KUALA LUMPUR: When living costs rise faster than savings can grow, the dream of a comfortable retirement by 60 could prove to be a distant one.

Rising living costs can erode the real purchasing power of retirement savings, says economists who want to see reforms towards a pension system.

Reforming the country’s pension system for both public and private sector employees and strengthening the social safety net for the elderly population is an urgent task due to the ageing population and rising life expectancy, says Sunway University economics professor Dr Yeah Kim Leng.

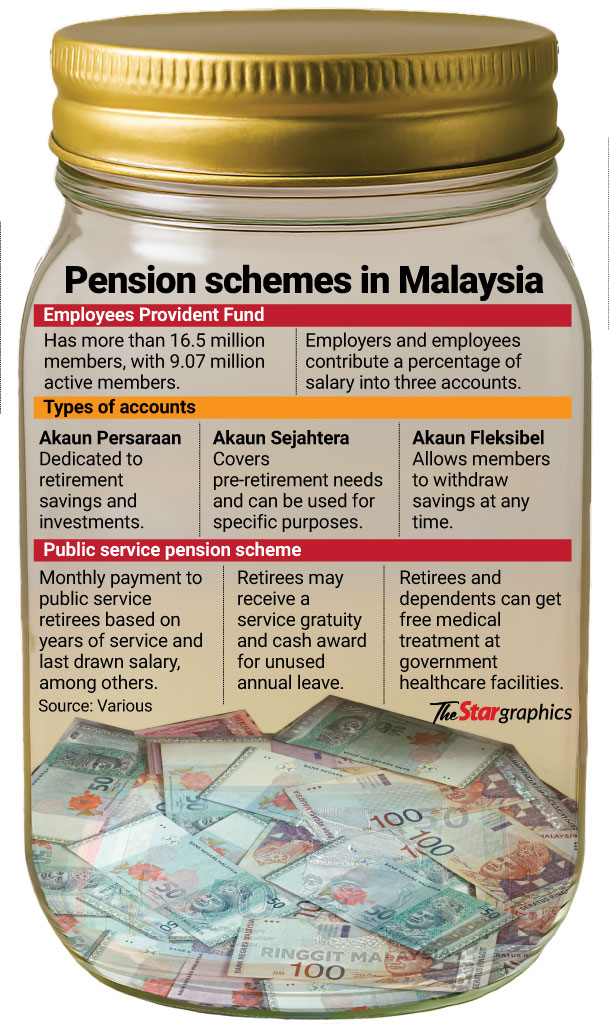

He said the Employees Provident Fund’s (EPF) revamp of its accounts to reflect current needs and its proposed plan to have monthly payments are steps in the right direction.

“Structural reforms could also include a universal pension scheme for the aged.

“Aged care and healthy or productive ageing are other areas of reform needed to ensure comprehensive old age financial and social security for all.”

Yeah added that rising living costs will mean more savings will be needed for those approaching retirement so they can maintain their quality of life after they leave the workforce.

“For those with well-invested savings, returns higher than inflation or keeping pace with it can help mitigate the rise in cost of living.”

He said mandatory pension schemes such as the EPF is also a major source of post-retirement financial security.

However, Yeah said this may not be enough to build a retirement savings pool if the decumulation phase is not planned or considered carefully.

Decumulation refers to the drawing down of accumulated savings to generate a steady income stream during retirement.

“This is because a large proportion of EPF contributors may exhaust savings within a few years following retirement. This could leave them without income security or being dependent on others for support,” he said.

A recent survey showed that only 58% of Malaysians believe they have enough savings to retire.

Many also expressed a strong interest in pension solutions that provide steady retirement income and protection against inflation.

In a separate survey, only 44% of respondents said they feel prepared for retirement, with the survey results also showing that confidence in long-term financial planning continues to decline.

Putra Business School Professor Dr Ahmed Razman Abdul Latiff said the only certainty is that living costs will continue to rise for the foreseeable future.

“This could prove to be a bigger challenge for individuals in the next five to 15 years as the rate of increase of living costs could be higher than that of salary increases.”

He further stressed the importance of financial literacy to optimise savings towards high-yield investments.

“Investments become complicated and are also technology-reliants. We should seize this opportunity to fully optimise return on investments.

“However, the threat of potential scams or frauds very real and the public must be cautious of this,” he said.