MRCB’s cash call has not gone down well with investors. However, the company says its growing order book calls for it to have a sustainable financing structure.

AT the penthouse of Malaysian Resources Corp Bhd’s (MRCB) headquarters, the executives of the engineering, construction and property developer are huddled in a room explaining the reasons for the company’s proposed rights issue to a group of journalists.

Shareholders generally do not like a cash call, but it is not out of sync in the corporate world. After the one-hour briefing, the message was clear.

The estimated sum of about RM2.2bil that MRCB is seeking from its shareholders is not for any projects related to Bandar Malaysia.

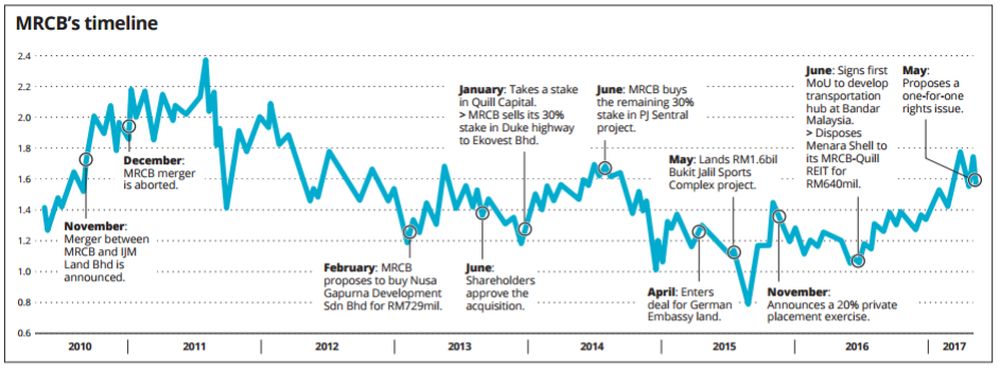

The executives, namely, Ann Wan Tee who is the chief financial officer of MRCB, and Amarjit Chhina, the chief corporate officer, went to great lengths to describe that the company is no longer the corporate vehicle it used to be four years ago when the Gapurna Group, helmed by Tan Sri Mohamed Salim Fateh Din, took over the management after becoming the second-largest shareholder.

Since then, MRCB’s external construction order book has grown from RM1.5bil to RM7bil. The gross development value (GDV) of its enlarged land bank is estimated at RM45bil, much larger than the RM5bil of three years ago.

The fabric of MRCB has changed. Hence, the company has decided that it needs to make a cash call to the tune of some RM2.2bil.

“Given the scale of our project pipeline, we felt that it was important to make sure that we raise adequate funds to finance all our present projects from this fundraising,” MRCB tells StarBizWeek.

However, the market did not respond to the proposal well. MRCB’s share price fell 11.5% on Thursday, a day after the announcement. Poor market sentiment on that day did not help either.

The capital-raising exercise was unexpected since the company had completed a share placement more than a year ago comprising 357.2 million shares, or about 20% of its issued and paid-up capital.

MRCB raised about RM408.1mil from the placement exercise, which was done in three phases.

According to the executives, the placement was done mainly to facilitate MRCB becoming a bumiputra company, whereby it needs a substantial portion of its shares to be held by bumiputra investors. Among those who took up a block was Bank Rakyat, which now holds 8% in MRCB.

Those who had taken up the bumiputra placement shares would probably stand to gain today from the proposed rights issue, as the placement was done between RM1.09 and RM1.26 per share.

It is even cheaper than the entry cost of the Gapurna Group into MRCB in 2013.

Gapurna Group injected assets into MRCB and was paid in a combination of cash and shares priced at RM1.55 each. In that exercise, all shareholders of MRCB, including Gapurna, received warrants that came with a strike price of RM2.30.

Interestingly, MRCB’s largest shareholder, the Employees Provident Fund (EPF), has sold down its warrants, leaving the Gapurna Group as the single largest owner with close to 10% of the outstanding warrants.

The latest exercise offers shareholders one new share for every existing share they hold, a move that would raise the capital base from 2.18 billion to 4.35 billion shares, and also comes with free warrants.

