SOUTH-East Asia (SEA) stands at the tipping point in its transition towards cleaner energy consumption as ESG values and practices become more integrated into the fabric of the economies of individual countries.

With only five years remaining for the individual countries to meet their 2030 climate pledges, the question of how the region is performing needs to be considered. For that, Bain & Company report on Southeast Asia’s Green Economy 2025, which was prepared in annual partnership with GenZero, Google, Standard Chartered and Temasek, becomes relevant.

The report outlined how the region can accelerate decarbonisation while creating economic value and jobs through a systems-based approach that integrated policy, finance and innovation. It pointed out that climate action must be treated as a strategic growth driver, not just an environmental obligation. However it revealed that despite the region’s obvious progress in sustainable practices, SEA is not on track to meet its targets.

Addressing the barriers

One reason for the discrepancy is that for most parts in the SEA, renewable energy penetration remains below 10%, electric vehicle (EV) adoption charted a low 15%, and that the region requires the need to reduce emissions to 600 tonnes carbon dioxide equivalent in order to achieve its 2030 target.

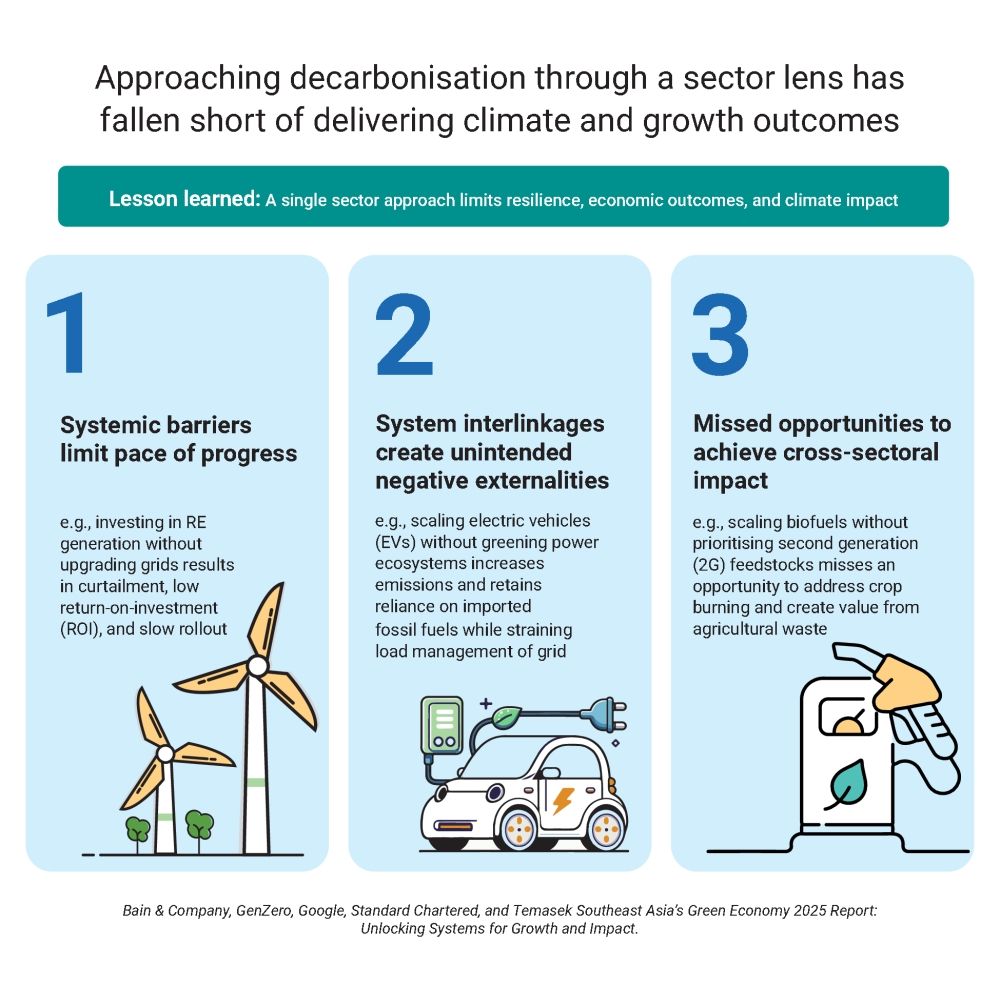

The report described that a sector-by-sector approach has slowed the region’s green transition instead of boosting it.

