PETALING JAYA: The equity market could be ripe for a rebound over the next six months, given the deep value that has emerged following the heavy selldown in the first half of 2023.

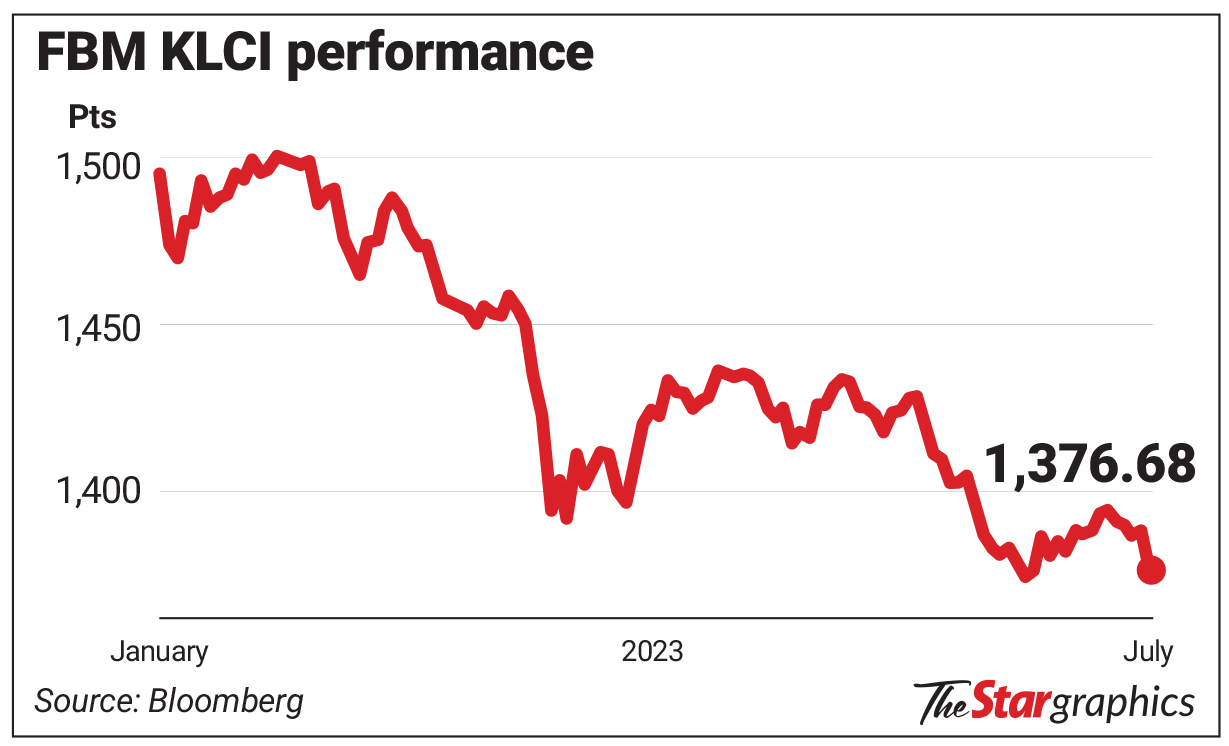

Closing at 1,376 points last Friday, the benchmark FBM KLCI is hovering at eight-month lows and has declined about 7.1% since the start of 2023.

At this level, the local equity market was valued at around 15 times the benchmark’s estimated earnings of 2023, and 14 times that of 2024. The benchmark also closed lower for the second consecutive quarter.

Analysts believe the bearish sentiment on the local exchange could linger at least for a couple of months more as the investment case for a quick recovery is lacking.

Nixon Wong, chief investment officer at Tradeview Capital, said the second quarter (2Q) was rather muted with limited positive catalysts and lingering concerns on the outcome of the state elections that are approaching.

The rather disappointing corporate results reported in April to May did not help as well, and further added to the poor investment sentiment during the quarter.

“With state elections, which will dominate the first half of 3Q, we believe the market could still be in the doldrums until a clear result is seen post-elections. After that, we are likely to see some positive recovery since the political risk will be behind us, in our view,” he told StarBiz.

Wong believes the weak ringgit was partially a result of the US dollar strength, which he believes may be peaking in the near future, when the US economy starts to slow and the Federal Reserve (Fed) rate hike is paused, and should see some inflow back into Malaysia as the currency may be seen as undervalued.

Any heavy lifting of the local indices will have to be done by local funds, as foreign fund managers will likely remain net short on the local markets and focused on other Asian markets, according to global fund manager Schroders.