It has caused a stir among shareholders.

Why the need to undertake such a large cash call, which would double its capital base? Would the earnings support the enlarged capital base of the company?

Also, considering that new warrants would be issued, would the old warrants be redundant?

MRCB says that the rights issue is to fund the future growth of the company, which includes the potential RM49bil GDV of its land bank and a five large-scale transportation hub pipeline across the Klang Valley and Penang.

“MRCB has grown from a one-project business, the KL Sentral development, to a large-scale transport-oriented developer (TOD developments), in essence another five KL Sentrals, which will sustain both revenue and profit for another 10 to 15 years,” it says (see separate question-and-answer story on MRCB).

Earnings dilutive

Since the Gapurna Group came into MRCB, it has undertaken a slew of asset-monetisation exercises to reduce the company’s debt level. Net gearing had reduced to 0.73 times as at the end of last year from 1.73 times in 2013.

In Ann’s own words, “There is only so much the management can do to reduce gearing.”

The cash call, when completed, would reduce MRCB’s gearing to almost zero. But does MRCB need to have zero gearing on its balance sheet?

MRCB wants to reduce its dependence on bank borrowings, as it ekes out value on its 400 acres of prime land.

It points out that it would still need to raise funds in the future to finance its future projects, but it would be at levels that are palatable to the market.

“Moving forward, the firm plans to maintain its gearing level of about 0.5 times,” it says.

The company has also ruled out the issuance of bonds, as it says that the market and shareholders do not favour such financing options.

“Given the market’s previous concerns regarding our gearing, any fundraising involving the issuance of bonds would not have been palatable to both shareholders and the market,” it says.

The main concern of analysts on the fundraising is the dilutive impact on MRCB’s earnings per share (EPS). The fear is that the enlarged capital base would not be supported by a growth in earnings.

CIMB Research estimates that the dilution in MRCB’s EPS for the financial year ending Dec 31, 2017 could be between 24% and 39%, taking into account potential interest savings and income from warrant proceeds.

Also, one analyst notes that MRCB had said in 2015 that it would not need to make a cash call when it landed the Bukit Jalil project, a mandate that required the company to refurbish and upgrade the facilities in the National Sports Complex before the SEA Games in August this year.

However, a substantial portion of the proposed rights issue has been slated for the Bukit Jalil project.

Towards this end, MRCB explains that it had to undertake more work that what was originally planned for the completion of the sports facility. From RM500mil, the job scope has increased to RM1.2bil, which changed the company’s funding strategy, according to Ann.

The mitigating point for MRCB to induce the minorities towards accepting the rights issue is that its earnings are on a growth trajectory.

“MRCB is on a growth trajectory. This rights issue has been called to fund that growth,” the company says.

Also, MRCB is tipped to land a few large projects in the next few months. It already has a foot in the building of the high-speed rail station in Bandar Malaysia.

The other two projects that the company is reported to be in the running for are the redevelopment of the Umno headquarters in Kuala Lumpur, and the construction of an incinerator in Kepong (Read: Company in the running for three big jobs).

Shareholder approval

The EPF has given its blessing to the exercise and is likely to take up the excess shares. Gapurna Group has also concurred with the EPF. So, there really is no issue of the proposal getting past shareholders.

However, the buy-in from other shareholders is also needed to ensure that there is a good share spread.

Former investment banker Ian Yoong Kah Yin reckons that the main attraction is that the major shareholders are supporting the deal.

“Minorities would find the rights issue unattractive, as it is a long-term play,” he says.

However, an investment banker points out that the key to whether minorities would go along with the major shareholders on the rights issue lies in the pricing of the rights shares.

“A deep discount is equivalent to a bonus,” says the investment banker.

MRCB is no longer the corporate animal it was five years ago. It has an aggressive set of managers with the Gapurna Group at the helm. Its land bank is located in prime spots in the Klang Valley and it has carved itself a position as a transportation hub specialist.

It is also into railways, the next big business for contractors in Malaysia.

The rights issue will come with dilution. What remains to be seen is how long will it take for the company to create the returns to its shareholders for the additional capital.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.