For more than a decade, climate ambitions in the SEA region have mostly been driven by specific sectors. Governments and industry players have focused on areas such as renewable energy, electric mobility or biofuels in isolation.

But as decarbonisation deadlines approaches, these countries realised that the sectoral approach is not as efficient as expected. The report pointed out that such a sector-only strategy was unable to deliver the scale, resilience and economic impact needed in a fast-changing climate and for energy landscape demands.

Central to the problem are three structural issues. Firstly, that systemic barriers continue to slow down progress, from outdated infrastructure to policy gaps and financial constraints.

Secondly, the transitions within a sector often create unintended consequences for another, especially when the broader energy and industrial systems are not taken into account.

Thirdly, by working in silos, countries miss out on opportunities to unlock cross-sectoral gains that could accelerate both climate and economic outcomes.

The renewable energy sector offers one of the clearest examples. Many markets have invested heavily in new solar and wind projects, yet grid networks have not been upgraded at the same pace. This mismatch has led to power curtailment, lower returns on investment and delays in scaling up new capacity. The ambition exists, but the system is not ready to support it.

A similar pattern is emerging in electric mobility. Governments are pushing to expand electric vehicle adoption, but the power ecosystem that feeds these vehicles remains largely fossil-fuel based.

Without greening the electricity supply, EV growth risks increasing emissions rather than reducing them. At the same time, an unmanaged surge in charging demand places additional strain on already stressed grid systems.

Biofuels are another example of a regional opportunity falling well short of potential. Efforts to scale production have often centred on first-generation feedstocks rather than second-generation alternatives. By not prioritising second generation feedstocks derived from agricultural waste, countries forgo the chance to tackle crop burning while building a more circular, value-added bioeconomy.

Valuable resources are left underused and environmental challenges remain unaddressed.

Simply put, a single sector approach may bring incremental progress, but it does not produce the far-reaching climate and economic benefits the region needs. Achieving meaningful change requires a system-wide perspective where energy, transport, agriculture and industry evolve together rather than in isolation.

The report states that should systems-level solutions be implemented, the region could achieve a 2% increase in GDP, create around 900,000 jobs and close half of its 2030 emissions gap.

Bain & Company’s Global Sustainability Innovation Center’s partner and co-director Dale Hardcastle shared further insights in a question-and-answer session.

The report highlighted three solutions that take a more “integrated systems approach” to address the aforementioned systemic barriers. What are these and what do each entail?

To achieve effective decarbonisation in SEA, stakeholders are turning their focus toward three core systems-level solutions supported by essential enabling mechanisms. These strategies span the critical sectors of agriculture, power and transport, aiming to balance regional economic growth with urgent environmental responsibilities.

> Sustainable bioeconomy: The first pillar focuses on agriculture and nature through the development of a sustainable bioeconomy. The primary objective is to harness local biomass and nature-based solutions to create new industries and jobs while significantly reducing the region’s reliance on imported fossil fuels. Success in this area relies heavily on climate and transition finance, which unlocks capital to innovate and de-risk investments. This financial support is crucial for improving financial inclusion for smallholder farmers. Additionally, green artificial intelligence (AI) leverages data-driven insights to enhance carbon sequestration, maximise land productivity and manage waste more intelligently.

> Next-gen grid development: There is a need to focus investments in grid infrastructure to scale renewable power and improve system reliability. This helps ensure long-term regional energy security, affordability and climate resilience. To facilitate this high-expenditure shift, climate finance should act as catalysts for long-term funding that balances risk and reward. Also, carbon markets can accelerate a clean energy transition by offering increased monetisation opportunities. Operational efficiency is further boosted by AI-driven grid balancing, predictive maintenance and generation forecasting to optimise energy demand and supply.

> EV ecosystem: This addresses the transport sector via the EV ecosystem. Asia’s transition to EVs presents a robust opportunity for manufacturing and innovation, driving the development of SEA supply chains to enhance global competitiveness and reduce long-term emissions. Mobilising financing is necessary to accelerate adoption and expand charging infrastructure. Furthermore, AI tools are employed to optimise energy usage in EV infrastructure through congestion prevention and grid balancing.

How close are each country in the region towards reaching their individual decarbonisation goals, especially for Malaysia, Indonesia and the Philippines?