Dionne Cheung, associate investment director, Asia ex-Japan equities at Schroders Investment Management (Hong Kong) Ltd, said the local stock market’s performance relative to regional markets has not been very good, as investor attention in 2023 has been on the tech cycle bottoming and China reopening thematics.

The tech cycle bottoming was why tech-heavy markets like Taiwan and South Korea have been leading this year, while the China reopening has fallen short of investors expectations.

“For Malaysia we don’t see any catalysts as we know gross domestic product growth in the second half of this year will be much lower due to the high base from the same period last year.

“So the second half will be quite challenging for Malaysia because you have a high comparison base and is not quite attractive for investors.

“They can park the money in Taiwan and South Korea as they can hope for tech recovery, or in Hong Kong or China where you can hope for more stimulus whereas Indonesia and India remain attractive.

Asean markets are at the later stage of the cyclical recovery and going forward cannot enjoy the low base but have a higher interest rate environment. So on a relative basis, Malaysia or even Thailand, is not attractive compared to other Asian markets. Finally the ringgit is quite weak which makes the investment case less attractive this year,” she said.

Nevertheless, Wong intends to keep an eye on the tech and industrial production sector given the relative underperformance year-to-date compared to other sectors.

“Its still pretty much a trading market, hence maintain a balanced approach whereby have both dividend yielders (as downside support) while also growth names to tap along on potential recovery from China economic point of view and valuation recovery of the local bourse,” he said.

According to Kenanga Research, Bursa Malaysia’s levels now are equivalent to bottom valuations during non-crisis times and represented the lowest points since the European sovereign debt crisis more than a decade ago.

As such, the brokerage is calling the bottom for the Malaysian equity market. It sees a potential for some rebound, with the FBM KLCI expected to end this year at 1,480 points based on 16 times the estimated earnings of 2023, and 15 times that of 2024.

“We believe the significant year-to-date underperformance of the local market itself already warrants a catch-up play,” Kenanga Research wrote in its recent investment strategy report.

It noted the valuations for its end-2023 FBM KLCI target come at a discount to the market’s five-year historical average of 18 times earnings to reflect equity valuation compression due to a more restrictive monetary policy by major policymakers globally over the short term.

“While we believe the local market has bottomed out, it is more likely to decisively break out from the doldrums under two conditions, namely a dovish pivot by the US Federal Reserve (Fed), and a market-friendly outcome of the six impending state elections,” Kenanga Research explained.

“The global market has rallied thus far this year driven by expectations of an end to the rate hike cycle in the US, and to a certain extent, the Artificial Intelligence frenzy. However, our local bourse has very much sat this out,” it added.

Kenanga Research pointed out that a dovish pivot by the Fed could potentially drive the global market to go another leg-up, which could eventually inspire a more sustainable uptrend in the local stock market.

The research house has a “market-friendly” outcome from the upcoming polls as the outcome would be one that would not unsettle the present political stability, or more specifically, erode the confidence of the unity government’s partners under the leadership of Prime Minister Datuk Seri Anwar Ibrahim.

“Assuming a ‘market-friendly’ outcome of the state elections, the unity government will then be able to expedite its policy reforms,” Kenanga Research said.

“A well-thought-out subsidy rationalisation plan and the reintroduction of some form of consumption tax to broaden the tax base could spark a re-rating of the local market as they would cement the long-term fiscal sustainability of the nation,” it added.

Kenanga Research recommended banks and telecommunications companies (telcos) and plantation companies for value play.

“We believe the sell down on banking stocks in the first half of 2023 on the heels of the banking crisis in the US and Europe was unjustified,” it said.

“We like telcos for their earnings resilience with telecommunications services having evolved into a basic necessity of modern life. We see an opportunistic risk-and-reward situation in plantation stocks by virtue of their downside risk that is well protected by asset value, but tremendous upside reward if the current El Nino weather phenomenon turns out to be a strong one,” it added.

Meanwhile, Kenanga Research said it would expect a significant revitalisation of the construction sector in the second half of 2023, backed by the roll-out of the RM45bil Mass Rapid Transit 3 project and six flood mitigation projects worth RM13bil and a vibrant private-sector construction market backed by building jobs for new semiconductor foundries and data centres.

It was also positive on the automotive sector based on strong consumer confidence and buying interest enticed by attractive new models.

Already a subscriber? Log in

Get 20% OFF The Star Digital Access

Cancel anytime. Ad-free. Unlimited access with perks.