There are suitors for 1MDB’s energy assets, but there are compelling reasons why the fund would opt to list the unit

A FAILED listing of its power-generation division and the growing need to fulfil mounting debt obligations have thrust 1Malaysia Development Bhd’s (1MDB) assets to be ripe for the picking.

Topping the list are assets held under the power-generation division that have attracted no less than the likes of IJM Corp Bhd. For IJM, the power sector is one area that it wants to venture into as the next step towards building its infrastructure-based division.

This is because power plants come with construction work and concession agreements, an arrangement that fits well into where IJM wants to go next. It is similar to highway construction and the subsequent concession agreements.

Although IJM has not gone big into the power sector, expertise is something that the company can easily acquire, says its former managing director Datuk Teh Kian Ming.

That is true to a large extent. IJM is known for its prowess in managing large-scale projects. Power-plant projects run into the billions with huge capital commitments.

“A delay of six months will have an impact on cash flows and cause the projected returns to be out of whack. If power plants are being built on internal rates of return (IRR) of less than 10%, then there is no margin for error,” says a consultant who has worked with numerous power plants, including the Bakun Hydroelectric Dam project that was delayed by a few years.

The construction of the dam in Sarawak, which was supposed to have been completed within four years, took almost double the time before it was done. This resulted in claims and counter-claims between the owner of the project - Sarawak Hidro Sdn Bhd - and the main contractor, which is a joint venture (JV) between Sime Darby Bhd and Sino-Hydro Corp of China.

The disputes amounted to billions of ringgit. If Sarawak Hidro had been a private company with private-sector money, it would have folded.

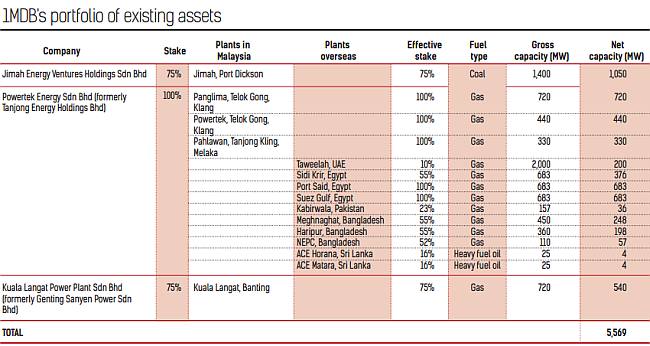

1MDB quickly grew its portfolio of power-generation assets mainly because it is owned by the Finance Ministry (MoF) and its debt papers are easily absorbed by the market on the strength of the shareholder.

Between 2012 and 2014, it acquired three major power-generation companies that gave it a generation clout of close to 5,600MW. 1MDB paid RM8.5bil for Tanjong Plc’s power assets located in and outside Malaysia, RM2.3bil for the Genting group’s power plant in Malaysia and RM1.2bil for a 75% stake in the Jimah power plant in Port Dickson.

The acquisitions gave 1MDB a generating capacity of more than 5,500MW, making it the second-largest independent power producer within just two years. This, however, came at a heavy price.

1MDB paid a total of RM12bil for the power plants, including a premium of RM3.3bil above the fair value.

“No private company is going to pay such high premiums for the assets,” says a merchant banker. “So, if 1MDB were to dispose of its assets, it would have to take the loss.”

This is something that 1MDB cannot afford to do, especially in the present climate where any deal that it undertakes will hog the limelight.

An alternative is to list 1MDB’s energy unit – Edra Global Energy Bhd

This is the preferred option for 1MDB, a signal that was made clear when CIMB Group was relieved of its mandate to look into the disposal of the power-generation assets last month.

“A sale or listing of the power unit will allow 1MDB to deconsolidate the debt of its energy unit from the holding company. This will reduce the glare of the public on the company’s RM42bil liabilities,” says the merchant banker.

The MoF withdrew the letter appointing CIMB to look for buyers of the assets just days after having given the investment bank the mandate.

The flip-flop decision was a sign that 1MDB preferred to list the energy unit. But until the listing takes place, there will be suitors.

Apart from IJM, another candidate also in the running for the power assets of 1MDB is Tenaga Nasional Bhd (TNB).

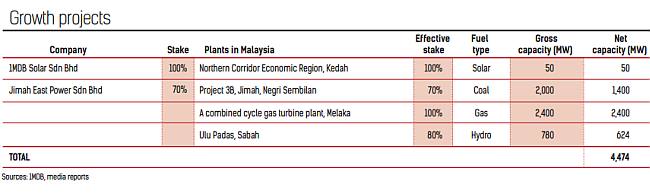

According to industry officials, TNB has already taken over the building of the 2,000MW power plant called the Jimah East project, which is also known as Project 3B.

When 1MDB withdrew its submission to list energy arm Edra from the Securities Commission (SC) in February this year, it had made known that the plan for listing was still an option it would pursue.

According to executives involved in the submission, the proposal did not pass muster with the SC due to the uncertainties on a loan tied to the purchase of the power plants from Tanjong and lack of disclosure on Project 3B.

Why listing is key

Apart from these issues, the executives say that there were concerns about the composition of the Edra board having too many representatives from 1MDB when its equity was to be reduced to 20% post-listing.

“For better governance, the board composition should have more independent directors and representatives of the shareholders,” says a banker.

The listing of Edra was last scheduled to take place in the first quarter of this year, with the sum to be raised estimated at RM5.5bil. That was until 1MDB withdrew its application from the SC in March.

But after power producer Malakoff Corp Bhd had managed to whet investors’ appetite for its listing exercise, there is renewed optimism that Edra could make the cut yet, even without Project 3B.

had managed to whet investors’ appetite for its listing exercise, there is renewed optimism that Edra could make the cut yet, even without Project 3B.

In this respect, industry officials say that 1MDB has started working on a 2,400MW gas-fired power plant that is due to be commissioned in 2021.

They do not discount this power plant being built in Malacca to feature in the proposed listing of Edra.A listing will not only raise money, but also reduce the debt burden on the balance sheet substantially.

“1MDB’s interest in Edra would be down to 20%. The debts would be cut by almost half because of the deconsolidation effect,” says the merchant banker.

Post-listing of Edra, the debts that are tied to the power plants would be deconsolidated from the group level, based on accounting standards.

As of March 31, 2014, 1MDB had liabilities amounting to RM49bil and assets of RM51.4bil. Out of this, RM42bil were long-term debts accumulated for taking up large borrowings to build up a portfolio of power plants and develop the Tun Razak Exchange and Bandar Malaysia projects.

Within the RM42bil debt are three tranches of US-dollar papers amounting to a total of US$4.48bil (RM16bil) which are tied to the power plants that 1MDB had purchased. There are two tranches amounting to US$1.75bil each, issued when 1MDB acquired the Tanjong and Genting power plants. The debts mature in 2022 and the estimated annual interest cost cumulatively is RM666mil.

There is also a short-term paper of US$975mil – a facility utilised to extinguish the put option by Abu Dhabi’s Aabar Investments PJS on the US-dollar loans – that falls due in August this year.

“The short-term paper would probably be refinanced or paid off post-listing,” says the banker.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.