Across SEA, countries have made visible progress in establishing decarbonisation frameworks and setting targets, yet the pace of implementation remains uneven. Malaysia, Indonesia and the Philippines stand at different stages of readiness and execution, reflecting variations in policy maturity, energy mix and investment climate, as well as the scale of decarbonisation needed.

When taken together, Malaysia, Indonesia and the Philippines, alongside their South-East Asian peers, are making credible progress but remain off track to meet the full 2030 emissions-reduction trajectory. This gap can be closed through efforts including accelerated grid reform, clearer transition finance mechanisms and coordinated regional power trade. We estimate that system-level solutions across grids, mobility and bioeconomy systems could close up to 50% of the region’s 2030 gap while driving inclusive growth. This would be a material change.

Malaysia has set a target to achieve net zero by 2050 and reduce the carbon intensity of GDP by 45% by 2030 (from 2005 levels). Progress is tangible in renewable energy capacity, now exceeding 25% of installed capacity, and in emerging private-sector participation through green PPAs and corporate sustainability programmes.

However, fossil-fuel subsidies and grid bottlenecks continue to constrain large-scale renewable deployment. Ideas and critical next steps to address these include reforms to liberalise the grid, enable third-party access and accelerate investment in transmission infrastructure. These are some measures that support Malaysia’s progress towards its 2030 interim targets.

Indonesia’s decarbonisation pathway is framed around reaching net zero by 2060, with a 2030 goal of reducing emissions by 31.9% unconditionally (or 43.2% with international support). They had also launched the Just Energy Transition Partnership (JETP) and a series of renewable auctions, signalling stronger intent.

Nonetheless, coal continues to account for over 60% of power generation, and renewable build-out has lagged policy announcements. Challenges include policy fragmentation, state-owned utility dominance and limited grid interconnectivity. The creation of green industrial clusters and cross-border power trade frameworks could accelerate alignment with national targets.

The Philippines has committed to a 75% emissions reduction by 2030 (conditional on international finance) and has emerged as one of the more open energy markets in the region. The country’s renewable share in generation has reached roughly 22%, driven by feed-in tariffs, renewable portfolio standards and active private investment.

However, grid congestion and inadequate transmission infrastructure restrict renewable penetration, particularly in the Visayas and Mindanao regions. The report suggests that sustained investment in transmission capacity, battery storage and standardised power-trading frameworks could allow the Philippines to exceed its interim decarbonisation targets.

The report states that a systems-level approach could increase the region’s GDP by US$120bil (RM490bil) and create 900,000 jobs. What are the key policy changes needed to unlock this economic potential whilst pursuing decarbonisation?

Unlocking roughly US$120bil in GDP and 900,000 jobs by 2030 will require reforms to energy markets, phasing down fossil-fuel subsidies, and enabling private investment in transmission and distribution infrastructure. Harmonising frameworks for cross-border power trade, scaling transition= finance and expanding the high-integrity carbon market will also be crucial to sustain economic momentum and decarbonisation.

Given that SEA’s current bioeconomy practices contribute to roughly 30% of the region’s total emissions, what are the most critical steps to transition to a sustainable bioeconomy that balances economic growth and environmental protection?

A sustainable bioeconomy requires scaling regenerative farming, enforcing sustainability standards in key commodities, and incentivising advanced biofuels.

Investment in measurement, reporting, verification (MRV) systems, and blended finance for nature-based projects, will help align economic growth with ecological protection. Transparent carbon credit markets can further monetise sustainable practices.

With the demand for data centres in SEA growing at a rate of 19% annually, what strategies can be implemented to ensure this growth is sustainable and does not derail the region’s decarbonisation goals?

With such growth, sustainability must be embedded into digital infrastructure expansion. Governments and operators should adopt efficiency benchmarks, mandate renewable energy procurement through power purchase agreements (PPAs) or virtual PPAs and should also co-locate facilities near clean power sources. Integrating load-shifting and waste heat recovery systems will also help ensure digital growth complements rather than competes with national decarbonisation goals.

The report highlights that SEA-6 nations are still heavily reliant on ICE vehicle production. What are the most effective dual strategies for both accelerating EV adoption and strengthening regional EV production to maintain manufacturing competitiveness?

