosted AirAsia’s profits by 39% since 2009 and is the only reason why the group remains profitable today.

It argues that RPTs have fattened AirAsia’s operating margins and such transactions, as the number of affiliates it has, have risen from RM13mil in 2004 to RM1.7bil in 2014.

As RPTs grew, the associates’ contribution to AirAsia’s operating profit has risen from 22% to 213% over the same period, says GMT.

GMT says AirAsia would have been loss-making if it were not for the transfer pricing to related parties.

Operating conditions for IAA and PAA have been tough as there is tremendous competition in Indonesia and the Philippines, affecting cashflow payments to AirAsia. The past couple of years revealed the cracks in those operations and GMT says that operating cashflow has fallen 81% from its peak of RM1.6bil in 2010 to RM307mil in 2014, and suspects actual conditions might be worse.

The research outfit claims that IAA and PAA of late have not been paying AirAsia as debt owed by related parties has ballooned from RM170mil at end-2007 to RM2.8bil at the end of the first quarter, with the amounts owed outstripping the sales those associates generate.

It’s not just the amounts owed by those affiliates that is a concern for GMT, as AirAsia has also been extending money for working capital to its associates in Indonesia and the Philippines. In 2014, that amount was RM1.1bil and a further RM323mil was extended in the first quarter of 2015.

Troubles in its associates, according to GMT, has now dragged operating cashflows of AirAsia by 46% to RM1.3bil, which was not helped by AirAsia’s spending on capital expenditure which was close to a record high.

With the amount owed by associates such as IAA and PAA growing and now translates to 60% of shareholders funds, a non-payment of that debt and a write-down would have an adverse impact on the financials of AirAsia, says the report. AirAsia has a net debt to equity ratio of 263%.

It feels AirAsia needs to raise RM7bil to restore its financial health.

AirAsia’s reponse

AirAsia rubbished notions that it is not transparent and in its statement to the stock exchange on Wednesday says it discloses far more than most airlines and “continues to be open about what more it wants to do.”

It says financial statements of IAA and PAA, along with that of operations in Thailand and India, were disclosed in the first quarter of 2015 and that its accounts were prepared in accordance with both the international and local accounting standards, and audited by PricewaterhouseCoopers.

AirAsia says it has been transparent on its aircraft leasing business and has always disclosed the amount of revenue it generated.

“There has been much discussion over the years on leasing income and profit; hence AirAsia created Asia Aviation Capital (AAC), the leasing company which was incorporated in the fourth quarter of 2014, to clearly show the Company’s leasing business and to extract a fair value from AirAsia’s large asset pool of owned aircraft,” it says.

AirAsia says income earned from aircraft leased to the associates is not excessive and the margin is makes is in line with that earned by third party commercial lessors.

The low-cost carrier goes on to say that it does not consolidate the accounts of its associates’ operations in Thailand, Indonesia, Philippines and India due to regulatory reasons as the company is not allowed to own more than 49% (40% in the Philippines) equity interest in each of the entity but the associates’ profits and losses are being taken into account on AirAsia’s income statement via equity accounting method set by the regulators.

AirAsia says IAA has been showing signs of profitability in 3Q14 and 4Q14 after the route rationalisation exercise was executed in the middle of 2014 and the airline was cash positive in the first quarter. Improvements were seen before the crash of QZ8501. It says action is being taken to drive IAA’s return to profitability in 3Q15 and 4Q15 as it targets to breakeven this year.

“IAA will meet payment for lease, MRF and brand license fees due to AirAsia starting this quarter and in some months, forecasted to have surplus to pay down outstanding debt to AirAsia,” it says.

As for its Philippine operations, AirAsia says PAA has shown a better than expected recovery performance in the last couple of months after the turnaround plans were initiated in July 2014.

“In 1Q15, losses have minimised significantly and the Company expects the associate to continue being cash positive. If everything continues to go as planned, profitability is targeted for 4Q15,” says AirAsia.

AirAsia intends to raise about US$100mil with local partners in Indonesia and the Philippines to raise the share capital in those associates from US$13.81mil and US$13.28mil respectively. Part of the money raised will be used to pay down the debt owed to AirAsia.

It also intends to have IAA and PAA issue convertible bonds to raise US$100mil each.

In both cases, AirAsia will match it by capitalising on the debt owned to maintain its shareholding. AirAsia also intends to list IAA and PAA, both having a combined valuation of US$1.3bil (RM4.85bil). Part of the proceeds from the listings, targeted for 2017, will be used to repay the inter-company loans.

To manage debt and cash, AirAsia says it intends to cut its gearing to 2 times by end 2015. It owns 120 aircraft and it has cut aircraft acquisition from an average of 25 a year to 4 a year for the next 3 years.

Convincing the market

That business update on Wednesday and an analyst briefing on the same day helped put out AirAsia’s side of the story on the state of its business. Most analysts said there was really nothing new in the conference call but some voiced doubts whether there would be demand for the convertible loan AirAsia intends to issue as a big sum will be used to repay advances to IAA and PAA instead of being used for those businesses.

“While there were no new takeaways after the conference call, we remain optimistic on its outlook on the turnaround from its Indonesia and Philippines associates. We rule out a rights issue materialising as AirAsia has a pipeline of incoming cash,” says RHB Research Institute in a note on Thursday.

It says discussions in the conference call centred on recovering amounts owed by associates, notably IAA and PAA. It says AirAsia’s auditor is satisfied with management’s turnaround plan at IAA and PAA, as forward loads and yields over the coming quarters are showing signs of improvement. RHB notes that IAA and PAA are lagging behind competitors such as Citilink and Cebu Air.

While it is positive on its associates’ outlook, RHB says conditions will be challenging in the near term for IAA and PAA to start regularising the amounts owed over the next one year, given their weak balance sheets.

“We only expect IAA to start making partial payments (at least the annual payments due) by FY16 (FY17 for PAA). Combined, these annual lease payments (excluding roughly 6% interest on amounts due and intercompany loans) work out to RM552.3mil (IAA: RM386mil, PAA: RM166mil). Management guided that the two can start making partial repayments as early as this year and to fully settle amounts due in five years. We have a more conservative earnings expectation, though we do not rule out that IAA’s and PAA’s net profits could turn out to be better than expected,” it says.

Public Investment Bank Bhd in a note says it was keeping its outperform call on AirAsia but with a lower target price of RM2.53 (previously RM3.08) tagged to a 10x PE multiple to FY16 EPS, after adjusting our assumptions of weaker ringgit from RM3.50 to RM3.70 in FY16F/17F.

The weak ringgit is expected to dent AirAsia’s performance as about 60% of its cost is in US dollars.

“The group’s performance will still be dependent on competition and volatility of US dollar against RM, nevertheless, we remain optimistic on AirAsia due to lower fuel prices, higher ancillary income and better environment with more rational market in Malaysia,” it says.

Related story:

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.