The region’s automotive sector remains dominated by internal combustion engines. A dual-track strategy is essential—combining consumer incentives, infrastructure readiness and EV mandates on the demand side with regional supply-chain development, localised manufacturing and technology partnerships on the supply side. Such an approach safeguards decarbonisation progress, industrial competitiveness and jobs in the sector.

How can AI be most effectively deployed to reduce emissions across the power, transport and agriculture sectors in SEA and what investments are needed to realise this potential?

AI can significantly improve energy efficiency and emissions management across key sectors. In power, AI can optimise grid operations and renewable forecasting. In transport, it can enhance route optimisation and charging patterns. As for agriculture, it can enable precision farming and carbon monitoring. Realising these benefits will require investment in digital infrastructure, data interoperability, and workforce skills.

What are the primary barriers to expanding and modernising domestic and cross-border electricity grids and how can “green industrial clusters” help to overcome these challenges?

Grid expansion is constrained by regulatory rigidity, unclear tariff structures, and fragmented cross-border coordination. Green industrial clusters, where renewable generation, storage and anchor industrial demand are co-located, can accelerate grid upgrades, de-risk investment and catalyse public–private partnerships. Such clusters serve as practical demonstrations of system-level decarbonisation.

The report indicates a significant gap between current green investment and the amount needed to meet 2030 targets. What are the most innovative

financing mechanisms that can be scaled up to bridge this gap, especially for harder-to-abate sectors?

To close the 2030 investment gap, we need blended finance, transition funds for early coal retirement and regional green-infrastructure platforms. Coupled with corporate PPAs and robust carbon markets, these instruments can crowd in private capital and move the needle in high-impact sectors, such as power and nature-based solutions

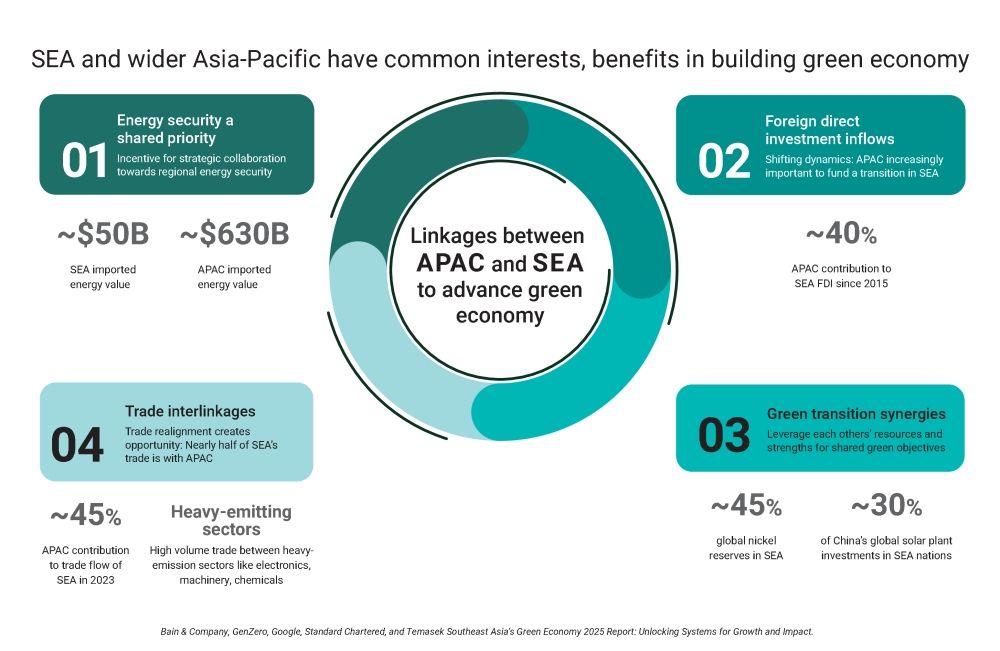

Given the strong trade and investment links between SEA and the wider Asia-Pacific region, what are the most promising opportunities for collaboration that could accelerate the green transition for all parties involved?

Stronger Asia–Pacific partnerships are one of the fastest ways to scale SEA’s green transition. Joint investment in grid infrastructure, along with clear regulatory frameworks for cross-border power trade, will unlock cheaper, more reliable clean electricity.

At the same time, co-developing EV and battery manufacturing ecosystems and deepening collaboration on carbon markets with consistent sustainability standards, will further accelerate the region’s collective green transition.